Indian pharma stocks have de-rated by 10% over the last one year, but with price erosion expected to increase, a further de-rating is expected.

Multiple triggers for further de-rating

Higher price erosion leads to lower earnings growth and returns and therefore drives de-rating. We expect price erosion to increase to 10-12% due to (i) higher competition from increasing FDA approvals; (ii) increasing channel consolidation where post Express Script joining Walgreen consortium, top three buyers now account for 90% of generic purchasing; (iii) increasing approvals of new entrants which get 30% of system approvals now.

Our assumptions are benign, could have further downside Our assumption of 10-12% price erosion factors in (i) the FDA approval rate being just equal to current filings and does not assume FDA clearing the large backlog queue of ~4000

ANDAs; (ii) we have taken only direct impact of channel consolidation, but not factored in non-linear indirect impact, as with reduced buyers 95% price erosion now could be achieved with 6+ players vs. 8+ players currently.

Stocks have not yet bottomed out; we cut earnings and multiples

We cut US multiples from 16-18x to 14-16x to factor in higher price erosion. We cut FY19 earnings for coverage by 7% average to factor channel consolidation and INR appreciation. TP for Lupin reduces to Rs1,200, DRL to Rs2,200, Sun Rs600, Cipla to Rs655, Aurobindo Rs750, Cadila Rs540 (Rs560). We stay underperform on Lupin, Dr. Reddy’s and NEUTRAL on Sun. We prefer Cipla and Cadila, with a lower base and a good pipeline.

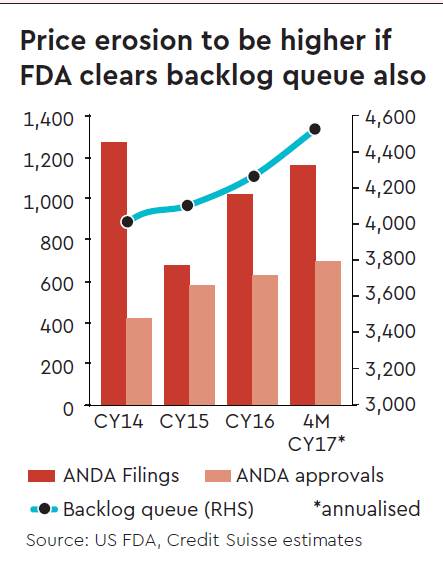

Structural concerns in US increase further

Trigger for de-rating is FDA increasing approvals by >50% over next two years: We expect ANDA approvals to increase from 650 to 1,000 in the next two years. FDA activity level is already up 35% over CY15 and FDA has fulfilled its GDUFA commitment of reviewing 90% of the backlog. However, higher activity has not fully translated into higher approvals as Complete Response Letters (CRL) picked up due to multiple review cycle. Under GDUFA II, FDA aims to convert more CRLs into approvals. The backlog queue is still large at 4,000 ANDAs but the larger problem is very high influx of ANDA submissions. In fact with more new players entering the US, ANDA filings should further increase. Therefore, the least FDA can manage is not to increase the backlog and reach approvals at least equal to the filing rate of 1,000. If we exclude first time generic approvals of about 100 a year, this amounts to ANDA approvals increasing from 550 to 900, and we expect price erosion to increase from 7-8% to 10-12%.

Price erosion could be non-linear with

increasing channel consolidation: Express Script has started participating in Walgreens consortium for generic sourcing. This implies that large buyers for generics are now down from four to three. In FY18, generic companies will get impacted from direct impact of following consolidations (i) Mckesson and Walmart (ii) Walgreens Rite-Aid merger (iii) Walgreens Prime and Walgreens OptumRx alliances (iv) Express Script sourcing through Walgreen.

The direct impact of the channel consolidation is easier to understand. It’s the indirect impact which could be non-linear. Each time a consolidation takes place, it reduces the number of slots that generic players could fight for volume share. This benefits larger generic companies but unfortunately pricing is set by the marginal player for whom R&D and capex is a sunk cost and in the process the profitability of all manufacturers gets severely impacted.