for Q4FY20 stood largely flat y-o-y.")

CDH is on track to implement a two-pronged strategy: (a) renew focus in DF by regrouping it into the Mass and Specialty segments; and (b) differentiated launches in US Generics. We maintain our EPS estimates for FY21/FY22e and continue to value CDH at 21x 12M forward earnings to arrive at TP of Rs 420. We remain positive on CDH on account of better prospects in DF (encouraged by changed strategy), a healthy ANDA pipeline (including injectables and transdermals) in the US market, and regulatory works at Moraiya nearing completion. Maintain Buy.

Performance in line with estimates

CDH’s sales at Rs 37.5 bn (in line) for Q4FY20 stood largely flat y-o-y. US sales (47% of sales) fell 1.9% y-o-y to Rs 17.6 bn. The India Branded Formulations business (24% of sales) was Rs 8.9 bn, almost flat y-o-y. EM and LATAM (5% of sales) revenue was down 17% y-o-y to Rs 1.7 bn, while API registered strong growth of 21% y-o-y, with sales of Rs 1.2 bn. The Consumer Wellness business grew 21.8% y-o-y to Rs 4.9 bn (13% of sales).

Gross margin at 66.4% expanded 350bp y-o-y owing to a superior product mix. However, the Ebitda margin contracted 140bp y-o-y to 21.1% for the quarter, weighed by higher other expenses (+200bp y-o-y), R&D expense (+160 bps), and employee cost (+140bp y-o-y). These costs were largely attributed to the integration of the Heinz business. Ebitda at Rs 7.9 bn (in line) was down 5% y-o-y.

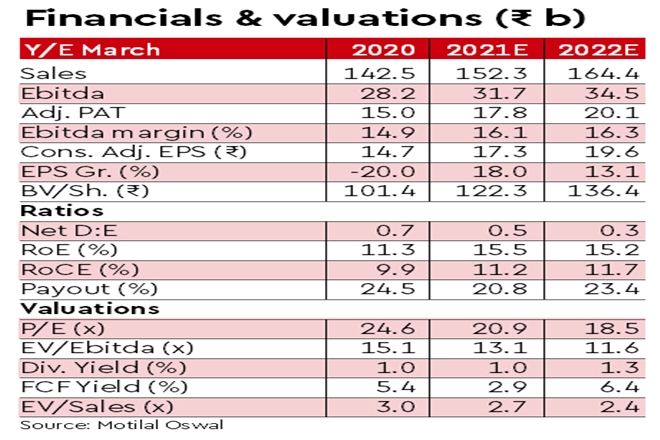

Impairment charge (Levorphanol/ goodwill in Windlass) was Rs 525 m. Adjusting for the same, PAT was down 12% y-o-y due to higher depreciation. For FY20, revenues were Rs 143 bn, up 8.3% y-o-y. Ebitda/adj. PAT was at Rs 28/15 bn, down 6.5%/20% y-o-y.

Highlights from commentary

CDH launched 6/34 ANDAs in Q4FY20/FY20. The Mass/Specialty segment formed 55%/45% of the DF business. CDH intends to increase: (i) penetration in the Mass segment; and (ii) detailing to key opinion leaders in the Specialty segment. Price erosion is down to low single digits in the US. CDH did not benefit from the panic buying witnessed in the US. It reduced its net debt by ~Rs 5 bn in FY20, and plans to further reduce it by Rs 8.5-10 bn in FY21. COVID-19 related disruptions impacted the business by 2.2 bn.

Valuation and view

After exhibiting y-o-y earnings decline in FY20, we expect CDH earnings to be back on the growth path (16% earnings CAGR over FY20–22), led by gradual recovery in US sales and improving growth in DF, with renewed strategy, better operating leverage in Consumer Wellness, and reduced financial leverage. We continue to value CDH at 21x 12M forward earnings to arrive at TP of Rs 420. Maintain Buy.