In Q3FY21, HDFC Bank (HDFCB) reported net profit growth of 18% y-o-y to `87.6 bn (20% ahead of our estimate). Led by stable loan growth (16% y-o-y) and NIMs (up 10bp q-o-q at 4.2%), improving fee income profile (up 10% y-o-y), and low cost-to-income (36% vs 39% in FY20), operating profit grew by 17% y-o-y. Gross NPA (on a pro forma basis) remained stable q-o-q at 138bp, net NPA was up marginally (at 40bp) with strong provision cover of 86%. Disclosures on RBI resolution book and portfolio quality suggest a stable asset quality outlook.

Outlook on asset quality stable: In Q3FY21, pro forma GNPA remained stable at 138bp (vs 137bp in Q2). There was a marginal increase in pro forma Net NPA (40bp in Q3 vs 35bp in Q2). Annualised slippage ratio, on a pro forma basis, was at 1.86% vs 2.3% in Q2. The bank disclosed that restructuring under RBI resolution framework for COVID-19 was c50bp of total advances. Demand resolution improved from 95% in Q2 to 97% in Q3. Commentary on portfolio quality indicates stable asset quality performance. The bank is carrying additional floating and contingent provisions at c93bp of loans.

Operating performance resilient: In Q3FY21, wholesale loans (up 26% y-o-y) continued to support loan growth (15% y-o-y). Retail loans were up 5% y-o-y, with growth in personal loans (up 5% y-o-y) and credit cards (up 11% y-o-y) slowing down. CASA deposits (up 30% y-o-y) outpaced deposits growth (19% y-o-y). NII grew by 15% y-o-y.

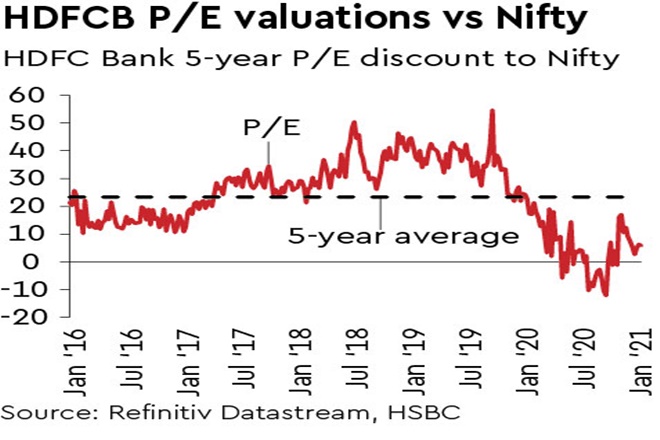

Buy – Accelerated market share gain with controlled quality and costs: Our FY21-23 estimates are revised marginally on back of lower credit costs assumptions. HDFCB is advantaged by its investment in distribution, lower cost of operations and funds, and clean underwriting track record. With falling RWA intensity along with improving operating profitability, HDFCB is a leader by some distance among its peers on RoE. Our TP of Rs 1,680 (vs Rs 1,660 earlier) implies 22x 1-yr fwd EPS for forecast average FY22-23e RoE of 18%. On a P/E basis, HDFCB is still trading below its historical premium/ discount to NIFTY valuations.