By Harsh Kumar Bhanwala & Nirupam Mehrotra

A defining feature of agricultural credit is that it is an indirect (as opposed to direct) input into agriculture, i.e. credit enables the farmer to buy inputs like seeds, fertilisers, pesticides, insecticides, etc, which has a bearing on what happens in his field and, ultimately, on his income. This criticality of agriculture credit perhaps lends it a power that no other indirect input has ever commanded.

Many a time, experts and opinion-makers have sought to attribute a one-to-one correspondence between growth of agriculture credit and agricultural production. No doubt, growth in agriculture credit is essential for supporting production, but it would be erroneous to seek a perfect correlation between the two, as agriculture credit influences agricultural production through other direct inputs.

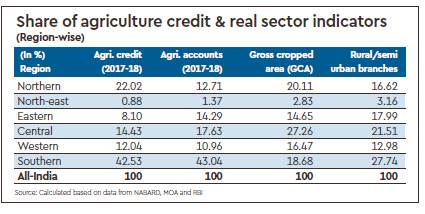

In the last decade, agriculture credit has registered a per-annum average growth of 16.5%. In terms of physical outreach, the three credit purveying agencies (commercial banks, cooperative banks and regional rural banks) have been able to add 699 lakh accounts between 2007-08 (440 lakh accounts) and 2017-18 (1,139 lakh accounts). The above aggregate numbers at the all-India level speak for themselves. However, the system needs to go up by a few notches in terms of equity aspects. The inclusiveness quotient in terms of regional distribution and connect with real sector variables can be further strengthened. For example, the five southern states together account for almost 43% of the amount disbursed and agriculture accounts. The next largest share in terms of amount is garnered by the northern region and is almost half of southern region (see table). The increased share for the southern region may be because of better infrastructure facilities, better outreach and credit delivery outlets. The skewed distribution of agriculture credit across regions is presented in the accompanying table and calls for redressal.

Economic textbook logic tells us that wherever the demand-side factors are conducive, resources (read agriculture credit) should flow towards those regions. For example, the share in credit of the eastern region is quite low compared to its share in the gross cropped area. Similar is the case with the central region. The distribution of real sector variables calls for a much better distribution of credit across regions (see table). What it indicates is the well-known reality that markets do not necessarily allocate resources optimally if left to themselves. The regional imbalance in agriculture credit has persisted for long despite the demand-side mapping reflecting a different picture. So, what needs to be done to make agriculture credit distribution more equitable?

Few suggestions

While policy stakeholders have been aware of the distortions, a more hands-on approach is required. There is a case for making concerted efforts to cover all farmers’ households within the fold of agriculture credit across regions (except southern and northern regions where the number of agriculture accounts is more than the number of farmer households). The gap between farmer households and agriculture accounts is the highest in the central and eastern regions, at 166 lakh and 152 lakh, respectively.

Fixing priority sector lending (PSL) should become a more granular exercise based on regional realities—the uniform norm of 8% credit going to small (less than 2 hectares) and marginal (less than 1 hectare) farmers under the 18% overall target of agriculture credit under the current PSL guidelines needs to be revisited and targets fixed based on regional realities. Introducing differential weight to the credit disbursed in agriculture credit-starved regions could be considered. Small and marginal holdings constitute 95%, 82% and 86% of total operational holdings in the eastern region, north-eastern region and central region, respectively, and for these regions the said target should be of a higher order.

READ ALSO | Now, get your electricity bill on WhatsApp; BSES launches new service for customers in Delhi

Digital technology has opened alternatives that can act as substitutes for brick-and-mortar branches, viz. business correspondents, business facilitators, mobile telephony technology, digital card technology, etc. Now, the policy challenge is to ensure that these interventions help leapfrog these hitherto credit-starved regions into the next league. The tendency of digital interventions gravitating towards the already well-endowed regions will accentuate the problem and runs the risk of becoming counterproductive. A similar focus should be in the case of farmers’ collectives like farmer producer organisations and joint liability groups as these help reap economies of scale both on the output and input markets and become vehicles of purveying credit to small and marginal farmers.

Digitisation of land records, which is under way in most states, needs to be completed on a mission mode in the eastern and north-eastern regions, as this can provide the much-needed reform at the bank branch level for credit expansion at a click of a button. Digitisation of land records will pave way to bring vibrancy in developing a land lease market.

The government has embarked on an emphatic initiative to complete the identified irrigation projects in a time-bound manner providing irrigation facility to 80 lakh hectares. This shall increase the credit absorption capacity in the command areas of these projects. To hasten the credit flow in these areas, banking plans are required under an ‘area development’ approach. The impact of public infrastructure creation in rural areas, be it irrigation, connectivity, health, sanitation or education, on enhancing credit absorption capacity and expenditure pattern is a proven one. In the credit-starved regions, rural infrastructure creation needs to be dovetailed with the small area-based plans for various agriculture investments including devices for efficient use of water, electricity and solar power that require bank credit and get the banks on board for these plans.

Agriculture credit has, over the last few years, won the battle of ‘growth’—the cake has grown bigger—but it still has to get the distribution aspect right. This is the immediate unfinished agenda of ‘agriculture credit in India’, which requires focused attention from all the stakeholders.

Bhanwala is chairman, Mehrotra is a senior officer, NABARD. Views are personal