In the Indian stock market, there are “story stocks” and there are “spreadsheet stocks.” Story stocks rely on narratives of future domination. Spreadsheet stocks rely on hard, cold cash flow. Rarely do you find one that is both.

So, when you find a stock that passes this test, it makes sense to dive deep and see if the stock holds any promise.

Especially if you see that a stock passes this test and is also trading at a discount.

The stealth mode small-cap solar champion

If you are thinking about Waaree Energies, we don’t blame you. After all it is India’s largest manufacturer and exporter of solar modules.

We are talking about a stealth mode small cap underdog, that is hitting the sweet spot between stock story and spreadsheet stock.

Solex Energy Ltd is one of those rare anomalies.

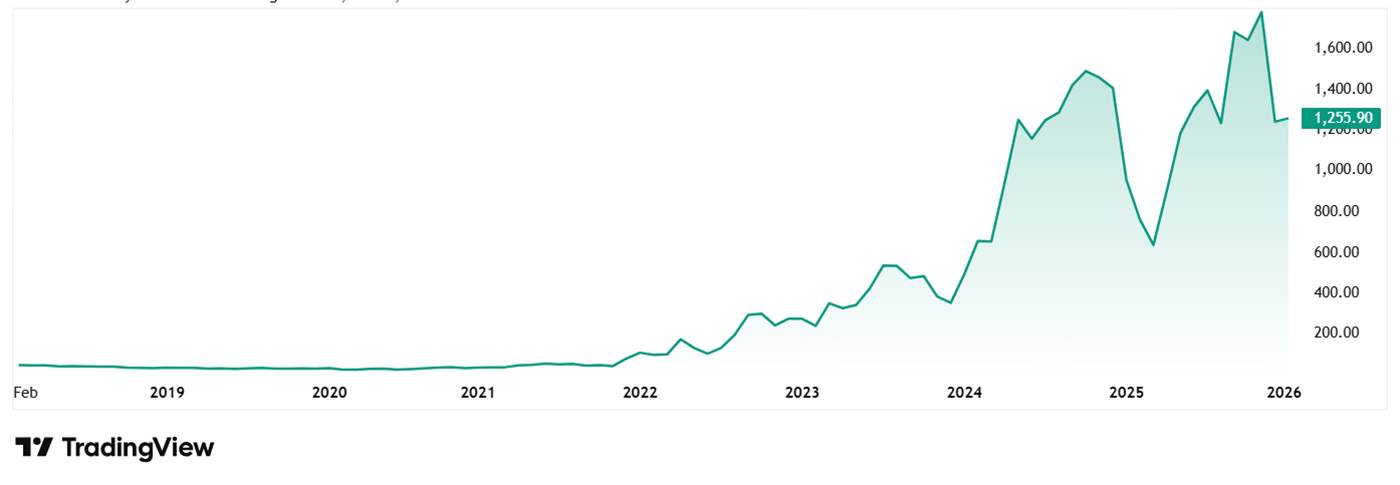

If you had invested Rs 1 lakh in Solex Energy five years ago, your portfolio would theoretically be worth close to Rs 42 lakhs today.

Mind you, this isn’t a hypothetical back-test; it is the reality of a stock that has surged from an unknown penny-stock to a commanding market price ofRs 1,251 (as on 5th January 2026).

Chart: Solex Energy Share Price

But what makes Solex fascinating isn’t where it has been, but where the data suggests it is going.

As India sprints toward its 2030 target of 500 GW of renewable energy, Solex has positioned itself not just as a participant, but as a highly efficient player in a capital-intensive space.

The macro view: Riding the $500 billion solar wave

To understand Solex, you must first understand the stage. The Indian government has declared war on carbon. With schemes like PM KUSUM (subsidizing solar pumps for farmers) and the PLI (Production Linked Incentive) for solar manufacturing, the ecosystem is glowing with liquidity and demand.

Solex didn’t just get lucky; they aligned their rowing with the current. The company manufactures solar photovoltaic (PV) modules, the actual “panels” you see on rooftops. But unlike generic assemblers, Solex has moved up the value chain, securing orders for solar water pumps and large-scale EPC (Engineering, Procurement, and Construction) contracts.

If we take a sector-wide look, the push by government and need to move to a greener future has pushed many companies ahead. But Solex has something that few of its peers can boast of. Its Capital Efficiency.

The litmus test: Why ‘spreadsheet’ investors love this stock

Return on Capital Employed (ROCE) is the ultimate litmus test for a manufacturing company. It tells you how much profit the company generates for every rupee of capital invested.

The median ROCE when compared to peers from the same sector is about 15%. But Solex has a 10-Year Average ROCE that stands at a tall 24%.

And that right there is a big authority signal.

It simply means that for a decade, through market cycles, policy changes, and raw material volatility, Solex has consistently squeezed more value out of its factories than its peers.

In the most recent year (FY25), the ROE (Return on Equity) hit a strong 39%, showing that shareholder capital is compounding at a fast rate.

The growth engine: 58% CAGR in profits

Efficiency is great, but you need growth to justify a Rs 1,356 cr market cap. To understand if that is the case, let us look at the financials for Solex.

We shall look at the standalone figures to get a longer period to look at, for a better perspective.

The sales of the company went from Rs 138 cr in FY20 to Rs 660 cr in FY25, which is a compound growth of 37% in 5 years. For H1FY26, the sales reached nearly Rs 400 cr, hinting at a strong end to FY26.

As for the EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) the company grew from Rs 7 cr in FY20 to Rs 69 cr in FY25, logging a compound growth of 58%. For H1FY26, the company has already logged operating profits of almost Rs 54 cr.

When it comes to Profitability, the company saw nothing short of a rise from the ashes as it jumped from Rs 4 cr in FY20 to Rs 40 cr in FY25, logging a compound growth of 55%. For H1FY26, the company has recorded profits of Rs 26 cr already.

While many would like to call this steady growth, a few might even call it exponential.

The company is capturing market share aggressively, likely fuelled by the commissioning of its new 1.2 GW (now scaling to 4 GW) manufacturing line in Surat.

Beyond assembly: The backward integration pivot

Currently trading at a P/E (Price to Earnings) ratio of roughly 26x, Solex is not cheap in the traditional sense. However, when you adjust for growth (PEG ratio), the view changes.

A company growing earnings at 300% YoY (as seen in FY25) often commands a premium. The market is betting that the FY25 earnings explosion wasn’t just a fluke.

The big question is what is Solex doing differently?

1. Backward Integration: Solex isn’t content just assembling modules. They are moving into cell manufacturing (TopCON technology). In the solar supply chain, cells are the high-tech component. By making their own cells, they protect their margins from Chinese import volatility.

2. The Technology Twist: Solex has transitioned from older Polycrystalline technology to TopCON modules. In simpler words, the company is making better and more efficient panels, which allow them to command a higher price per watt. This technological nimbleness is why their margins (OPM) have jumped from about 2-3% a few years ago to over 10% in FY25.

3. The Order Book: According to screener.in, the company’s order book at the end of FY25 stood at Rs 175 cr. In May 2025, Solex bagged an order from KPI Green Energy for over Rs 450 cr. The government-backed demand acts as a safety net, ensuring factory utilization remains high even if private demand falls.

The risk factor: Chine and cyclicality

No company comes without its risks. Let us look at the red flags.

1. The Volatility of Quarterly Earnings: While the annual numbers are stellar, the September 2025 Quarter showed a downward trend.

- Sales: Rs 155 Cr (Down from Rs 260 cr in June ’25).

- Net Profit: Rs 6 cr (Down significantly from Rs 25 cr in June ’25).

The company faces cyclicality. Solar project execution slows down during monsoons (Q2), which explains the dip, but a drop of this size is a reminder that this is a small-cap stock.

It creates lumpy cash flows that can scare away weak hands.

2. The “China Factor”: Solar industry essentials like wafers, silver paste, glass etc are still heavily dependent on global supply chains, a space dominated by China. A geopolitical issue or a just a spike in silver prices could make those hard-earned margins fall overnight.

3. Valuation Discomfort: After a 4,000% run-up, the stock is now trading at a modest PE of 26x. Any deviation from the growth trajectory, like the weak Q2, is punished severely. The stock has already corrected over 35% from its all-time high, reminding investors that gravity still applies.

A gem or a trap?

Solex Energy Ltd represents the India Growth Story. It is a small player punching above its weight, armed with high efficiency (24% ROCE) and operating in a sector with a 10-year tailwind.

The 4,000% return is in the rearview mirror. The question for new investors is whether the company can execute its expansion to 4 GW and beyond. Note that while promoter holding fell from 71% (Sept 2024) to 66% (Sept 2025), the promoters still retain significant skin in the game.

According to screener.in, the company has guided revenues of Rs 2,200–2,400 cr for FY26 (including EPC) and Rs 3,000–3,400 cr for FY27 with 4 GW module capacity and EPC, while aiming to maintain EBITDA margins of 9-11%.

If you believe in the Solar Surge and want exposure beyond the crowded large-caps, Solex demands a place on your watchlist. But unlike the verified stability of a Tata or Adani, this needs proper scrutiny before you jump in.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.