and retain our Buy rating on PLNG as it is well placed to benefit from any increase in gas demand in the country in our view.")

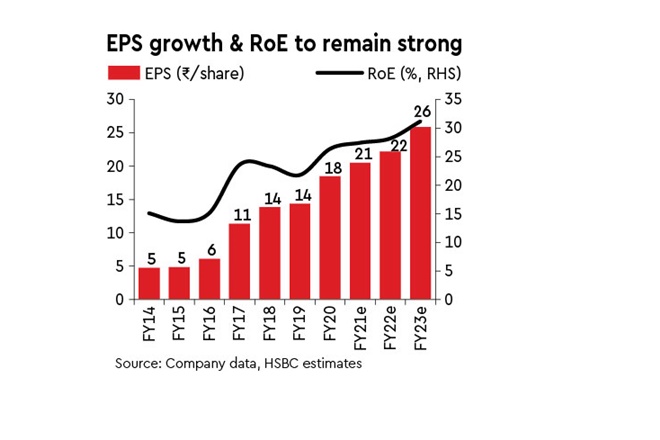

We expect near-term growth to pick up with the Kochi Mangalore pipeline now commissioned which will open up new customers. Interestingly, the price of newly discovered domestic gas is linked to the global LNG price. With global LNG prices falling (and likely to remain weak), crude prices continuing to rise and economy recovering rapidly, we expect LNG offtake to increase in India during FY22. We estimate this will drive 8% and 17% earnings growth for PLNG in FY22 and FY23.

Longer-term growth pipeline is still a work in progress

While PLNG continues to evaluate new terminals in Sri Lanka and the East Coast of India, big capacity growth plan is still some distance away. However, PLNG has some relatively easier growth planned with an increase in capacity at Dahej (by virtue of additional terminals and jetty) which should position it once again as one of the lowest-cost re-gasifiers in a region that has the potential for more gas demand. We still assume Kochi utilisation at 30% in FY22 and peak utilisation at 50% as uncertainties on tariffs still remain but we also see upside risk to utilisation as connectivity is finally available.

In the interim, it remains a cash-generating machine

Even as PLNG has c`50 bn of cash (c14% of market cap) as of Sep’20, it continues to generate cash with a c10% FCF yield. Consequently, we expect the company to pay out a significant dividend at a 7.2% dividend yield in FY22 even as capex gradually scales up in FY22. We believe this will provide significant downside support to the stock price. While investors worry about potential return on deployment of cash, we are more confident given its recent assessment of deals and increased dividend pay-out.

Valuations are undemanding

We lower our earnings estimate by 5-7% in FY22/23e to factor in a more conservative utilisation and tariff for Kochi pending its tariff negotiation. An Rs 10/mmbtu decrease in the Kochi tariff can reduce the company’s valuation by 3% and a 10% increase in the utilisation rate can increase the valuation by 3%. We value the company on a DCF of individual terminals to arrive at target price of Rs 290 (earlier Rs 300) and retain our Buy rating on PLNG as it is well placed to benefit from any increase in gas demand in the country in our view.

PLNG is trading at FY22e PE of ~11x, a 20% discount to its 10-year historical average. Catalyst: Increased utilisation of Kochi terminal should drive up both earnings and the PE multiple. Key risks are sharp increase in domestic gas production, sharp cut in Kochi tariffs and ROE-dilutive capex.