On at least three occasions earlier this year, these columns have suggested the corporate tax rate be hiked. So, it is flattering to note that Anantha Nageswaran, member of the Prime Minister’s Economic Advisory Council, feels the same way. The move to lower the rate to 22% plus cesses was always ill-advised; the sharply lower rate was supposed to attract truckloads of investment and create thousands of jobs, but nothing of the sort has happened.

On the contrary, fat-cat corporations and banks that were, in any case, raking it in, pocketed the gains. CRISIL estimated at the time, based on estimates for FY19 profits-before-tax (PBT), the top 1,000 companies collectively reaped a windfall of Rs 37,000 crore.

These columns also observed on June 1 that it is inconsiderate—to put it mildly—of the corporate sector to call for government stimulus without even offering to contribute. This, in a year in which it has raked in such phenomenal profits even as the economy contracted some 7.3%, the worst performance in decades. For perspective, just as the earnings season is ending, India Inc (a sample of 1,022 companies including banks and financials) has reported a phenomenal net profit of Rs 5.45 lakh crore; that is a jump of 56% over profits the previous year. The increase in the PBT is an even more impressive 61%, clocking roughly Rs 8 lakh crore.

The profits have resulted not merely from better sales growth—in fact, the aggregate sales are down 2.44%—but also from huge cost-cuts. Expenditure was slashed by some Rs 4.2 lakh crore at a time when commodity prices are elevated. Going by the cash levels, it doesn’t seem like companies are scrounging for profits. The combined free cash-flows of three two-wheeler players was Rs 8,300 crore while ITC’s free cash-flows are nudging Rs 10,000 crore. Little wonder, interest costs came off by 5%.

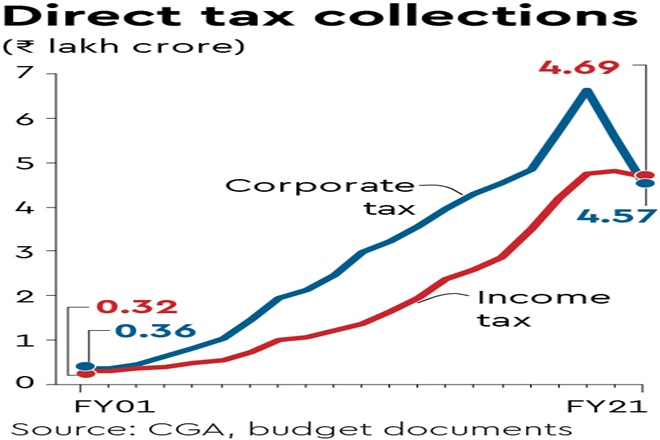

Also, more pertinently, the tax bill fell by a whopping 32% and there is no base effect here. As is known, collections from corporation taxes in FY21, at Rs 4.57 lakh crore, came in lower than the Rs 4.69 lakh crore from personal income taxes. Also, indirect taxes, as a share of GDP, stood at 5.46%, higher than the share of 4.79% for direct taxes, partly because of the very stiff duties on auto fuels. However, economists always prefer a higher share for direct taxes, and this is a good time for the Union government to rethink corporation taxes. Even a retrospective tax for FY21 would not be out of place.

The point is that the broader economy needs support. To be sure, it is the government’s responsibility to stimulate demand and to take care of the vulnerable sections of the population that need income support. The thousands of MSMEs, especially the smaller units, need assistance to be able to stay in business. While RBI has come up with several credit lines for banks, at very affordable rates—it did so even last Friday—banks have not been too keen to lend. Their profits continue to soar in a year in which loan growth collapsed to multi-year lows. For the banks and financials in the sample, profits went up 18%, but corporate credit for FY21 was virtually flat. Most of the corporate lending has happened in the corporate-bond market, directed at the better-rated companies.

Rather than take on any risk, banks are content to mop up cheap deposits and park them with RBI at 3.35%. It is hard to understand why RBI needs to incentivise them to lend to healthcare—in the midst of a pandemic—as also to lend to contact-intensive sectors. State Bank of India’s advances went up by a measly 5% last year, but the lender’s profits soared 41% to Rs 10,400 crore. At Kotak Mahindra Bank, the loan growth for the year was just 1.8% while the net profits were up 17%.

Thanks to their finance muscle, the larger companies were able to restore supply chains fairly quickly once the lockdown was lifted last year and, thus, were back in business by about September. In contrast, the smaller enterprises—most of these being in the unlisted space—were unable to recover as quickly and lost market share. As is known, a much bigger percentage of MSMEs opted for the loan moratoriums last year than bigger firms.

Nowhere is the disparity between the formal and informal sectors seen more starkly than in the GVA; India’s GVA contracted 6.2% in FY21 while the proxy for India Inc’s GVA—the sum of the ebitda plus employee expenses—went up by a remarkable 18%. The variance could be even higher when the numbers are revised, given the data initially capture more of the organised sector’s performance than that of the unorganised sector. The government’s total revenues (including disinvestment proceeds) for the current year are likely to fall short by more than Rs 1 lakh crore; the deficit could also be wider than Rs 15.06 lakh crore if it spends as budgeted. A hike in corporation taxes could ease the pressure.