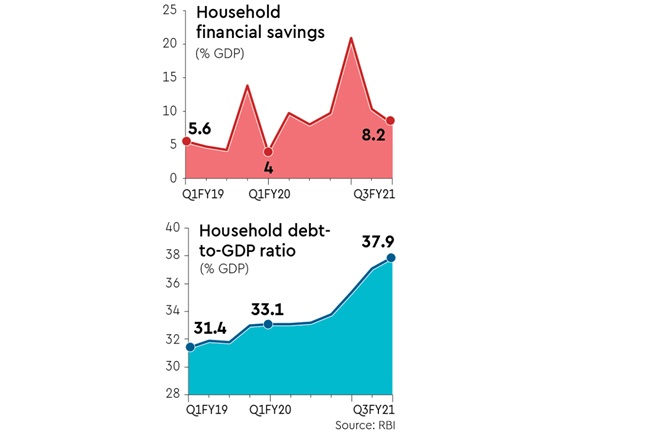

While there is no cause for alarm, the somewhat sharp rise in the household-debt-to-GDP ratio in the September and December quarters of 2020 needs to be watched. Much of the borrowing has been attributed to the increase in purchases of homes, cars, durables, as people adjusted to a new lifestyle last year in the wake of the pandemic. Higher medical expenses and financial distress, caused by a loss of jobs or a fall in incomes, could also have prompted additional borrowing. The jump in the ratio—by four percentage points, from 33.8% in March 2020 to 37.1% in June and to 37.9% by December—could also have been driven up by very small businesses, taking personal loans to fund their operations, as the economy opened up. These levels, are by no means low, especially in the current rough environment, and we may see a rise in delinquencies, especially from small businesses. Households seem to have borrowed a fair bit from NBFCs in the September quarter—though this had reversed by December. While their share of bank credit also saw a pick-up, one assumes at least the home loans would be well collateralised.

Given that expenses related to the changing lifestyle would be largely missing post the second wave, household leveraging should moderate; much of the pent-up demand has been satiated, except for services perhaps, since the lockdowns have been less stringent. Hereon, spends should largely be made from current incomes and the forced savings; until the economy is on a firmer footing, one doesn’t see households leveraging themselves too much. However, should the borrowings continue to go up, relentlessly, it would call for some caution.

Meanwhile, the household-savings-to-GDP ratio that had soared to 21% in June 2020—a one-off caused by the lack of opportunities to spend during the lockdown—trended down to 10.4% in September and 8.2% in December. The absolute savings amount had jumped to Rs 8.16 lakh crore in the June quarter, a four-fold increase over the June quarter of 2019; in contrast, the GDP during the quarter had collapsed to Rs 38.9 lakh crore, compared with Rs 50 lakh crore in June 2019.

As the economy opened up, borrowings from banks and NBFCs picked up, leaving the net savings smaller. While savings moderated—there was noticeable fall in currency holdings and mutual funds, bank deposits continued to grow indicating it remains the preferred savings avenue for many.

Having tapered off to 8.2% in the December 2020 quarter, the savings ratio should, as the economy opens up further, revert to the mean and closer to the historical average of about 7.5% of GDP. The smaller contractions in the private financial expenditure are in sync with the falling savings ratio. The trend should persist as the festive and wedding seasons approach—and the vaccination drive progresses—allowing consumers to spend more freely. While savings are, no doubt, important for the economy, right now, it is critical consumers spend so that the troubled sectors—including large ones like automobiles—recover quickly. Given we are above the trend rate, and comfortably placed, consumption would help the economy far more at this point.

Consider the fact that even with Open Market Operations (OMOs) of just Rs 3 lakh crore last fiscal, RBI was able to push through a record quantum of government borrowings of a net Rs 13.2 lakh crore; in earlier years, RBI has needed to conduct OMOs of a similar quantity to facilitate a far smaller quantum of government borrowings. The biggest chunk of financial savings is usually in the form of bank deposits—a little over 50%—though the amounts do tend to vary from quarter to quarter, for reasons that are not always clear; for instance, between September and December last year, the share of household-deposits-to-GDP fell from 7.7% to 3%.

Nonetheless, banks have been inundated with deposits, and since loan growth is languishing at multi-year lows, they are sitting on surpluses of Rs 4-5 lakh crore. Interestingly, there has been much greater enthusiasm for the stock markets and mutual funds over the past year; the share of savings in equities has more than trebled from 0.4% of GDP in FY20 to 1.3% of GDP in December 2020. This is not wholly unexpected given the meagre returns from bank deposits. Moreover, the higher penetration of the internet and the availability of smartphones has seen a sizeable portion of the investments and trading volumes coming in from Tier II and Tier III cities. In the process, businesses have been able to raise capital. Again, with real interest rates on bank deposits having turned negative, there seems to be a shift to small savings; excluding PPF, these accounted for 1.4% of GDP at the end of December 2020, up from 1.1% in March, 2019 and 1.3% in March, 2020. Hopefully, the government will put these savings to good use.