Airbnb’s business does not look broken.

In 2025, revenue grew to $12.2 billion, up 10% year-on-year. Gross Booking Value crossed $91 billion. More than 533 million nights and experiences were booked on the platform. Free cash flow was strong at $4.6 billion, with margins close to 38%. On most operating metrics, Airbnb continues to look like a durable, profitable platform.

And yet, the stock has not reflected that strength.

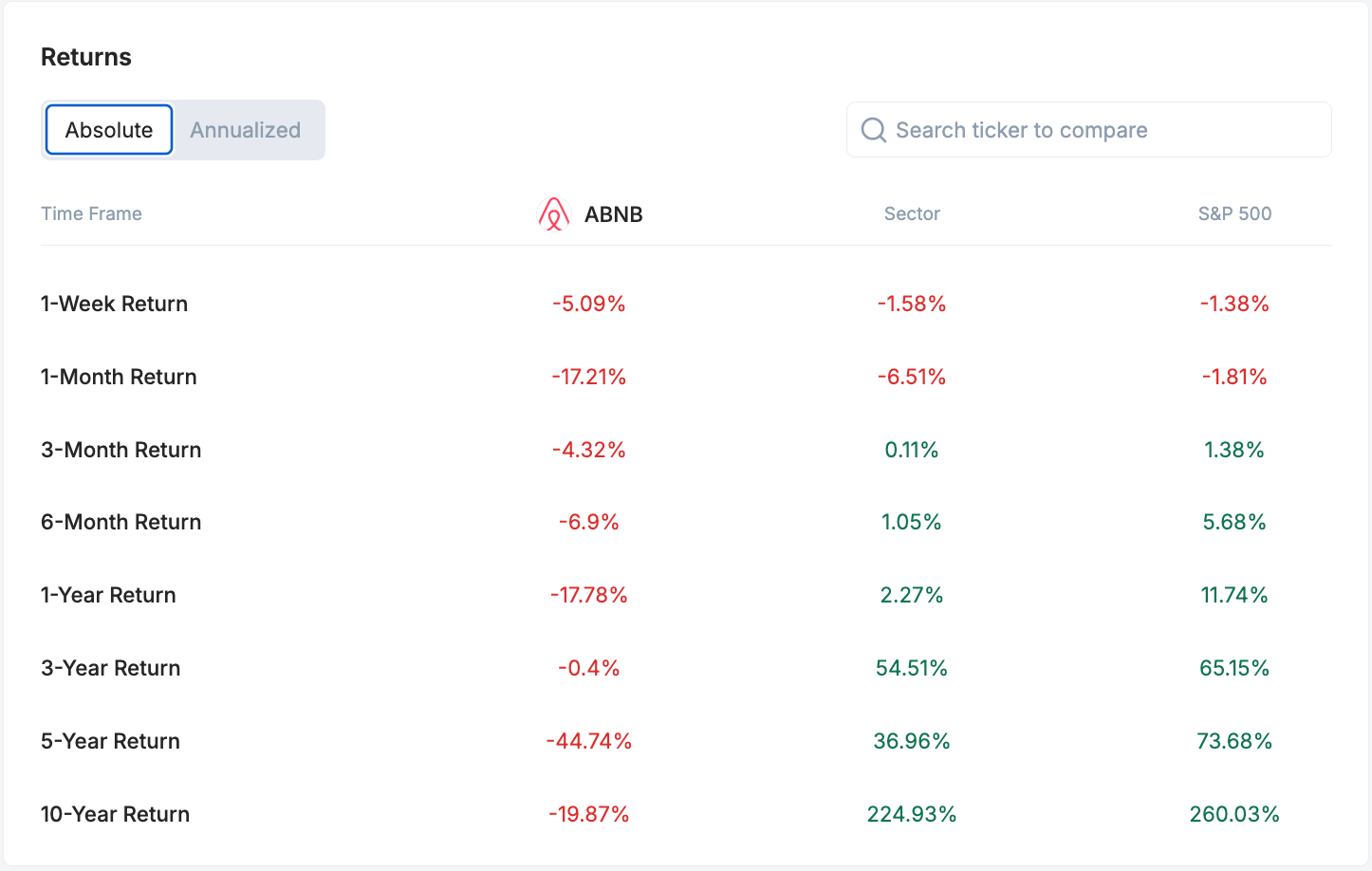

Over the past year, Airbnb shares have delivered negative returns, even as several large technology names have moved higher. Many AI-linked businesses have been re-rated sharply. Infrastructure, platforms, and software companies have seen strong capital inflows. Airbnb has not.

So the question is not whether Airbnb is growing. It is.

The real question is what the market is looking for that it is not seeing.

Is this about valuation? Growth deceleration? Regulatory risks? Competition? Or is Airbnb simply sitting in the part of the market that is steady but not exciting enough for a cycle that is rewarding acceleration?

That is what this article explores.

The business is evolving, but in measured ways

To understand Airbnb’s stock performance, it helps to first understand what kind of business Airbnb has become.

Airbnb is a transaction-driven travel marketplace. It earns revenue every time a stay or experience is booked on its platform. Unlike a subscription software company, revenue depends on travel demand, pricing, and booking frequency. That makes growth steady when travel is healthy, but rarely explosive unless there is a structural shift.

The model is effectively proven and seems to be working.

But what is happening inside the business matters more than the headline growth rate.

1. The core marketplace is stable

The primary engine remains home stays.

Nights booked grew 8 percent for the full year and 10 percent in the fourth quarter. Demand was broad-based across regions. Average Daily Rates rose modestly, helped by price appreciation and some currency effects.

The key takeaway is stability. It is now effectively operating in a normalised travel environment (unlike the COVID-environment). Growth is consistent, but it is not surging.

2. Monetization is steady, not expanding aggressively

Airbnb earns a service fee on bookings. The implied take rate in Q4 was 13.6 percent, slightly lower year-on-year due to foreign exchange and booking timing.

The company has simplified its fee structure and adjusted host fees to improve transparency. These moves strengthen long-term competitiveness, but they do not dramatically increase monetization in the short term.

This is important. The business is not squeezing more revenue out of each transaction. It is focusing on volume and platform health.

3. Expansion markets are growing faster than mature ones

Airbnb’s next leg of growth is geographic.

Expansion markets are growing roughly twice as fast as core markets. Brazil and Japan have shown strong demand. India saw origin nights booked grow around 50 percent year-on-year.

This suggests penetration is still low in many regions. The strategy is clear: localize the product, build supply, and attract first-time bookers.

However, expansion takes time. It improves the growth runway, but it does not immediately change the consolidated growth rate.

4. The platform is broadening beyond homes

Airbnb is investing in Experiences and Services to increase engagement.

A notable data point from Q4: nearly half of experience bookings were not tied to an accommodation booking. That indicates Airbnb is trying to create standalone demand beyond stays.

The company is also piloting partnerships with boutique and independent hotels in supply-constrained cities. This increases available inventory and captures demand that might otherwise shift to traditional hotel platforms.

These initiatives expand the addressable market. But today, they are incremental contributors rather than major revenue drivers.

5. AI is improving efficiency, not driving a new revenue wave

Airbnb is integrating AI into customer support and search.

A growing share of support queries are resolved without human agents. Search is becoming more conversational and personalized. These improvements reduce friction and operating costs.

But unlike AI infrastructure companies, Airbnb’s AI investments are defensive and operational. They improve margins and user experience. They do not yet create a visible new growth curve.

The picture that emerges

Airbnb today is:

- A scaled travel marketplace

- Growing at high single to low double digits

- Highly profitable with strong cash flow

- Expanding globally

- Experimenting with new surfaces like experiences and hotels

- Using AI to strengthen the core

It is a mature platform building steadily outward.

What the market is not liking

Airbnb’s business is not deteriorating. But it is not accelerating either.

Revenue is growing around 10 percent. Nights booked are growing high single digits. Guidance suggests low double-digit growth ahead. These are healthy numbers, but they look like normalization rather than a new growth wave.

In the current market cycle, investors are rewarding companies where growth is visibly accelerating, often linked to AI, infrastructure spending, or strong operating leverage. Airbnb does not sit in that bucket. It looks more like a mature, cash-generating platform than a re-rating story.

There is also the nature of the business itself. Airbnb is tied to discretionary travel. That makes it economically sensitive. Even if demand is stable today, investors know it can slow in a downturn. That cyclical exposure naturally limits how aggressively the stock is valued.

Regulation adds another layer. Short-term rentals are increasingly debated in major cities. This does not remove Airbnb’s growth, but it introduces friction and supply constraints. Markets tend to discount uncertainty, especially when it affects key urban markets.

Monetization is steady but not expanding. The take rate has been broadly stable. Fee simplification improves transparency, but it does not dramatically lift revenue per booking. Growth is coming from volume, not from pricing power or a new revenue engine.

Put together, the picture is simple.

Airbnb is executing well. But it has shifted from rebound-driven acceleration to steady compounding. When expectations were higher, that shift leads to multiple compression.

The negative returns are less about weak fundamentals and more about a market that wants acceleration and is getting stability instead.

What next, and how should these numbers be read?

The latest quarter does not alter the core narrative. It reinforces it.

Revenue in Q4 grew 12 percent year-on-year. Gross Booking Value increased 16 percent. Nights and Seats Booked rose 10 percent. Free cash flow remains strong, and margins continue to hold up. Guidance for the first quarter points to mid-teens revenue growth, helped partly by currency effects, while full-year 2026 growth is expected to remain in the low double-digit range.

These are healthy numbers. They show that demand is intact, pricing is stable, and the business continues to scale efficiently. What they do not show is a structural shift to a higher growth trajectory.

Airbnb today appears to be operating in a normalized travel environment. The post-pandemic rebound phase, when growth rates were naturally elevated, has largely passed. The company is now compounding from a larger base.

Expansion markets such as Brazil, Japan, and India are contributing meaningfully, app engagement is increasing, and initiatives in services and experiences are adding incremental activity. Artificial intelligence is improving customer support and search efficiency, but it is functioning as an operational enhancer rather than a new revenue engine.

The quarter therefore confirms stability rather than acceleration.

How one interprets this depends on expectations.

If Airbnb is viewed as a platform capable of sustained 10 to 15 percent growth, generating strong free cash flow and reducing share count through buybacks, then the numbers support that thesis. The company is disciplined, profitable, and expanding methodically.

If, however, the expectation is that Airbnb will enter a new phase of rapid expansion driven by a breakthrough product category or dramatic monetization improvement, the evidence is not yet visible in the financial profile.

For the stock to re-rate meaningfully, investors will likely need to see either a clear re-acceleration in booking growth beyond the low double-digit range, a new revenue stream such as services or experiences becoming materially significant, or sustained operating leverage that lifts margins faster than revenue growth.

At present, Airbnb looks like a durable franchise executing well within its current growth band. The business is performing. The question is whether that performance is enough in a market that continues to reward visible acceleration.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please consult a qualified professional before making investment decisions.

Note: This article relies on data from fund reports, index history, and public disclosures. We have used our own assumptions for analysis and illustrations.

Parth Parikh has over a decade of experience in finance, research, and portfolio strategy. He currently leads Organic Growth and Content at Vested Finance, where he drives investor education, community building, and multi-channel content initiatives across global investing products such as US Stocks and ETFs, Global Funds, Private Markets, and Managed Portfolios.