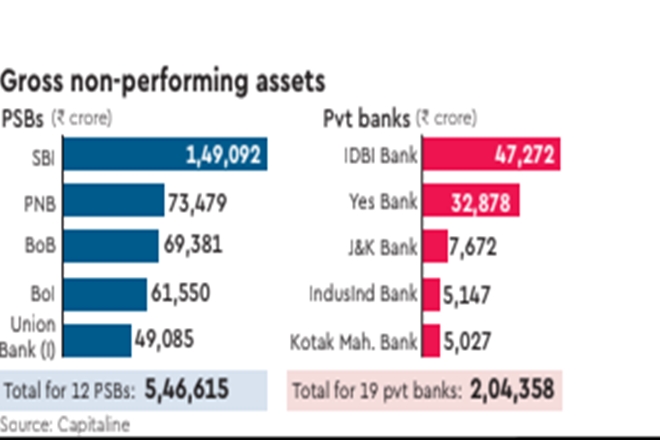

The March quarter was good for some public sector banks (PSBs), as many turned profitable after posting losses for several quarters in a row. Non-performing assets (NPAs), too, declined for most of them. Even so, the twelve public-sector banks (PSBs) recorded gross NPAs worth Rs 5.47 lakh crore, more than twice the size of the bad-loan pile of 19 private banks, which stood at Rs 2.04 lakh crore, showed data from Capitaline. The actual value of bad assets in PSBs is likely to be much higher as Q4 results for six PSBs, which were merged with other banks during the quarter, have not been made public. Almost all PSBs saw a decline in absolute GNPA numbers, with the exception of Indian Bank and Canara Bank.

The sharpest slide in NPA numbers was seen in the case of Bank of Maharashtra (BoM), Indian Overseas Bank (IOB) and Uco Bank, where NPAs fell 23%, 16% and 13% respectively. State Bank of India’s (SBI) gross NPAs fell 6.6% and Bank of Baroda’s (BoB) fell 5%. At the same time, BoB’s bad-loan portfolio shot up 44% on a year-on-year basis, reflecting the bank’s merger with Dena Bank and Vijaya Bank, and possibly foreshadowing asset quality problems in the other four banks which have been amalgamated with six others, effective April 1, 2020.

The 12 PSBs together saw a 5% sequential decline in their gross NPAs, while the private pack’s NPA pile fell 6% from the end of the December quarter. This trend may not continue through FY21 as the spread of Covid and the associated lockdowns are expected to exacerbate the stress on banks’ books. Analysts said that the pandemic could have the effect of launching a fresh cycle of bad loans in the Indian banking system. In a recent report, India Ratings & Research said the new cycle of stress could this time come from both corporate and non-corporate segments. “As per India Ratings’ analysis, COVID-19 may drive total slippages of up to Rs 5.5 lakh crore (5.7%) in FY21. The credit costs for the system could increase up to Rs 2.7 lakh crore, of which around 70% could be attributed to the PSBs,” analysts at India Ratings said, adding that if the accelerated provisioning regime is reinstated, then there could be additional credit costs of up to 0.6% for the PSBs.

Two PSBs — Indian Bank and Canara Bank — saw a sequential spike in NPAs. Indian Bank’s gross NPAs rose 2% to Rs 14,176 crore in Q4FY20. Days after the bank declared its results, S&P Global Ratings put Indian Bank on credit watch, citing deteriorating operating conditions which could lead to a higher rate of NPA formation and increase in credit costs for the bank over the next few quarters. “Moreover, we believe the merger with Allahabad Bank will be an overhang on Indian Bank’s credit profile because of the former’s sizable stock of stressed assets and weak capital levels,” analysts at the rating agency wrote, adding that the bank will continue to benefit from a very high likelihood of government support.

Canara Bank’s gross NPAs increased a little over 1% to Rs 37,041 crore. LV Prabhakar, MD and CEO, Canara Bank, told FE that the lender’s slippages in FY21 are likely to range between Rs 9,000-9,500 crore and recoveries could be in the range of Rs 9,000-10,000 crore. At the same time, the recovery expectation factors in the resolution of the Bhushan Power & Steel account, which has come under a cloud lately. The quality of Syndicate Bank’s loan book, which has been absorbed by Canara Bank, is also uncertain at present.

Some private banks, too, had a tough quarter in terms of bad-loan accretion. Mid-sized lenders City Union Bank, CSB Bank and DCB Bank saw their gross NPAs increasing between 14-20% between December 2019 and March 2020. IndusInd Bank’s gross NPA figure rose 12.4% between Q3 and Q4. The bank’s management expects a worsening in asset-quality metrics in view of the Covid-19 outbreak. Based on specific assumptions around the opening up of the lockdown, IndusInd Bank could see its gross NPA ratio rise by up to 80 basis points (bps) and credit costs increase 50 bps as a result of the spread of Covid-19, MD and CEO Sumant Kathpalia had said in a post-results interaction.