Dhariwal is L1 to supply 185 MW (net) to Maharashtra (MH) at Rs 2.76/kWh during December 2017 to June 2018. The contract is part of the flexible coal scheme under which coal will be supplied by MH at Coal India’s notified price. We estimate contribution margin of Rs 0.7-0.8/kWh. Dhariwal will supply the power from its second unit of 300 MW (2×300 MW plant). Though the margin is low, the strategy partially de-risks it from the volatile merchant market. Moreover, Dhariwal can now look to supply in day-ahead market from the remaining 115 MW capacity, given that operation of part of the unit is now assured. MH could extend the contract, as the price is lower than variable cost of its own plants. We have increased PLF estimate from 50% earlier to 70% over FY19-20 for Dhariwal.

UP regulator rejects additional regulated PPA for Noida; no surprises: In another development, the Uttar Pradesh (UP) regulator has rejected the proposal for an additional regulated PPA between Dhariwal and Noida DISCOM. It has argued that a competitive bid can fetch lower tariff than the regulated tariff offered by Dhariwal. The decision does not come as a surprise. We were building in just 50% PLF over FY18-20 at Dhariwal (existing long-term PPAs of 287MW and some merchant sales). There is no impact on our estimates.

Spencer’s — turnaround progressing well; focus shifting to growth: For Spencer’s, sales performance in the last couple of quarters was impacted by GST transition and some licensing issues in Andhra Pradesh (AP) and Telangana. Yet, it managed to report positive EBITDA (v/s -ve 1.3% margin in FY17), driven by savings in overheads. Sales have begun to recover from October and cost savings should continue. The management expects Spencer’s to turn PAT-positive from FY19. The focus in the last few years was to close unviable stores and reduce overheads. With performance improving, the focus will shift back to growth.

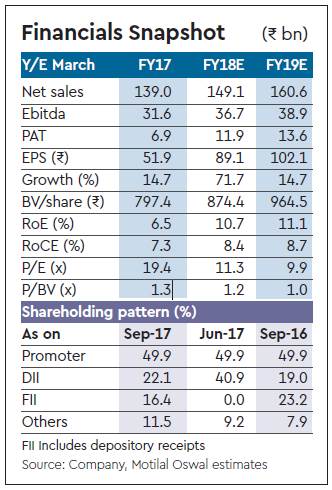

Demerger to unlock value: maintain Buy: We raise our PAT estimates marginally by 3% to Rs 13.6 billion/Rs 14.8 billion for FY19/20 on higher PLF at Dhariwal. CESC’s demerger plans remain on track. It has received exchange and SEBI approval. Shareholder meeting is scheduled on December 15, 2017. The demerger into four separate businesses would drive value through unlocking the potential of the distribution and retail businesses. Distribution business will get re-rated on reduced volatility in earnings and lower cost of equity. Spencer’s too will command better valuations after expected turnaround in FY18. Our SOTP value is Rs 1,360/share. Maintain Buy.