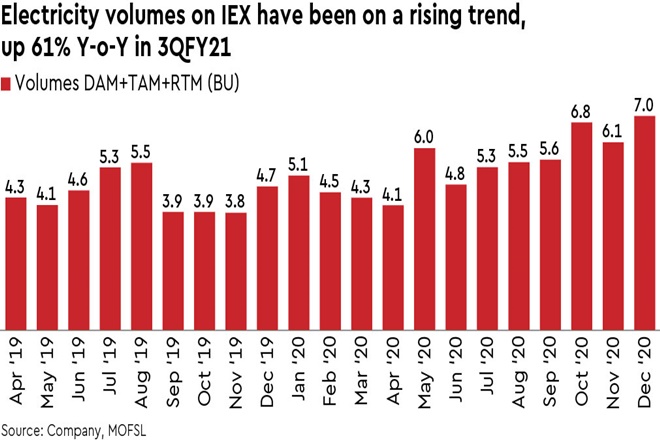

Electricity volumes on Indian Energy Exchange (IEX) jumped 49% y-o-y to 7BUs in Dec’20, led by: (i) continued growth (up 29% y-o-y) in day-ahead market (DAM) volumes, and (ii) strong volumes for the recently launched RTM. In Q3FY21, electricity volumes grew 61% y-o-y to ~20BU. Based on initial data from POSOCO and power ministry, power demand for the quarter is estimated to have risen 6.5% y-o-y, with a generation of 337BUs. This implies a 5.9% market share for IEX for the quarter (v/s a 4% share in FY20).

While an uptick in merchant prices (as demand improves) and the large base of Q4FY20 needs to be watched, we conservatively revise our FY21e electricity volume/EPS estimates by 10%/8% given its strong performance. Rolling forward to 30x Dec’22e EPS, we maintain our Buy rating with a TP of Rs 255/share.

New products faring well: The launch of new products such as the Real-Time Market (RTM) and Green Term Ahead Market (G-TAM) has also provided a fillip. RTM crossed over 1BU in Dec’20 and contributed ~14% of IEX’s electricity volumes in Q3FY21. Total, TAM (incl. G-TAM) + RTM now contribute 20% of its volumes.

Await resumption of REC trading, launch of LDCs: Trading for RECs continues to be suspended since Jul’20. While we expect trading in RECs/LDCs to eventually resume/launch, we do not build in incremental volumes from the same for the remainder of FY21.

Market share gains to drive volume/PAT CAGR of 16/18% over FY21-23e: Long term potential for IEX remains huge given the nascent market share for exchanges in India’s power generation. With new product launches, continuous oversupply in the market, and IEX’s competitive positioning, we expect volumes/PAT to increase at 16%/18% CAGR over FY21-23e. Given the strong growth and high return profile (RoEs of ~45%), the stock trades attractively at 25x FY23e EPS. Maintain Buy .