")

Fondly called the “Queen of Small Caps,” Dolly Khanna needs no introduction. One of the most highly followed super investors known for the knack to spot future multibaggers, her disciplined and thoroughly researched approach has earned her the well-deserved title.

She has been investing in the stock markets since 1996 and currently her portfolio holds 10 stocks worth almost Rs 265 cr. Her portfolio is managed by her husband Rajiv Khanna.

Recent exchange filings reveal a significant portfolio reallocation. Two stocks: one a fresh addition to her portfolio and the other she sold off after holding it for over 4 years.

IFB Agro Industries Ltd – The Alcohol Entry

Incorporated in 1982, IFB Agro Industries Ltd is in the business of manufacturing alcohol, bottling of branded alcoholic beverages, processed marine foods for domestic and export markets and sale of feed.

With a market cap of Rs 1,338 cr, the company owns 1 distillery plant and 2 bottling plants that together get its manufacturing capacity to 170 KLPD and a total bottling capacity of ~216 Mn bottles a year.

Dolly Khanna just bought a 1.13% stake in the company worth around Rs 15 cr as per the exchange filings made by the company for the quarter ending December 2025.

Analysing the company’s financials reveals the likely rationale for this acquisition.

The sales of the company were Rs 986 cr in FY20 and as of FY25, the sales were Rs 1,059 cr logging a compound growth of just 1%. For H1FY26, sales of close to Rs 700 cr have been recorded already by the company.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) logged a compound growth of 7%, but not without a lot of ups and downs in the 5 years.

| FY | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| EBITDA/Rs Cr | 26 | 55 | 75 | 73 | -10 | 37 |

And for H1FY26, EBITDA of Rs 59 cr is logged by the company hinting towards a stronger end to FY26.

The net profits also followed a path like the EBITDA.

| FY | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| Profit/Rs Cr | 22 | 46 | 59 | 49 | -8 | 22 |

For H1FY26, the company has logged net profits of Rs 40 cr already, which means FY26 will end on a much stronger note than FY25.

If we put all this together, while the sales have shown dismal growth, operating profits and net profits seem to be on a rebound heading towards a strong end to FY26. This could be a reason for Dolly Khanna’s interest in the company.

Financial Performance: A Rebound in Sight?

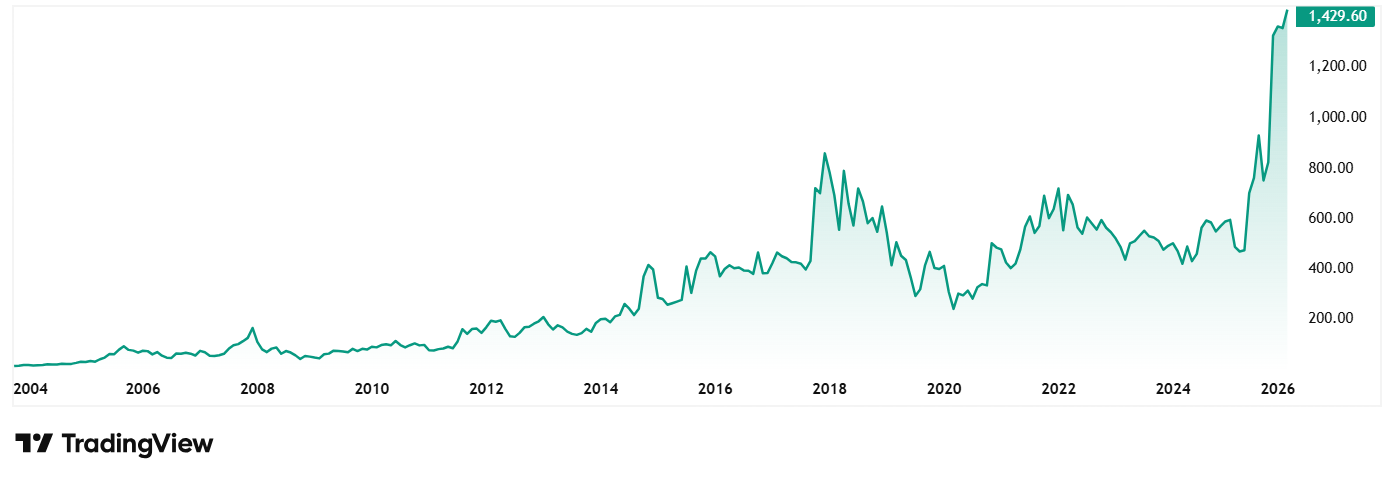

Add to that the share price of IFB Agro Industries Ltd which jumped from around Rs 460 in January 2021 to its current price of Rs 1,428 as of closing on 14th January 2026. That’s a jump of 210% in 5 years. Rs 1 lakh invested in the company 5 years ago would have been Rs 3.10 Lakhs today.

Even at this 210% jump, the stock is trading at a discount of over 20% from its all-time high of Rs 1,795, giving rise to questions if this is a good point of entry for the investors who lost out on the last rally.

Strategic Pivot: Beyond West Bengal’s Liquor Policy

The stock is trading at a PE of 26x, which is lower than the industry median of 33, making the stock an undervalued pick for Khanna. The 10-Year median for the company is 13x and the industry median for the same period is 22x.

The company is now focusing on the vision of its late Founder and Chairman, Bijon Bhushan Nag, to scale its marine (aqua feed) segment into a big valuable business and de-risk from West Bengal liquor policy challenges. The company on the same lines acquired Cargill India’s Shrimp and Fish Feed Business, and by FY28 plans for exponential growth by scaling Cargills assets.

Prakash Pipes Ltd – Small Cap That Lost Favor

Incorporated in 2017, Prakash Pipes Ltd was a part of Prakash Industries Ltd and was formed by means of a demerger of business.

With a market cap of Rs 513 cr, the company is in the business of manufacturing

PVC pipes and fittings. It also specializes in sustainable laminates, composites and

barrier films, to create quality packaging solutions.

The company boasts of a ROCE (Return on Capital Employed) of 27%, while the industry median is 16%. Which means it makes over Rs 27 on every Rs 100 it uses as capital while its peers average just around Rs 16. However, even this capital efficiency couldn’t hold Dolly Khanna from selling her stake in the company.

Khanna held a stake in the company since December 2021 (as per data on Trendlyne.com). And as per the exchange filings for the quarter ending December 2025, her stake has fallen below 1%, meaning a partial or complete exit from the stock.

Surprisingly, her fellow super investor, Mukul Agrawal continues to hold 2.36% in the company, which gives rise to a lot of questions in the minds of investors.

Let us look at the financials to make sense of this difference of opinion.

Prakash Pipes: The Erosion of Operating Margins

The sales of the company have grown at a compound rate of 15% between Rs 385 cr in FY20 and Rs 780 cr in FY25. And for H1FY26, the company has logged sales of Rs 385 cr.

EBITDA grew from Rs 38 cr in FY20 to Rs 121 cr in FY25, logging a compound growth of 26%. However, EBITDA recorded for H1FY26 was about Rs 32 cr, which is a drop of 50% from the previous figure of Rs 64 cr for H1FY25.

The net profits grew from Rs 25 cr in FY20 to Rs 83 cr in FY25 logging a compound growth of 27%. For H1FY26, the profits recorded are Rs 20 cr, which is lower than the figure of Rs 30 cr for the same two months previous year.

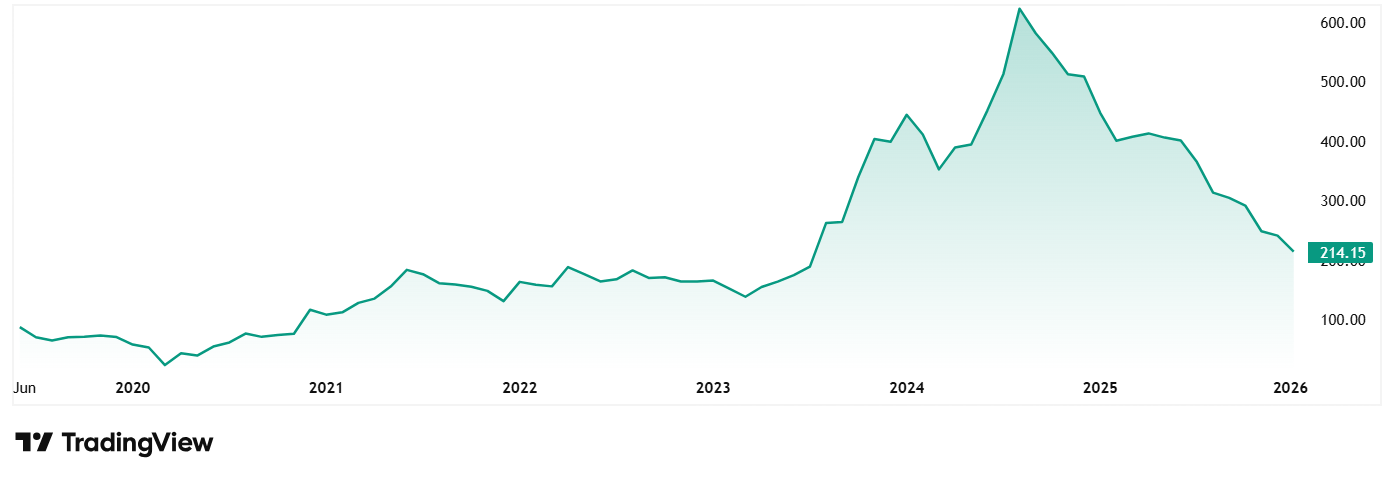

The share price of Prakash Pipes was around Rs 117 in January 2021 and as of closing on 14th January 2026 it was Rs 214, which is an 83% jump in 5 years.

At the current price of Rs 214, the share is trading at a discount of about 68% from its all-time high of Rs 668.

The company’s share is currently trading at a PE multiple of 10x, while the industry median is 22x. The median PE for the last 10 years is 9x and the industry median for the decade is 23x.

Future Outlook: Capacity Expansion and New Verticals

The company is entering the next phase of expansion by adding CPVC and UPVC injection molding machines to increase its production capabilities. Additionally, it is introducing a new product line for HDPE drums, which is crucial for the pharmaceutical, chemical, and food processing industries.

Also, the company is expanding its capacities to 36,000 MT over the next 2 years, focusing on extrusion-coated and laminated structures. Investments are being made in machinery.

Verdict: Strategic Moves or Dodged a Bullet?

If there is one super investor who has proved many times that the risk associated with small caps, it is Dolly Khanna. She has shown that if one has the right strategy and strategic research, even this category could be a goldmine.

Hence, when she picks or drops stocks from her portfolio, the market takes notes. The fresh pick, IFB Agro has logged some impressive numbers and looks like is on the way to a comeback. But the sell off, Prakash Pipes, despite strong conviction by management has lost Khanna’s favour.

Was the Prakash Pipes sell off one where Khanna dodged a bullet? Is the IFB Agro pick the next multibagger in making? These are questions that only time can answer. But if you want to find out, we recommend you add these stocks to your watchlist and follow them closely.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.