Are we being unfair when we constantly fret over the slow transmission of interest rates by banks when the repo rate is cut? This has become a habit of late, one where there is a lot of concern raised on the slow transmission process. The storyline is now familiar. RBI lowers the repo rate and is joined by the government which presses banks to take action on lending rates. Periodically, bankers are summoned to Delhi, and the case is put forward on lowering rates. The view put forth by economists and analysts is that the banks are not following RBI’s suit, and that blunts the efficacy of monetary policy. How far is this true?

Two things need to be understood here. The first is that the lending rate is driven by a formula. There is the base rate and the MCLR (an improvement over the base rate concept), which is driven by a formula. One variable in the formula is the repo rate; that, however, affects a very small part of the total cost of funds and is negligible (total LAF borrowings at repo rate is fixed at 1% of NDTL). The most important component is the deposit cost, which has to change. If this cost changes, the base rate or MCLR will come down accordingly. This becomes the benchmark for banks to decide on other lending rates. Therefore, the crux is the changing of the deposit rate and the benchmark lending rate.

The second is that the mechanics of interest rates changes. Banks first have to lower deposit rates. But all deposits are generally contractual and have fixed rates till maturity. Hence, when it comes to time deposits, the new price can come in with a hiatus, say, when the deposits come for renewal or when new deposits are reckoned. Therefore, even if deposit rates are lowered, the impact on cost would come with a lag. Now, when it comes to lending rates, once lowered, it would be applicable for all loans and, hence, the revenue would dip for the bank when rates are reduced. Hence there is a priori reason to believe that the pace of lowering of lending rates will be calibrated with time. But what is the true picture?

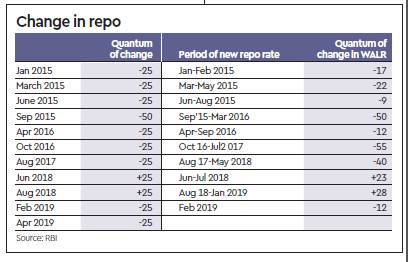

The accompanying graphic looks at the changes in interest rates developments since January 2015. The movements in the repo rate are mapped with the changes in the extent to which the WALR (weighted average lending rate) on fresh rupee loans sanctioned has moved.

The idea here is to look at the month in which the repo rate was changed and see the corresponding change in the WALR during the period when the new repo rate change was valid, which would be till the next change in policy was announced. From January 2015 to June 2018, there were seven reductions in the repo rate (six occasions of 25 bps each and one of 50 bps), amounting to 200 bps, and the weighted average lending rate (WALR) of banks changed by an equivalent of 205 bps during this period. This indicates an elasticity factor of 1. When the repo rate was increased by 50 bps in the next two policies, the WALR for banks rose by 51 bps, which is again an elasticity of 1. Therefore, if one tracks the changes on the repo and the reaction of banks to these changes, it does appear that banks have been very receptive to policy. There is little reason to believe that there is any transmission issue with banks.

The change will not be instantaneous for sure and will take time to work out, as can be seen in the graphic. There are processes involved in the bank where the ALCO meets and decides on the interest rate action. In fact, when the rate-cut is allowed to work through for a longer period of time, which can be more than six months, then the effect is sharper and the past rate-cuts also get included in the final impact. This has been so in all the three instances when the WALR has changed by more than 40 bps over the longer time period. In two of these cases, the reaction was to an immediate cut of only 25 bps—in October 2016 and August 2017.

Hence, quite to the contrary, it appears that banks have actually been very receptive to RBI’s policy changes and passed on the benefit of lower repo rates to the customers. This does not appear apparent when one looks at just the base rate or MCLR that have tended to be sluggish in changing as they are driven by the formula where the deposit rate is critical. This is probably why it does look as if banks lower their deposit rates at a faster pace than their lending rates. But, as the data shows, this is not true and banks do in fact give a good part of the benefit to the average customer. In fact, one could argue that banks have been doing so even though the NPA levels have been high, where the credit risk environment has not been congenial. Ideally, these rates should be less than elastic when the credit risk perception is higher.

This data should also satisfy RBI that has been trying to reconcile the phenomenon of repo rate changes with market interest rates. In a way, it is a vindication of the efficacy of monetary policy. Data, however, indicate that the interest rate cut should be given time to work through and, typically, a longer time-period relates well with policy changes. There is definitely no need to get overly critical of bank reaction to policy changes.

The author is Chief economist, CARE Ratings Views are personal