Novo Nordisk is having a moment. The Danish pharmaceutical giant has seen its stock price skyrocket roughly 25% over the past month, and Wall Street can’t decide whether this is the beginning of a comeback story or a temporary bounce in what’s been a turbulent year.

The headline grabber? Novo just became the first company ever to get an oral GLP-1 pill approved for weight loss. That’s a massive milestone in a market analysts predict could reach $100 billion annually.

The once-daily pill offers the same semaglutide that made Wegovy injections wildly successful, but in a format that’s infinitely more appealing to needle-phobic patients. At $149 per month initially (rising to $199 after April 15), it’s positioned as more accessible than injections and could dramatically expand the patient pool.

But here’s the twist: while investors celebrate, CEO Mike Doustdar just threw cold water on the party at this week’s J.P. Morgan Healthcare Conference. His message? Buckle up, because 2026 is going to be rough.

The international headwinds nobody saw coming

Novo’s international operations, spanning 80 to 85 markets globally, are about to face serious pressure. The company is losing market exclusivity in several countries, meaning competitors can now legally sell their versions in markets where Novo once dominated. “When you have a very high market share, competition will take some of that share away,” Doustdar admitted, warning of “a difficult year” ahead.

The timing couldn’t be worse.

After struggling through 2025 with supply constraints and pricing pressures, Novo was counting on international markets to pick up the slack. Instead, Eli Lilly is expanding aggressively across multiple geographies with Mounjaro and Zepbound, which generated a staggering $24.8 billion in combined sales during the first nine months of 2025—54% of Lilly’s total revenue.

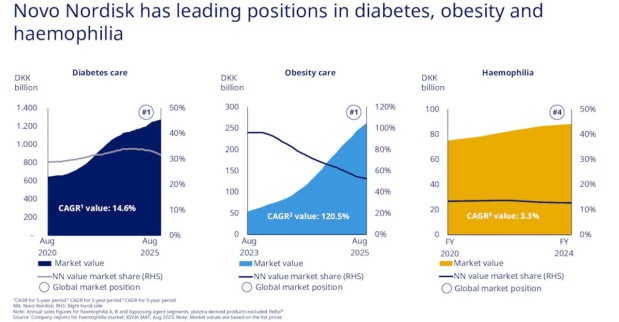

Market share data tells a sobering story. Novo has experienced continuously deteriorating share in both Diabetes Care and Obesity throughout 2025, a trend that didn’t stop in Q3.

Meanwhile, Lilly keeps gaining ground with what many view as superior tirzepatide-based products.

The pricing pressure dilemma

Here’s another massive issue: Novo slashed U.S. prices on Wegovy and Ozempic during 2025, dropping monthly costs from around $959 to approximately $274—a 71% price cut. The strategy helped recapture volume from compounded alternatives and expand access, but it raises serious questions about margin compression.

The impact is already visible. Novo revised its 2025 outlook downward twice, from initial projections of 13-21% sales growth to just 8-11%. For 2026, consensus estimates project essentially flat to slightly negative growth—a tough comparison against 2025’s higher pricing.

Why investors are still betting big

Despite these headwinds, there are compelling reasons for optimism. Novo’s pipeline is firing on all cylinders.

CagriSema, a next-generation injectable combining GLP-1 with an amylin analogue, has been submitted for FDA review with approval expected in 2026. Amycretin, another next-generation candidate, enters phase III trials in early 2026 with potentially even better efficacy.

Beyond obesity, Novo is diversifying. Wegovy became the first GLP-1 approved for treating liver disease (MASH), opening an entirely new market. The company secured approvals for Alhemo in hemophilia A and B, and submitted filings for Mim8, expanding its rare disease footprint.

The oral Wegovy advantage is real.

Yes, it requires morning fasting for 30 minutes before eating—a restriction Lilly’s pending orforglipron doesn’t have. But Doustdar pointed out that Rybelsus, Novo’s oral diabetes drug with similar requirements, has attracted 1.5 million patients. He also noted Lilly’s pill may require patients on certain statins to wait two to four hours before dosing.

Being first to market matters. Physicians develop prescribing habits, patients develop brand loyalty, and payers negotiate formulary positions. Even when Lilly’s pill eventually gets approved, Novo will have a meaningful head start.

Yes, it requires morning fasting for 30 minutes before eating—a restriction Lilly’s pending orforglipron doesn’t have. But Doustdar pointed out that Rybelsus, Novo’s oral diabetes drug with similar requirements, has attracted 1.5 million patients. He also noted Lilly’s pill may require patients on certain statins to wait two to four hours before dosing.

Being first to market matters. Physicians develop prescribing habits, patients develop brand loyalty, and payers negotiate formulary positions. Even when Lilly’s pill eventually gets approved, Novo will have a meaningful head start.

The valuation story

Despite the 25% surge, Novo trades at 17.02 times forward earnings, well below its five-year mean of 29.25. Multiple analysts peg fair value at $63-$69, suggesting another 7-17% upside. That’s either a screaming buy or a value trap, depending on whether you believe Novo can execute.

The bottom line

For long-term investors, Novo remains a leader in one of the biggest pharmaceutical opportunities ever created, with a first-mover advantage on oral therapies, a stacked pipeline, and global scale. The obesity market is still in its infancy—only a fraction of eligible patients are on treatment.

But short-term volatility is almost guaranteed. The next 12-24 months will be bumpy as Novo navigates pricing pressure, Lilly’s competition, and international headwinds. Post-2026 looks better once the company gets past difficult comparisons, but getting there requires patience.

In short, don’t expect smooth sailing—this is a bet that innovation can overcome execution challenges before it’s too late.

Sonia Boolchandani is a seasoned financial writer She has written for prominent firms like Vested Finance, and Finology, where she has crafted content that simplifies complex financial concepts for diverse audiences.

Disclosure: The writer and her his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.