For most investors, the phrase “China Plus One” has gone from a strategic foresight to a somewhat exhausted cliché. For the better part of the last three years, every mid-cap management team with a CNC machine and an export license has utilized it as a boilerplate growth narrative.

However, as we get ready for FY27, the market is ruthlessly separating the assemblers from the actual engineers. The easy alpha made on the back of generic supply chain shifts has largely evaporated, replaced by a much more lucrative, albeit complex, opportunity: The Precision Engineering Bottleneck.

And there are companies that do not simply make things cheaper than their counterparts in Guangzhou or Zhejiang, but they manufacture components that are technically almost impossible to replicate, mission-critical to the end-user’s final product, and deeply integrated into global high-growth cycles like AI infrastructure and specialized healthcare.

And two such stocks are held by the Big Whale of the market, Ashish Kacholia. Known for his surgical entries into small and mid-cap alpha, Kacholia has been holding these two stocks for quite some time now. These holdings hint towards him no longer betting on the broad, horizontal theme of manufacturing, but on the vertical entities that have successfully navigated the chasm from commodity-adjacent products to high-barrier precision components.

The precision engineering bottleneck: India’s shift from volume to value

To understand why Ashish Kacholia has been interested in these two stocks, one must first understand the shift in India’s manufacturing comparative advantage. The first wave of China Plus One was about volume. India provided the labour and the space.

The second wave, which we are currently entering, is about Reliability and Complexity. In a world of “Just-in-Case” supply chains, global OEMs (Original Equipment Manufacturers) are looking for partners who can co-design components.

And this is exactly where the 2 precision bets of Kacholia come in. Let us take a dive in and see if these companies are performing on the promise of growing from vendors to Tier-1 Partners.

Aeroflex Industries: A thermal management proxy for the AI revolution

For years, Aeroflex Industries was known as a manufacturer of stainless-steel flexible hoses. While a steady business, it lacked the glamour of high-tech manufacturing. But one look at the Q2 and Q3 FY26 earnings, and one would see that the cycles have revealed a radical transformation. Aeroflex is no longer a hose company. It is now a Thermal Management Proxy for the AI revolution.

The company’s current market cap is Rs 3,160 and Kacholia currently holds 2% stake in the company worth Rs 62 cr.

Let us try to find out what has held Kacholia for all these years.

The Liquid cooling opportunity: Doubling revenue via AI data center manifolds

The global AI boom has a physical, thermodynamic limit: Heat. As Nvidia’s latest H200 and Blackwell chips consume unprecedented levels of power, traditional air cooling is reaching its breaking point. The world is shifting toward Liquid Cooling, and Aeroflex has positioned itself as a frontrunner in this shift.

In a recent investor call, Managing Director Asad Daud provided a roadmap that caught the market by surprise: “The global market for liquid cooling is expanding at a CAGR of 33%. We are not just supplying hoses; we are supplying the entire manifold and skid assemblies.”

The company has expanded its skid assembly capacity from 2,000 units to 15,000 units per annum, with the final robotic welding lines set to be commissioned by June 2026. At a realization of approximately Rs 300,000 per skid, the revenue potential of this segment alone exceeds Rs 400 cr at peak utilization, effectively doubling the company’s current revenue base.

Aeroflex financial blueprint: Analyzing the 60% profit CAGR

When you look at the financials of the company, it gives a hint of what may have attracted Kacholia.

The sales of the company have grown at a compound rate of 19% from Rs 144 cr in FY20 to Rs 346 cr in FY25, while the sales for the 3 quarters of FY26 ending December 2025 was Rs 316 cr.

Regarding the EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), grew at a compound rate of 30% from Rs 22 cr to Rs 80 cr in the same period. And for the 3 quarters of FY26, the EBITDA logged was Rs 69 cr.

The Net Profits of the company jumped from Rs 5 cr in FY20 to Rs 53 cr in FY25, which is a compound growth of 60%. And for the 3 quarters of FY26, profits of Rs 37 cr were recorded by the company.

The share price of Aeroflex Industries was Rs 163 when it was listed in September 2023, and as of closing on 30th March 2026 it was Rs 239.

The share is trading at a PE of 64x, and the industry median is 16x, which means that the market is pricing in significant future growth expectations and assigning a premium valuation to the company compared to its peers.

Also, one of the most critical metrics when looking at a company like Aeroflex, is the CFO (Cash Flow from Operations)-to-EBITDA ratio. Aeroflex converts over 80% of its EBITDA into hard cash, a solid number.

What is also worth noting is that despite the massive Chakan plant expansion, the company remains Virtually Debt-Free (Debt-to-Equity: 0.00). This provides them with a solid margin of safety which can act as a cushion if the global economy faces a temporary slowdown.

Shaily Engineering: Leveraging the Global GLP-1 and Insulin boom

If Aeroflex is the proxy for AI, Shaily Engineering is the proxy for the global GLP-1 (Obesity Drug) and Insulin Revolution.

With a market cap of Rs 9,579 cr, Shaily’s journey from making high-volume plastic parts for IKEA to manufacturing complex pen-injectors for global pharma is a masterclass in business transformation.

The company also offers secondary operations in plastics like vacuum metalizing, hot stamping, and ultrasonic welding. Its manufacturing facilities are at Savli and Halol, Vadodara, Gujarat.

However, what makes this stock impressive for smart investors is its healthcare pivot.

Healthcare CDMO Pivot: Why Shaily’s medical revenue jumped 139%

In the December 2025 quarter, Shaily’s healthcare vertical didn’t just grow; we can say it exploded. Revenue from this segment jumped 139% YoY, and for the first time, healthcare now contributes 42% of total revenue (up from 20% just 18 months ago).

Management guidance for FY27 is even more aggressive. With the onboarding of two new global Top 10 pharma majors for GLP-1 pen manufacturing, Shaily is transitioning into a full-scale CDMO (Contract Development and Manufacturing Organization).

Apart from this, the company’s Abu Dhabi Gambit with a Rs 350 cr expansion is more of a strategic hedge. It is not just a capacity play. By manufacturing in the UAE, Shaily get proximity to the European and Middle Eastern markets with favourable trade agreements.

Plus, it helps in reducing the “India-discount” in global drug delivery procurement, where lead times are critical. Not to forget, the plant adds 75 million units of annual pen-injector capacity, targeting a global market that is currently facing a severe supply-side shortage.

Shaily’s Capital Efficiency: Operating margins expand to 28%

Let us look at the financials of the company to see what has made Kacholia stay loyal to the stock with a current holding of 5.2% worth Rs 490 cr.

The sales of the company have grown at a compounded rate of 11% from Rs 568 cr in FY22 to Rs 787 cr in FY25. And for the 3 quarters of FY26 ending in December 2025, the sales recorded by the company were Rs 754 cr.

EBITDA jumped from Rs 82 cr in FY22 to Rs 177 cr in FY25, which is a compound growth of over 29%. For the first 3 quarters of FY26, the company logged in an EBITDA of Rs 213 cr already and surpassed the previous years number in just 9 months.

The Operating Profit Margins (OPM) jumped from 15% in FY22 to 22% in FY25. For the trailing twelve months, the OPM is 28%.

Regarding net profits, the company recorded a compounded growth of 38%. For the first 3 quarters of FY26, the company logged in profits of Rs 129 cr, which is 38% higher than the FY25 figure of Rs 93 cr.

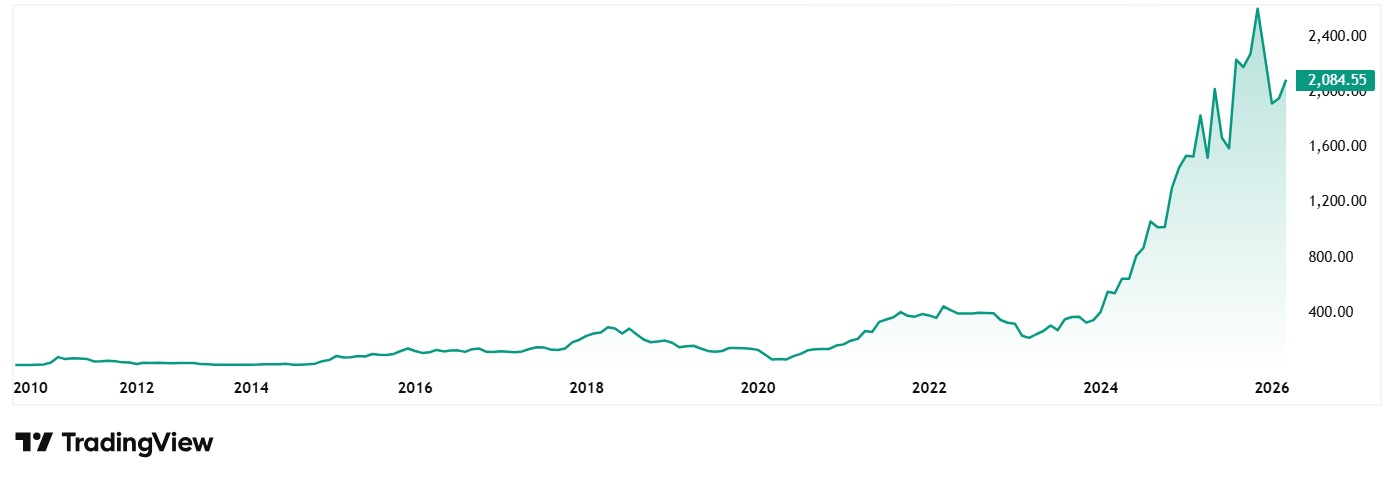

The share price of Shaily Engineering Plastics Ltd was around Rs 199 in March 2021 and as of closing on 30th March 2026 it was Rs 2,084.

However, in the last few months, the stock price has corrected by over 24% from its all-time high of Rs 2,750 to its current price of Rs 2,084. This correction is a textbook valuation reset where the current 60x P/E collided with sub-50% capacity utilization and consumer-segment weakness.

While healthcare demand remains robust, the market is discounting near-term headwinds from aggressive Abu Dhabi capex and pricing erosion on key contracts. Essentially, the stock’s premium outran its operational ramp-up, triggering a necessary correction to align with current factory-floor realities.

However, despite being in a heavy CAPEX phase, Shaily’s Fixed Asset Turnover remains healthy, suggesting that management is not over-building but is instead building precisely for secured orders.

Decoding Kacholia’s cluster strategy

Now, one question for anyone who has read this far is, why has a seasoned investor like Kacholia been holding them both? Well, it’s about the Correlation of Growth Drivers. Both Aeroflex and Shaily are Pick and Shovel plays for the world’s two most aggressive growth cycles:

- The Infrastructure Cycle: Data centres need cooling (Aeroflex).

- The Bio-Pharma Cycle: Modern drugs need precision delivery (Shaily).

By holding both, Kacholia is possibly insulated from sector-specific shocks. If pharma regulations tighten, the AI boom compensates. If data centre growth slows, the global obesity drug craze provides the floor. This is what cluster investing is all about.

Are Aeroflex and Shaily priced for perfection?

No balanced analysis can ignore the elephant in the room: Valuation.

At P/E multiples exceeding 60x, both Aeroflex and Shaily are currently higher than industry medians. The market is probably discounting their FY27 earnings today. This leaves very little room for operational error.

For Aeroflex, any delay in the commissioning of the robotic welding lines at Chakan would be seen as a major red flag. For Shaily, the execution of the Abu Dhabi plant is the X-Factor. If that plant faces regulatory or construction delays, the stock’s current premium could evaporate quickly.

Also, both companies are exposed to Global Regulatory Risks. Aeroflex depends on US-China trade relations remaining stable enough for China Plus One to remain a priority. Shaily depends on US FDA and global health approvals for its CDMO clients.

How things will unfold for these two stocks would be a fascinating watch. You should add these stocks to a watchlist and watch them closely, if you want to be in the know.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.