Revenues grew by 24 y-o-y to Rs 5.7 bn (est. Rs 4.6 bn) aided by Rs 1 bn income from land monetisation. Adjusted for this segment, revenues were in line with estimates.

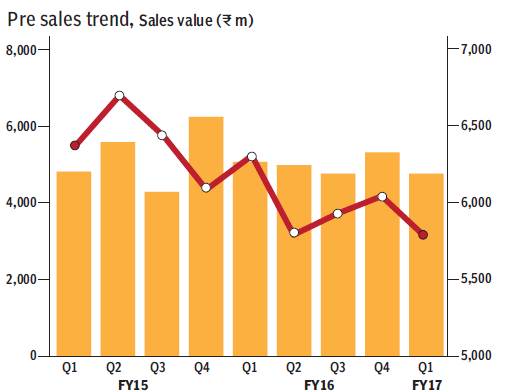

Contractual revenues grew 28% to R1.71 bn ahead of estimates of Rs 1.46 bn. For Q1FY17, Sobha reported 0.8 msf (4% lower y-o-y) and Rs 4.7 bn (down 6% y-o-y) of pre-sales. Subdued performance was on account of delay in new launches in Non-Bangalore markets and soft demand in its traditional Bangalore projects. Ebitda came in at R1 bn (down 23% y-o-y) vs est of R1.2 bn.

OPM was down 1000 bps y-o-y to 17.5%. OPM was impacted by 12.3% profit contribution from land monetisation revenue as well as higher component of construction business. Reported PAT of Rs 359 m was below our estimate of Rs 426 m. During the quarter, Sobha reported q-o-q debt reduction of Rs 342 m. The debt decline was driven by Rs 400 m proceeds from land monetisation transaction.

Key positives: Higher construction revenues; net debt reduction.

Key negatives: Lower margins; weak pre-sales.

Impact on financials: We lower our FY17/18 earnings by 12%/3%.

Valuations & view: Sobha’s pre-sales run-rate and cash collections have been sluggish for many quarters and we see limited signs of a material revival in the near term. This has also steadily increased leverage on the balance sheet and return ratios. Though recent entry into the aspirational home segment will boost volumes, the impact on cash flow/pre-sales will be muted unless Sobha is able to replicate this strategy across multiple locations. Given the lack of near-term triggers and muted visibility on new launches, we maintain Underperformer with a TP of R301. Faster monetisation of its legacy land bank is a key risk to our call.

Other highlights: During the quarter, Sobha sold 0.81 msf with a sales value of Rs 4.7 bn. Average realisation fell by 3% y-o-y led by change in product mix. Sobha’s run-rate has been stuck in a narrow band of 0.8-9 msf over the last several quarters now. Company’s FY17 guidance of 3.5 msf/Rs 20 bn is also largely in line with this run-rate which is indicative of management’s caution and doesn’t give too much comfort on a material turnaround in the company’s growth trajectory anytime soon.

In general, management expressed optimism in the improvement in the pace of approvals across different locations including Chennai. This should aid new project launches. Management has guided to 9.1 msf worth of new project launches over next 4-6 quarters.

Reported Ebitda margins came at R17.5% and margins, adjusted for the land sale revenues, were 20%. Ebitda (adj for R130m contribution from land sale) came at Rs 860m — sharply below estimates of Rs 1.22 bn. The company ascribed the Ebitda miss partially to the higher sales and marketing expenses.

In terms of cashflow, Sobha collected Rs 5.8 bn (flat q-o-q) during the quarter (including contractual collections of R1.67 bn), with R4.4 bn incurred for operational expenses, thereby generating

Rs 1.4 bn of operational surplus.

Post interest payment (R606m) and taxes (R107m), cash flow was a positive Rs 714 m. During the quarter, the company spent Rs 310 m for capex including land acquisition. Hence, Sobha generated total positive FCF of Rs 342m, resulting in marginal decrease in net debt.

Notably, Sobha received R400m of cash from the land sale transaction; therefore adjusted for this cash income, the business hardly generated operational cash flows despite limited capex/land acquisitions spend. At this level of operations, Sobha will not be able to aggressively invest in further land acquisitions without straining its balance sheet.

Sobha’s net debt stood at R20.25 bn (from R20.6 bn in Q4FY16) with D/E ratio of 0.78x. Given limited land payments/ capex in FY17, company sees debt reduction in FY17. Cost of debt stood at 11.6% in Q4FY16 and is down 100 bps y-o-y. The company sees scope for further reduction in the interest rates.

Sobha had announced buy-back of Rs 750m (2.3 m shares, 2.3% of current equity) by way of tender offer at price of Rs 330/share. It has bought back 1.759 million shares at a total cost of Rs 580 m.