IDFC Bank is now focused on customer acquisition, helped by its digital platforms, ad campaigns and competitive rates. It is focusing on salaried clients, large corps and SMEs for Casa and we forecast its Casa ratio to reach 15% of deposits by FY21. We expect diversification into retail/working-capital loans and PSL buyout to drive loan growth. IDFC Ltd offers better risk-reward if the holdco structure unwinds. While valuations look fair after the recent rally, we see franchise buildup driving a rerating and raise our targets from R65 to R92 for IDFC Bank and from R60 to R80 for IDFC Ltd as we roll forward our numbers. Buy.

Digital platforms, marketing and market rates to aid Casa

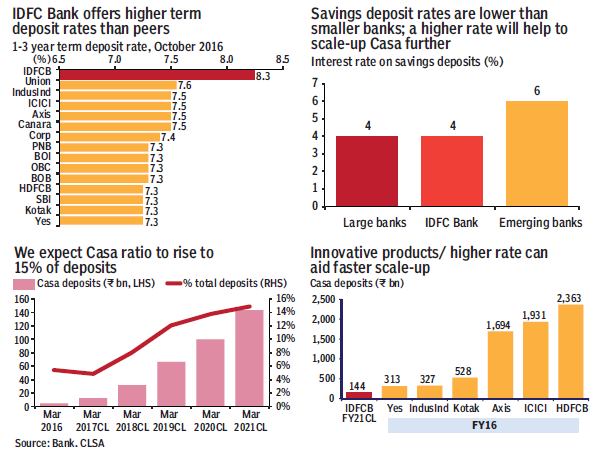

After beefing up teams and completing its product suite, IDFC Bank is leveraging relationships with corporates to build salary deposits. Its key offerings are: account opening in 4 minutes, leveraging tablets and Aadhaar data; and higher term-deposit rates (8.3% vs 7.5% at peers) with free sweeps. Its savings deposit rate of 4% is lower than emerging private banks; higher rates/innovative-offerings can help build Casa faster. For current deposits, it’s leveraging corporate and SME relationships with its ‘Truly One Account’ offering. Scale-up of Casa is key to asset growth.

You may also like to watch

Loan growth led by diversification & PSL buildup

We forecast a 23% loan CAGR for IDFC Bank over FY16-21, led by diversification into working capital lending and retail, including priority sector loans (PSL). Its competitive lending rates and better capitalisation will help it gain share among better-rated clients/refinancing opportunities and also help build non-fund based relationships for fees. Scaling up the Bharat Banking model (non-urban segment with expectation of 4-5 million customers in 5 years) and the recent acquisition of a micro-lender will be key.

Holdco offers better risk-reward than bank

After the recent rally, IDFC Bank’s valuations seem fair, but the holdco discount at IDFC Ltd has widened to +45% and can unwind if the structure can be simplified. We raise our earnings and target for IDFC Bank to R92 as we roll forward to 2.2x Sep 18CL adjusted PB; and raise our IDFC Ltd target to R80 post a 40% holdco discount. We maintain buys on both stocks.