Coal India’s (COAL) Q4 numbers disappointed on lower ACQ realisation. Ebitda (ex-OBR) of Rs 62.1 bn (down 11% y-o-y) was below est. of Rs 68.2 bn on 5% miss to our ACQ realisation estimate. PAT of

Rs 42.4 bn (flat y-o-y) benefited from lower tax rate (33% v/s. 39% in Q4FY15) partly offset by 7% y-o-y lower other income.

Realisation: ACQ NSRS declined 5% y-o-y to Rs 1,350/ton mix (power volumes were higher) and incentives. E-auction NSR declined 12% q-o-q to R1,648/t.

Volumes: E-auction volumes were up 47% y-o-y to 20.4mt aided by sales from the custodian Gare-Palma blocks (2.3mt). ACQ vols. were up 3% y-o-y (to 119mt).

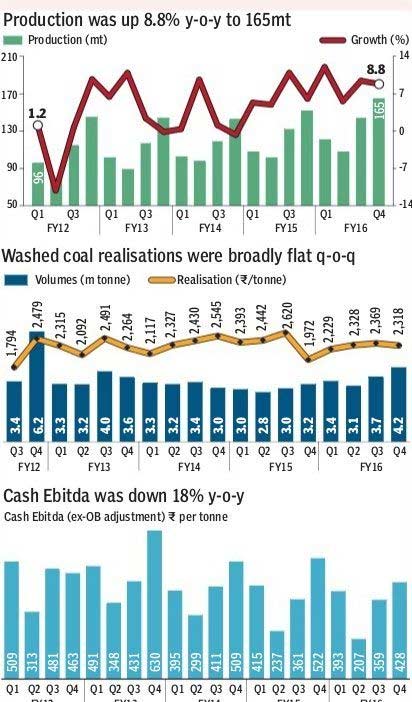

Cash cost (ex-OBR) per ton was down 3% y-o-y to R1,002/ton benefit of operating leverage and benign inflation. Costs also included provision of Rs 7.1 bn relating to overdue debtors. Ebitda (ex-OBR) per tonne was down 18% y-o-y to Rs 428/t.

Price hike after three-years: COAL announced blended 6.3% increase in notified price of coal. Notified prices for higher grade (G1-G4 grade) were cut substantially (Rs 500-1,300). Prices of lower grades (G5-G13) were increased by Rs 100-300. Average price hike for power sector is 7.5-8%. For non-regulated sector, the impact is negated by cut in notified price premium from 35% to 20%.

Upgrading FY17E adj Ebitda but keeping FY18e unchanged; Valuations attractive

We are upgrading FY17e adj. Ebitda (ex-OBR) by 8% to Rs 196 bn to account for price hike w.e.f. May 30, 2016 (earlier April 1, 2017). We believe that price hike will offset upcoming wage hike. Despite weaker demand, aggressive production growth target is putting pressure on E-auction prices. Valuations are already factoring in negatives as it is trading at attractive FY18e EV/Ebitda of 5.7x. Maintain Buy.

Coal India has demonstrated that it is able to achieve strong volume growth and has addressed issues related to land acquisition and evacuation bottlenecks. The stock (adjusted for dividend) has got de-rated and corrected by 30% from its peak of Rs 445 on concerns that it will be difficult to achieve price hike.

The value of stock has very high leverage to market prices of coal. When prices are high, Coal India is able to (i) substitute imports at a faster rate, (ii) push more volumes into domestic market, and (iii) benefit from operating leverage and higher prices in E-auction. This works otherwise when the prices are weak, as is the present situation.

We believe that international coal prices have limited downside because current market prices are hurting production in both Indonesia and USA, among the key coal exporters in the world. The stock is trading at an EV of 6.9x FY17e Ebitda and 5.7x FY18e Ebitda. Valuations are attractive for a growing mining company, despite challenging market conditions. We value Coal India at R370/share based on EV/Ebitda of 7.5x FY18e. Maintain Buy.

—Motilal Oswal