By- Smitha Francis and Murali Kallummal

From biscuits to automobiles, the Indian industry is battling the combined adverse impact of the economic slowdown and FTA-led import surge and is putting pressure on the government not to sign the mega-FTA, the Regional Comprehensive Economic Partnership (RCEP). RCEP is aiming at greater integration among the ten member ASEAN and six of its bilateral FTA partners in the Asia-Pacific region. Amidst the global slowdown and escalating trade tensions, the prospect of increased duty-free access to India’s large market is definitely of prime importance to the other negotiating countries. But is this the case for India?

Unquestioned faith in the ability of efficiency-enhancing international competition to deliver export growth has been one of the main drivers of India’s trade policy. This has led successive Indian governments to undertake import liberalisation in excess of India’s commitments under the WTO. In the absence of any strategic approach to trade liberalisation and industrial development, India carried out even greater tariff liberalisation in its FTAs with ASEAN (2010), South Korea (2010), and Japan (2011).

Also read: Modi govt’s mega PSU bank mergers to improve efficiency, credit quality; what analysts say

However, several trade-related indicators reveal that exposure to heightened external competition has not pushed domestic firms in the majority of manufacturing sectors to become significantly more competitive, either globally or in the markets of her FTA partners. An analysis of India’s top ten manufactured export sectors reveals that only four sectors, namely, organic chemicals, pharmaceuticals, vehicles and parts and non-electrical machinery have seen some increase in global export shares. All others among India’s top ten export sectors have seen drop in global export shares in the recent years, reflecting the inability of Indian firms to compete with competitors in her major markets.

Watch: How to file ITR-1 in less than 15 minutes

Even in the former four sectors, India’s global export shares remain very low, at 4%, 2.6%, 1% and 0.8%, respectively. Country-wise growth rates estimated for India’s manufactured exports also clearly establish that it is the share of exports going to low income markets that has recorded increase. There is a distinct decline in the growth in India’s exports to the developed countries. This is also a reflection of the challenges Indian firms face in maintaining their competitiveness in the technologically more mature advanced markets. It is equally revealing that while only 20 out of the 64 HS (Harmonised System) chapters representing manufacturing sector had recorded trade deficits during 1996-2001, as many as 52 sectors registered trade deficits during 2015-18.

A recent research policy paper from the Centre for Regional Trade, IIFT, made an argument that “Though India’s trade deficit as a percentage of total trade has increased, India’s total trade has also increased, implying that the capacity to sustain trade deficit has also increased”. Evidently, India’s trade deficit has increased as a percentage of her total trade precisely due to the faster growth in her imports in comparison with exports. In a narrow macro sense, the capacity to sustain trade deficit increases when the exact opposite happens; that is, when exports grow faster than imports.

But then the ratio of India’s trade deficit to total trade would not increase! (True that growing trade deficits can also be financed by becoming dependent on increasing inflows of foreign capital. But this increases the external vulnerability of the economy in a number of ways, causing a currency crisis or an ever widening current account deficit, and leading to a drain on economic growth and national sovereignty).

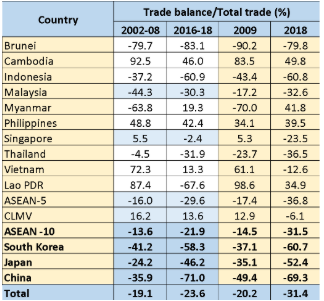

It is puzzling that in the case of ASEAN, the above paper claimed that India’s trade deficit to total trade ratio vis-à-vis ASEAN has declined from -17.4% in 2009 to -15.9% in 2018 and that this implies that “its capacity to afford trade deficit has increased”. As seen in the Table, the ratio of India’s trade balance to total trade has deteriorated for almost every single ASEAN member country (except Myanmar and the Philippines), as well as for ASEAN as a group. This is also true for India’s trade with South Korea and Japan.

Table 1. India’s trade balance with major FTA/CECA/CEPA partners and China

Source: Authors’ calculations based on WITS UN Comtrade data

Using DGCIS data, India’s trade balance to total trade ratio deteriorated from -17.5% to -22.6% with respect to ASEAN, -43% to -56.2% for South Korea, and -30% to -44.9% for Japan. India’s approach to FTAs has also been guided by the belief that increased imports of lower priced intermediate products from partners will increase the competitiveness of India’s final goods exports. (This is used to argue that FTAs will therefore increase Indian firms’ engagement with regional and global value chains.) Evidence based on a preliminary analysis of export unit prices of FTA partners vis-a-vis India carried out by the authors do not support these arguments. Changes in the average unit values of Japan, South Korea and ASEAN’s exports to India between their respective pre- and post-FTA periods were compared with the corresponding changes in the unit values of their global exports.

It is seen that capital goods and consumer goods (as categorised by the WTO) presented a mixed performance, with both lower and higher percentage increases in unit prices of their exports to India relative to the changes in their global unit export prices. However, in the majority of raw materials and intermediate goods, the increase in the unit values of their exports to India were significantly larger than the increase witnessed in the case of their global exports. Incidence of higher percentage increase in unit prices of their exports to India would mean that India was importing at a higher cost compared to the pre-FTA period.

Such increases were far in excess of the tariff preferences accorded by India under these agreements, making India’s raw materials and intermediate goods imports from these countries uncompetitive. It is high time to accept that if India’s export competitiveness had increased through liberalised access to imported inputs without industrial policy support for enhancing technological capabilities at the firm and industry levels, this would have reflected in increased export market shares for India. However, the evidence presented earlier is to the contrary.

In the case of ongoing RCEP negotiations, the benchmark for tariff reductions is the average applied tariff rate in 2013. Among RCEP members, India had the highest average applied tariff rate at 13.5% in 2013. Applied tariffs in many other countries are much lower. This means that Indian firms will not gain any significant price advantage from tariff liberalisation under RCEP. This is likely to be true even if the developed country partners like Australia, New Zealand, Japan, etc. agree to eliminate their tariffs immediately upon entry into force of the agreement and India is allowed a 20 year staging period to bring down its remaining tariffs.

It must be remembered that under the CEPA with Japan, Japan had eliminated tariffs on nearly 80% of its total tariff lines upon entry into force of the agreement in 2011. Yet, the share of India’s total exports going to Japan declined from between 2011 and 2018 (1.9% to 1.5%). It is thus unrealistic to hope that RCEP will offer any additional market access to Indian firms, especially with China’s inclusion in it. Between 15-17% of India’s total imports already originate from China compared with 2.8% in 2000, the year before China joined the WTO. Clearly, India thus has lower incentives in going ahead with RCEP negotiations without examining systematically how tariff liberalisation under the existing FTAs have eroded incentives for domestic production and increased import intensity in different sectors.

Moreover, in the absence of any significant benefit out of a decrease in tariffs across RCEP partners, the incidence of non-advalorem tariffs and non-tariff measures used by the various countries play critical roles in deciding actual market access. In case of agriculture, lack of information on the use of mandatory national MRL-based SPS standards by partners plague Indian small exporters’ access to markets. Seemingly, no effective attempt has been made during the ongoing negotiations to examine and factor in any of these measures. The fact that there have been no quantifiable gains for India under existing FTAs in the services sector (which has been considered the golden goose without economic justification, and against which the manufacturing sector tariff liberalisation has been continuously traded off), makes the case stronger.

(Smitha Francis is Consultant at the Institute for Studies in Industrial Development (ISID) and author of the recent book Industrial Policy Challenges for India and Murali Kallummal is Professor, Centre for WTO Studies, New Delhi. The views expressed are authors’ own)