too met with a disappointment.")

HCLT has reported disappointments across the board – revenue growth, margins and outlook. Organic growth (+1.6% q-o-q, CC) was tepid and in line with a typical March quarter even before the pandemic. Like TCS and Infosys, muted growth in Mar-21 further strengthens our anti-consensus argument that industry growth rates are unlikely to accelerate going forward (vs pre-Covid). Both revenue growth and margin guidance bands are unusually abstract and underwhelming.

It should be noted that HCLT was one of the very few companies that came out with definitive guidance bands in Jun-20 amidst peak Covid uncertainty. In that context, the street is unlikely to take much comfort in strong deal wins, also given the limited causal relationship here. Impact of the proposed investments on deal wins and subsequent period growth will be keenly tracked. Expectations around articulation of a formal capital return policy (like TCS & Infosys) too met with a disappointment.

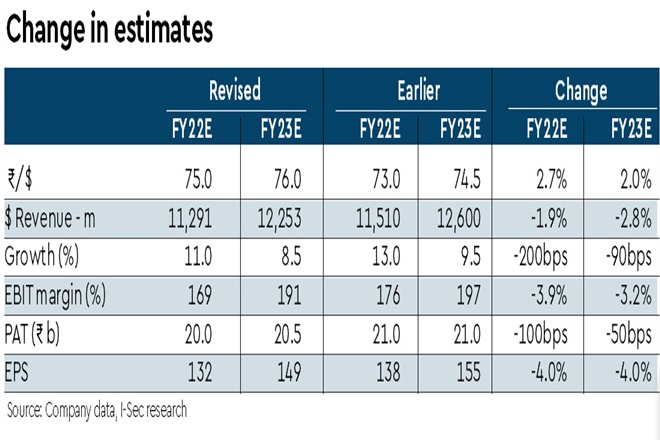

As we revisit growth, margin and ETR assumptions, FY22-23e EPS witnesses a ~4% downgrade notwithstanding INR depreciation benefit. We cut our TP by ~8% now implying a lower target multiple of 19x FY23e EPS. We downgrade the stock to Add (from Buy earlier).

Disappointments across the board: Revenue missed our/consensus estimates. Seasonality in Products & Platforms (-4.9% q-o-q, CC) was the key overhang on growth. In addition, elusive recovery in ER&D business (+0.7% q-o-q, CC) was another dampener. In IT & Business Services, organic growth (+3.2% q-o-q, CC) was in line with a typical March quarter adjusted for a bit of base normalisation seen during the recovery leg.

Adjusted for a one-off special bonus to employees (-370bps q-o-q impact), EBIT margin was 90/210bps behind our/consensus estimates. Residual wage hikes (- 60bps impact), seasonality in Products & Platforms (-70bps impact), fresher hiring (- 60bps impact) and INR appreciation (-20bps impact) were the key margin movers. In addition, impairment charge related to a couple of products led to significant Ebit margin compression in P&P segment (980bps to 20.8%).

Guidance signals weaker confidence: Both revenue and margin guidance are unusually abstract and underwhelming. While the company reported strong deal wins (TCV of $3.1 bn), the street is unlikely to take much comfort given the limited causality on growth in subsequent periods. Notwithstanding INR depreciation benefit, we cut our TP by 8% implying a lower target multiple of 19x FY23e EPS.