Rarely has there been as much anticipation of an Indian Budget as this year. This is surprising because, being an election year, the government simply presents a Vote on Account or an interim Budget seeking parliamentary approval for grants typically for just four months of the next fiscal year, before a full Budget is presented by a new government in July.

Interest, however, stems from the current macroeconomic backdrop. With states’ deficits rising, GST collections under pressure, and India’s total public sector borrow requirement at a hefty 8.2% of GDP in 2017-18, all eyes are on whether the Centre can keep to its budgeted consolidation for 2018-19 and, if so, whether the quality of consolidation will be compromised by having to cut capital expenditures. Further, perceived distress in both agriculture and SME sectors has increased pressure on authorities to announce some sort of “agrarian package” or a quasi-universal basic income potentially involving cash transfers, as well as palliatives for the SME sector. All this could put pressure on next year’s deficit. Against this backdrop, this piece raises five questions to help navigate India’s Budget and what one should monitor on February 1.

1. Will the government meet its 2018-19 fiscal deficit target and, if so, how?

We expect authorities will do what it takes to either meet the budgeted central deficit target of 3.3% of GDP or come close to it. Having overshot (albeit modestly) last year’s deficit target, and with bond and currency markets exhibiting nervousness, we believe policymakers will want to reassure markets on the sanctity placed on fiscal targets.

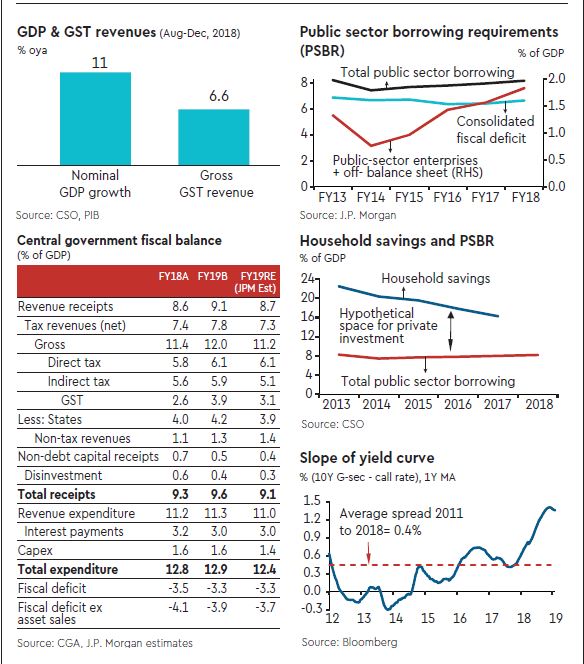

The fiscal challenge this year is real. We had worried on Budget day itself last year that GST revenues had been budgeted too ambitiously and, unfortunately, this has come to pass, compounded by repeated tax cuts by the GST Council in 2018-19 and patchy GST compliance. Aggregate GST revenues have only grown by 6.6% over year ago between August and December, much below nominal GDP growth. We expect gross GST collections to be short by about 0.8% of GDP. However, because 42% of the divisible pool goes to the states, the net impact on the Centre will be close to 0.5% of GDP. We also think the asset sales (disinvestment and telecom spectrum) target of 0.6% of GDP will be challenging to achieve given the current run-rate. All told, we expect revenues to be about 0.5% of GDP lower than budgeted, and this presumes an interim dividend from RBI to the tune of 0.2% of GDP.

However, we expect adjustments will be made on the expenditure side. Because expenditure was slashed in the last few months of the last fiscal, the budgeted expenditure growth was not as austere as initially believed. Instead, de facto budgeted expenditure growth is a healthy 14%, and expenditures are running much below that target. In other words, there will be expenditure savings to offset revenue challenges. That said, capital expenditure growth is running at only 4%, and the worry is budgeted capex will be a casualty of this year’s deficit.

The good news is we expect policymakers will stick to the 3.3% of GDP target or come very close, and that this will calm markets. But there are two challenges: (1) GST revenues remain anaemic; and the (2) quality of the fiscal consolidation will be imperilled by capex having to bear the brunt.

2. Will the 2019-20 Budget continue with consolidation?

We believe the 2019-20 Budget will continue with modest fiscal consolidation, targeting a deficit of 3.1% of GDP (or very close to that) in line with the FRBM Review Committee’s recommendations. To be sure, the assumptions of the interim Budget are less binding because they will be revisited when a full Budget is presented. Yet it would be important to analyse what tax buoyancy has been budgeted for 2019-20. With GST revenues sharply undershooting, tax buoyancy is expected to be just 0.9 in 2018-19 compared to 1.2 in 2017-18. We expect measures to improve GST compliance after the election. Notwithstanding that, we think a buoyancy much above 1.1-1.2 would be challenging to accomplish.

On the expenditure side, the key is whether any new “agricultural package” is announced and how it will be financed. Will it partially replace existing welfare programmes, or will new measures of revenue be sought or does it risk creating a new, unfunded liability? Finally, the fiscal wild-card for 2019-20 is whether the government will be recipient of any “excess capital” from RBI’s balance sheet and whether this is used to retire public debt, recapitalise public sector banks or finance new spending on the budget.

3. How should one evaluate the announcement of an agricultural package and/or cash transfers?

Markets are ripe with expectancy that authorities are on the cusp of announcing an “agricultural package” potentially involving cash transfers to constitute a basic income for the rural economy. Any such package would need to be assessed on five dimensions:

n Who is it targeting? Will this be directed just towards farmers? Or the rural economy more broadly? Or even the urban poor? The more targeted it is, the more fiscally viable it will be. Equally, however, the greater the targeting, the greater the chance of exclusion errors (intended recipients being left out) or inclusion errors (unintended recipients being included). Hence the temptation to quasi-universalise. But that must be traded-off against fiscal viability.

– What is the quantum of the cash transfer? If directed to farmers, this will likely be a biannual payout like Rythu Bandhu scheme in Telangana. If this is meant to be a basic income for the rural economy, there will be a monthly pay out. What will that quantum be and how will it be indexed?

– Will any cash transfer be unconditional or contingent (on land holdings, for example)? Any payout on land holdings (per hectare, for example) will be regressive (disproportionately benefiting rich farmers with larger holdings). It may also distort the decision of a small farmer to sell the land and move out of agriculture to higher value-added manufacturing/ services, which must be the goal.

– How quickly can it be rolled out? Financial inclusion has improved. But is last-mile connectivity in place? Do the most needy and marginalised have operational bank accounts to receive and access such a transfer? How long will it take to ensure the financial infrastructure is actually working?

– How will this be funded? This will be the key question that markets will likely focus on. Will an agricultural package replace or subsume exiting programmes? Will new sources of revenue be sought?

4. What net and gross borrowing can markets expect?

Under our assumption of a fiscal deficit of 3.1% of GDP, we expect net market borrowing to amount to Rs 4.2-4.4 trillion. This assumes the proportion of the deficit that is financed by market borrowing remains (at a relatively low) 66%. There are also large redemptions next year to the tune of Rs 2.4 trillion. However, we expect the government will undertake “switches” of about Rs 400 billion before the end of this fiscal, such that redemptions for 2019-20 are brought down to Rs 2 trillion. We expect gross borrowing to be in the range of Rs 6.2-6.4 trillion—or about 3% of GDP.

5. (Don’t miss the forest for the trees) What is India’s public sector borrowing requirement (PSBR)?

Even as markets continue to obsess about the Centre’s fiscal stance, we have maintained that is to miss the forest for the trees. The fiscal centre of gravity has moved to states, whose combined expenditure is much higher than the Centre and whose combined fiscal deficit has increased over the years, offsetting the Centre’s consolidation. If one were to add off-balance-sheet borrowing (by FCI, for example) and borrowing by CPSEs, the total PSBR for India remained a hefty 8.2% of GDP—a level at which it has been close to for five years. Note this estimate is a “floor” because it does not include borrowing by state PSEs, including state electricity distribution companies.

A lot of the borrowing—particularly by states and CPSEs—is to finance much-needed capex. But a PSBR of this quantum—sustained for several years—constitutes a large claim on domestic household financial savings, which have fallen in recent years from 22% of GDP to 16%, and likely explains why the slope of India’s yield curve has steepened.

A PSBR of such quantum is perhaps rationalisable at a time when private investment has been depressed. But if private investment were to pick up—as is hoped—it would need to be accommodated by the public sector reining itself in. Else, borrowing costs would rise sharply—and crowd out some private activity—or India’s CAD would swell, and private investment would need to be financed by (more risky) foreign borrowing, at a time when global interest rates are hardening, and uncertainty and volatility remain elevated.

(Excerpted from JP Morgan Asia Pacific Emerging Markets Research dated January 30, 2019. Views are personal)