Repo linked lending rate (RLLR): From October 1, 2019, all new floating rate personal or retail loans such as your car or home loans that are sanctioned by banks will have to be linked to external benchmarks, and the central bank’s repo rate is one of them. Every bank will have its own Repo linked lending rate or RLLR which will keep varying each time the Reserve Bank of India or the RBI revises the repo rate. For the uninitiated, repo rate is the rate at which banks borrow from the RBI. The central bank reviews the repo rate on a bi-monthly basis through its Monetary Policy Committee or MPC.

What is repo linked lending rate?

So, what is RLLR? As the name suggests, repo linked lending rate or RLLR is the lending rate which is linked to the RBI’s repo rate. However, the effective RLLR interest rate depends on multiple factors. For example, the RLLR-linked home loan interest rate will depend on several factors such as what the loan amount is, the loan-to-value of the loan and even the risk group of the borrower, amongst other things. There can be a Spread or Margin charged by the bank. To explain, a bank may have an RLLR of 6.5 per cent, but the actual home loan interest could be 7.5 per cent, of which 1 per cent will be the Spread or Margin of the bank. Banks are free to fix Margin while lending to the borrowers.

How does RLLR home loan work?

When banks borrow funds from the RBI, it is at the repo rate. Lowering of repo rate by the RBI makes banks lend at a lower rate. Therefore, in case of lending based on RLLR, the home loan interest rate will move up or down as per the movement in the repo rate. Let us see with the help of an example. Say, the RBI’s repo rate is 5.35 per cent and is cut by 35 basis points to settle at 5 per cent, the RLLR of all banks, having repo rate as the external benchmark, will also get reduced by 35 basis points. If the repo rate, in the above example is hiked, the scenario is reversed.

What is MCLR linked interest rate? Why is RLLR replacing MCLR?

Whenever the RBI revises the repo rate, the Marginal Cost of Funds based Lending Rate or MCLR of banks gets impacted. Any cut in the repo rate means that the banks can lower the MCLR and vice versa. However, it has been observed that there is a time lag in the passing of repo rate cuts from banks to the borrowers. In case MCLR linked interest rate, the entire repo rate cut benefit is not passed on. In RLLR loans, the transmission is quicker as compared to MCLR loans. Typically, in the case of MCLR-based loans the reset period is 12 months. When the interest rate is on a downward trend, the RLLR home loans would suit borrowers. Conversely, they may hurt borrowers in the rising interest rate scenario.

WATCH VIDEO | What is Repo Linked Lending Rate, Home Loan? RLLR meaning, comparison vs MCLR

RLLR vs MCLR home loan

- MCLR is primarily an internal benchmark of the bank as its own cost of funds will determine the MCLR of the bank. However, in the case of RLLR which is externally linked, the bank’s own cost of funds does not have a direct impact when the repo rate goes up or comes down. In the case of RLLR home loans, the interest rate will be linked to the bank’s RLLR. This RLLR, in turn, will depend on the RBI’s repo rate. Whenever the RBI revises the repo rate, RLLR of banks gets impacted. Any cut in the repo rate will help banks in lowering RLLR and vice versa. RLLR, therefore, is an external benchmark.

- The reset period in MCLR linked home loan is generally 12 months while a few banks have a 6-month too. Whatever the reset period is, the home loan interest rate and hence the EMI gets revised accordingly. This gives a time-lag to MCLR-based loans. However, in the case of RLLR based home loans, the reset-period for the interest rate and hence the EMI to reset is to be at least three months.

- In the case MCLR loans, the banks are allowed to charge a spread, mark-up or margin. For example, if the MCLR of the bank is 8.6 per cent, then it may lend at 9 per cent after factoring in 40 basis points of mark-up. In RLLR, the Spread is as per the loan amount and the risk group of the borrower.

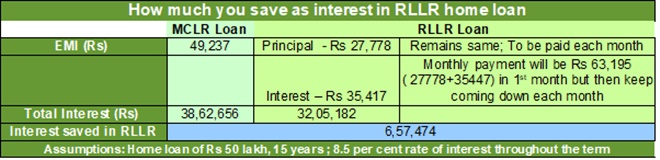

Let’s consider a simple example to understand the differences between MCLR and RLLR. For a fair comparison, the effective home loan interest is being taken at 8.5 per cent under both the scenarios – RLLR and MCLR home loan. This will remain the same through the term of the loans. In practice, being flexible loans, the rates will vary and typically MCLR loans will come at a higher rate of interest. Assuming one has to take a loan of Rs 50 lakh for 15 years, let us look at the difference in EMIs and interest burden.

MCLR home loan

The Rs 49,237 EMI remains constant for the entire 180 months period. The total interest paid over these months amounts to about Rs 38,62,656.

RLLR home loan

In an RLLR loan, two payments will be made separately. One, for the principal repayment and other for the interest payment. For RLLR loan, the principal loan amount is divided by tenure to know the EMP or equated monthly principal. This comes to Rs 27,778 in the example under consideration, and it will remain the same through the loan term. In the case of RLLR home loan, the interest payments will vary each month. They will be the highest in the first month and then keep falling.

Interest saved under RLLR loan: The borrower has to Rs 35,417 in the first month and by the 180th month, the interest portion comes down to around Rs 200. As per the RLLR amortization schedule, the total monthly payment for RLLR home loan is actually more than the MCLR home loan for the initial few years. This then tapers off in the subsequent years. For a 15 year loan, after a period of 6 years, the monthly payments witness a drastic fall as compared to the EMI in MCLR loan. For other scenarios, the calculations could work out differently.

But most importantly, the comparison tells us that the total interest burden is lesser in RLLR loans than MCLR loans. The above example helps understand how EMIs and interest burden differ, and by what extent is the interest cost expected to be lower in the case of RLLR loans. In this example, almost Rs 6.5 lakh lesser interest is paid in RLLR loan, primarily because the repayments are higher in initial years.