By Sonal Varma & Aurodeep Nandi

Our current baseline projection for FY22 (year-end March 2022) GDP growth is 13.5% yo-y, up from an estimated -7.4% in FY21. This is underpinned by medium-term tailwinds from the lagged impact of easy financial conditions, fiscal activism, strong global growth and continued vaccine momentum alongside activity normalisation. Our annual growth assumptions are based on expectation of GDP growth picking up to 1.0% y-o-y in Q1 2021 from 0.4% in Q4 2020, before escalating to 34.5% in Q2, reflecting favourable base effects. This inherently projects sequential momentum of 4.3% q-o-q (sa) in Q1 (from 6.3% in Q4), which subsequently moderates to 0.5% in Q2.

How will the second wave impact our growth forecasts? High-frequency data suggest mobility and traffic indicators are being impacted, especially in the worst-affected state of Maharashtra. On a national scale, there is evidence that passengers are reluctant to travel due to the second wave, while industrial sectors appear to be chugging along well.

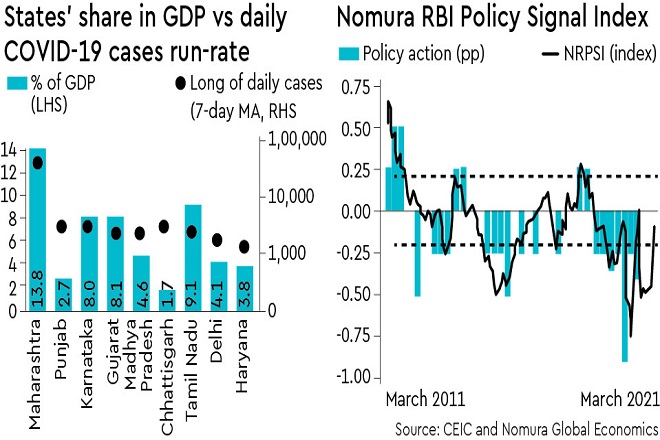

Consequently, the sectors of the economy that seem most at risk from a second wave are hotels & restaurants and transportation. Hospitality accounts for ~1.1% of GVA, while road, railways, air and water transportation and incidentals cumulatively account for ~4.6% of GVA, with road transport leading the pack at ~3.1% of GVA. So overall, the ‘high risk’ proportion of the economy (at risk from a second wave) amounts to ~5.7% of GVA. The rest of the economy—agriculture, industry and services like construction, communication, trade—should remain largely resilient to these shocks. The accompanying graphic shows the share of national GDP of the most affected states against the current daily rate of new cases.

At one end of the spectrum is Maharashtra at ~14% of national GDP; it dwarfs other states in terms of daily case rates, the severity of lockdowns and the impact on high-frequency data. The next worst affected state of Punjab accounts for 2.7% of GDP, while the others with relatively high case rates cumulatively account for ~31.5% of GDP. Even in the extreme and improbable situation of a complete halt of hospitality and transportation services in Maharashtra and Punjab, the impact would probably amount to less than 1% of GVA.

In our view, since the second wave started only towards the end of March, and as the economy normalised rapidly in January and February, the second wave is unlikely to have a major impact on Q1 GDP growth, and our estimate of 1.0% y-o-y appears reasonable.

However, if the second wave worsens further, causing more state-level restrictions and a moderation in contact services (all of which appear likely over the next 1-3 months), then the sequential momentum in Q2 (April-June) will likely be close to zero or marginally negative (relative to our forecast of 0.5% q-o-q sa). This would mean year-on-year GDP growth of around 32.5% in Q2 (versus 34.5% in our baseline) and FY22 GDP growth closer to 12.2% (versus 13.5% in our baseline), both of which are still above the RBI’s projection of 10.5%. The hit to growth in the near term, therefore, is likely to be marginal at ~2pp in Q2, and the drag on FY22 GDP growth could be ~1.3pp relative to our baseline (of 13.5%), although we will await more information to finalise our gauge of the economic impact.

There are a number of reasons why we expect the economic impact in the short term to be muted. The economy appears to have become far more resilient and consumer and businesses have adapted to the new normal. Lockdown measures are likely to be more localised and less draconian. The goods sector is likely to continue to recover and vaccinations are progressing, which is a major offset against rising new infections.

Given the renewed uncertainty over the growth outlook due to the second wave, it is natural that markets would expect RBI to further delay its normalisation of rates and liquidity. Indeed, in recent comments, Governor Das mentioned that, even as the RBI is likely to maintain its FY22 growth projection of 10.5% y-o-y (Nomura: 13.5%), the economy is “not out of the woods yet” and that the RBI remains “fully committed to use all [of its] policy tools to secure a robust recovery”, which suggests the accommodative stance will be maintained at the April 7 policy meeting.

Interestingly, the Nomura RBI Policy Signal Index (NRPSI) jumped from rate cut territory of -0.44 in February (no change is between -0.20 and 0.20), to neutral territory of -0.09 in March.

This was primarily driven by the recent rise in oil prices, as well as the lagged impact from GDP growth returning to positive territory in Q4 2020. This suggests that, while there are near-term growth concerns/uncertainty due to rising infection cases, fundamentally, the economy is approaching a policy inflection point and growth-inflation dynamics are gradually turning in the direction of policy normalisation.

For the next policy meeting on April 7, we expect RBI to maintain the policy status quo, both to policy rates as well as its ‘accommodative’ stance. The forward guidance at this meeting will likely be updated, given existing guidance of ensuring an accommodative stance “into the next financial year” will have run its course. The RBI may choose to maintain its preference for time-based forward guidance, which can help push back against market expectations of near-term normalisation. However, in an environment of impending policy normalisation, this could also constrain its policy options, especially if upside risks to inflation materialise. Alternatively, RBI may opt to shift gears to outcome-based guidance, with a more open-ended objective of a growth revival, while keeping inflation within target. This would provide RBI with more policy maneuverability but comes with the trade-off of ambiguous guidance.

For now, while policy normalisation is not a key focus due to the second wave risks, we believe that the medium-term trend is one of policy normalisation. In our base case, we expect RBI to leave its policy repo rate unchanged through 2021, as the output gap stays negative (despite the cyclical recovery) and as inflation remains within RBI’s band of 4% +/-2% (although above the 4% target). However, we expect the process of liquidity normalisation to begin in mid-2021, the policy stance to shift to ‘neutral’ from ‘accommodative’ in Q3 (July-September), and a 25bp reverse repo rate hike in Q4. This is likely to be followed by 50bp worth of repo rate hikes in H1 2022, with risks skewed towards further hikes.

(Edited excerpts from Nomura’s Asia Insights report dated April 1, 2021)

Varma is chief economist, India and Asia ex-Japan, and Nandi is India economist, Nomura. Views are personal