We attended Infosys’s analyst meet, where the company showcased its progress on the ‘Renew’ and ‘New’ strategy, threw light on addressing of first quarter performance, business environment and retention of senior leadership. While the termination of RBS contract drives further pressure on current guidance, Infosys chose to defer any update on the same up till October, to get a greater grip on the nature of headwinds. It admitted that challenges to business do pose downside risk to guidance.

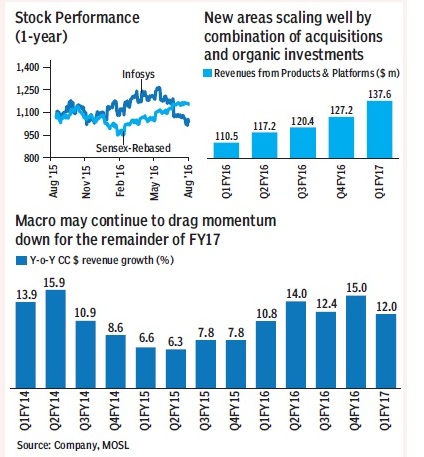

Infosys’s longer term ‘Renew & New’ strategy continues to progress well. Strides around renew of core are reflected in increased utilisation, improved large deal wins, and uptick in automation. At the same time, new initiatives are fast gaining scale and traction, with: (i) 104,000 employees introduced to Design Thinking workshop, (ii) Zero Distance spanning 95% of 9.5k projects, and floatation of 11.4k ideas (iii) 4 live engagements already in 4-month old MANA, and (iv) 40% q-o-q growth in new areas last quarter. Infosys also demonstrated the capability of its AI platform MANA, showcasing the use of the product across various stakeholders in the client system. MANA already has a significant pipeline of potential customers on the platform.

Defers guidance update amid a turbulent macro

The recent termination of Infosys’s contract with RBS was a further dent in its revised 10.5-12% y-o-y constant currency growth guidance amid a tough macro. While we believe that a moderation in guidance is imminent, Infosys chose to defer an update on its guidance in October. It remains confident that growth in second quarter will be better than Q1 (1.7% q-o-q in constant currency and 2.2% q-o-q in USD). That said, it admitted that the headwinds to business are clearly higher than that baked into the guidance at the beginning of the quarter, and there is a downside risk to FY17 guidance. The weakness is not yet broad based, but restricted to select clients. Notwithstanding the near term macro, pipeline of deals remains very healthy. The much improved trajectory of deal wins over last few quarters is expected to continue. However, some of these large deals take time to ramp up, especially in the current environment.

Long term agendas around Renew & New going well

Infosys’s longer term execution on the strategy of Renew and New continues its march, and the launch of MANA is an example to that effect. MANA is at the heart of Infosys’s renew strategy, and has already gone live in some accounts, despite being only 4 months old. Operational excellence (utilisation, sub-contractor costs, large deal wins), landscape renewal (mainframe modernisation, migration to cloud) are the other pillars of its renew strategy. As far as INFO’s initiatives around renew are concerned, it has trained over 100K+ associates in Design Thinking and conducted 200+ Design Thinking workshops. Through the Zero Bench initiative, it has created over 21,600 work pockets. Coverage of Zero Distance now spans 95% of the projects with over 11,400 ideas floated. New areas have kicked off nicely through Skava, and continue to bode excitingly with Design Thinking at the heart, along with M&A and other investments. Design Thinking has been a key initiative since the articulation of INFO’s new strategy. In the new areas, 104,000+ employees who have attended the Design Thinking workshop have got a start in looking at tasks more strategically. Investments in acquisitions like Skava has already been witnessed in current and new accounts. Revenue from new services grew by 40% q-o-q in the previous quarter demonstrating the pace of progress of its initiatives.

More strategic engagement with its clients

The larger, long term intent of INFO is to elevate quality of discussions with customers enabling a consultative-led approach towards transforming customers’ businesses. This needs the front end to have the content, confidence and articulation. While INFO is slowly improving towards that end, this is restricted only in a few instances and is far from mainstream, as the number of people who can engage in such strategic discussions is insufficient. INFO’s attempt to get the capabilities up to the level needed is through a combination of all three: (i) tap the available skilled talent, (ii) skill more people internally, and (iii) amplify the ability of people with software.

Early signs in improving sales effectiveness

INFO’s focus on large deals has been fruitful over the last year, with a 45% growth in TCV seen in FY16. Higher win rates, relationships with advisors, separate hunting and farming function and reach to new clients in new geographies have all contributed to the progress. Moreover, MANA, Skava and Edgeverve have been further aiding INFO’s positioning in the market. At the same time, growth in top accounts has been higher than company average, and the number of engagements that are above $ 100 million have increased.

Shortcomings of Q1 arrested

The problem areas that caused a subdued beginning to the year were weakness in consulting, led by project completion that didn’t get renewed, decline in EMEA and India, decline in Finacle. These drag factors have been arrested, and leadership changes have taken place where necessary (Finacle and Consulting). All these areas are being monitored closely, and the company expects better growth in Q2, compared to Q1.

INFO’s focus on high-performers and efforts to increase retention are reflected in the resumption of the ESOP programme, and higher-than-average compensation increase for high-performers. High performance employees on average were given a salary increase of 2.2x v/s the overall average. The measures to stem the attrition of quality talent has paid dividends, with title holder attrition down to 4.9% from 7.4% in Q4FY15 and 9.6% in Q2FY16. Its high performer attrition is down 220bp q-o-q to 11.2%. The company expects that its measures would drive continued improvement in attrition.

MANA — more than just Automation

INFO demonstrated to us its recently launched knowledge-based Artificial Intelligence Platform MANA. It enables continuous reinvention of existing systems, which is otherwise a complex and expensive process. It not only helps manage infrastructure but also in maintaining systems by deep understanding of the systems. INFO showcased this by an instance of how once MANA has captured the knowledge of the underlying system, there is a clear business case for multiple stakeholders from business manager to an engineer.

Valuation view: Gunning to regain bellwether status

Journey to ‘Infosys of the future’ progressing well: INFO’s strategy ‘renew and new’—renewing the way of delivering existing services and also building new services of the future — resonated with the changing landscape of technology demand. Several senior personnel from SAP have been recruited to facilitate this. Successful execution of the strategy will help INFO regain its bellwether status with industry-leading growth at strong profitability.

Addressed various pain points under new management: Over the past 4-5 quarters (before Q1FY17), INFO’s improving traction is demonstrated in multiple areas: Volume growth has picked up gradually from 9.3% in FY15 to 14.5% y-o-y in FY16. Improvement in client mining—top-10 accounts, which were flattish till Q1FY15 have turned around impressively. Top account has grown 17.1% in FY16 (compared to -5.6% in FY15). Similarly, the top 2-5 accounts have grown by 9.3% in FY16, compared to 0.7% in FY15. Deal wins have picked up, with TCV of $2.8 bn in FY16 being 45% higher than that in FY15. INFO hasn’t factored in an additional $440m from deals that have been framed but not concluded. Flux in the senior management has been addressed. Standalone attrition declined from 18.9% in FY15 to 13.6% in FY16. Cost optimisation levers have helped deliver on margins despite pricing pressure —

IT Services utilisation excluding trainees is up to 81% in FY16 and FY15, from 77% in FY14 and 73% in FY13.

After cost optimisation, pricing aggression puts margins in limelight: INFO’s cost structures have stabilised, allowing it to balance investments and profitability without having significant volatility on the margins. While there remains room to improve utilisation, optimising onsite employee and subcontractor costs in the near to medium term, these may in the best case offset the headwind from wage hikes and lower pricing. Velocity of benefits from new initiatives like automation will be crucial, in the absence of which, execution on the margins will get challenging. However, we see this as a sector-wide phenomenon and believe outperformance on revenue growth will aid relatively better show on profitability too.

Cut estimates following Q1 miss, but expect growth to revive in Q2: We have cut our $ revenue estimates for FY17/18 by 2.4%/3.2% and earnings estimates by 5.5%/4.3% respectively. INFO had steadily addressed the concerns under new management over last 18 months around revenue growth, operating margins and new age services. A soft start in the challenging macro pushes the recovery back a few paces, and growth rebound in Q2 will be crucial for industry-average growth in FY17. Momentum in top-25 accounts and deal wins lend confidence towards that end.

Uncertainty limits triggers in the near term: The stock trades at 17.0x/14.6x on our FY17e/18e earnings. We expect INFO to grow its revenue at a CAGR of 10.6% over FY16-18 and EPS at a CAGR of 10.7% during this period. We believe that INFO is investing in all the right areas to regain and sustain its growth leadership, compounded by industry leading margins. Our price target of R1,300 discounts two year forward earnings by 18x. Notwithstanding the headwinds over the near term, INFO’s gradual recovery to industry-matching/industry-leading growth at a strong margin will command a premium to peers. Maintain buy.