While owning a home is typically the dream of every Indian, sky-rocketing property prices especially in metros have led people to opt for renting rather than buying. However, for people who can afford to buy a house, the choice between buying and renting is always a tough one. In the Indian context, it is observed that people who can afford to buy a house tend to put more weightage on owning a house and renting is mostly a compromise. There are definite advantages and disadvantages of both the options, and some of the advantages are summarized as:

Advantages of owning a home over rental accommodations:

# It gives a sense of security and pride of home ownership.

# Rent is an expense that is incurred every month without creating any physical asset. Paying EMI, however, has dual benefits; it not only provides for a one month of shelter, but also increases the proportional ownership in the house.

# With renting you often have to relocate which entails a lot of wasted time, money and energy, but that is not the case with owning.

# Real-estate investment is a safe investment backed by a real asset which has potential of capital appreciation and tax benefits.

Advantages of renting:

# Renting does not overburden one with EMI payments, house tax and other legal issues that are part and parcel of property ownership.

# Renting generally gives a feeling of lower liability. In metro cities you can rent a house worth Rs 50 lakh for only Rs 10,000-15,000 a month. At the same time, if you buy a home at the same cost, you have to shell out anywhere from Rs 30,000 – 40,000 as an EMI (equated monthly installment).

# One can rent closer to work or closer to good schools, but the same properties may or may not be affordable or within one’s budget.

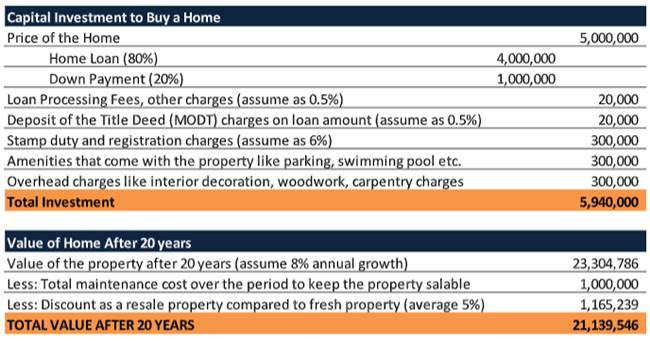

The choice between renting and owning is a tough one. Only a careful analysis would help one to reach a proper conclusion. Let’s try to understand the financial implication of renting vs owning through an example of a person who wants to own a property in the NCR region. The first step is to calculate the capital needed to buy a ready-to-move-in flat in Delhi/NCR in a residential project assuming the market price is Rs 50 lakh. The down-payment and associated transaction costs have to take care of upfront, the following table lists all the costs associated with a property purchase.

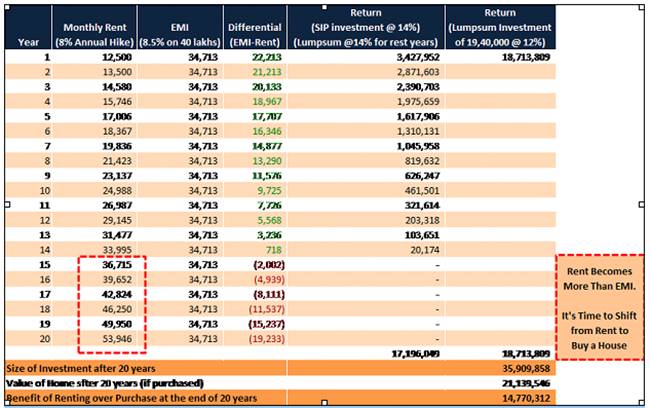

From the above table, it is clear that a capital outlay of Rs 5,940,000 is required to own a property in the NCR region. After 20 years your investment value would be Rs 21,139,546 considering an 8 per cent annual appreciation in home prices after accounting for all the maintenance and transactional costs over the entire duration. To compare owning vs renting, the first step is to calculate the investment returns on the down-payment and other related costs that one incurs upfront while buying the house. The second step is to calculate the investment returns of the difference between the EMI payments and the rent over the entire duration of ownership. The down payment for the house is Rs 10 lakh and other capital outlay is Rs 9.4 lakh. Therefore, the total onetime lump-sum capital outlay is Rs 19.4 lakh. In this example, the returns on the lump-sum investment are assumed to be 12% and the returns on the monthly investments are assumed to be 14%. At the end of twenty years if one opts for renting, he/she would have accumulated Rs 3.59 crore, which is approximately Rs 1.5 cr higher than the value of the property at the end of the 20 years as shown in the table below:

It is amply clear from the example that renting turns out to be a better option. However, this may not be true in all market conditions. Indian real estate market is going through a period of slump with all major metros and Tier-I cities showing softness in property prices. For homebuyers who are interested in owning a house, it is recommended that unless they are buying a house for primary residence, investment in real estate at this point does not make sense. The return or efficacy of owning vs renting is largely dependent on market conditions. In rapidly-rising real estate markets, owning makes more sense. On the other hand, when there is not much room for property price appreciation, renting is perhaps a better option.

(By Rahul Agarwal, Director, Wealth Discovery/EZ Wealth)