Rapid changes in the Union-state fiscal landscape are receiving increasing attention from scholars and policy makers. Abolishing the Planning Commission and creating the NITI Aayog, changes in the nature and quantum of centrally-sponsored schemes, the award of the 14th Finance Commission and the terms of reference of the 15th Finance Commission, have all generated new debates. Arvind Subramanian, who recently demitted office as Chief Economic Adviser (CEA)—in a public debate in Mumbai in July —suggested a new framework for Finance Commission transfers. He had written on the this in the Economic Survey 2016-17. More recently, in Business Standard, he presented a new framework for the Commissions’ transfers even as he described the 14th Finance Commission award as a ‘game-changer’. Subramanian’s emphasis for changing the framework by the Finance Commissions underlines the fact that the dynamics of Union-state relationships need to be debated upon . According to him, the new framework of transfer should satisfy the objective of redistribution and risk sharing in response to shocks and should incentivise better performance by states. He suggests that the transfer system should be divided into four ‘pots’, viz., return or true devolution; redistribution, risk sharing and reward and incentivisation.

As per Subramanian, “return or true devolution” is “what gets returned to the states as their share of the tax base” and this can be approximated by nominal GSDP. This needs to be viewed in light of the intent of principles of intergovernmental transfers and constitutional provisions. As is well known, unconditional transfers are given to the states to enable them to provide comparable levels of public services at comparable tax effort. This implies that the objective of such transfers is to offset revenue and cost disabilities of states. In recognition of this, the founding fathers of the Constitution made the provision for an independent Finance Commission to act as an arbiter for the sharing of Union taxes.

There are three major concerns with Subramanian’s approach. First, GSDP may be related to, but does not represent, states’ tax bases and, therefore, does not tantamount to “return”. The states’ tax bases predominantly comprise marketed consumption that is different from GSDP. Second, if tax collection, instead of GSDP, is taken as a proxy, it doesn’t represent tax accrual. Many businesses pay tax and file their returns in big cities although the production/distribution activities are spread in other states. Finally, there is a more fundamental objection, that it violates the objective of offsetting revenue disabilities.

The Constitution assigns all broad-based and mobile taxes to the Centre for reasons of comparative advantage, but these need to be distributed amongst the states for the latter to carry out their constitutionally mandated functions. It is not about paying back a particular state based on collection; it is to compensate for the shortfall in revenue capacity and meet expenditure needs. Source of collection is irrelevant here. The objective of federal transfer is fiscal equalisation. Besides, the basis of estimating the states’ shares raises conceptual difficulties due to the difference between collection and accrual. How does one allocate customs duty? Every state doesn’t have an international border. Should those without forgo a share? Similar arguments can be made in the case of both personal and corporate income taxes. Taxes are paid in places where the returns are filed; this may be different from where the income is accrued. The second issue is the desirability of such a proposition. Some history is worth highlighting here. The “collection” factor, with weightage varying between 10% and 20%, was used for tax sharing by the 1st to the 9th Finance Commissions for income tax. The 10th Finance Commission discontinued it, stating:

“The generation of income, especially non-agriculture income, is a spatially interdependent activity. An input being produced in a specific place may be using inputs produced in various other locations. The income generated from the sale of this output also depends on the income of consumers who may be spatially dispersed throughout the country. The country as a whole represents a common economic space and market, and growing interdependence in economic activities has considerably weakened the case of locally originating incomes in the non-agricultural sector”.

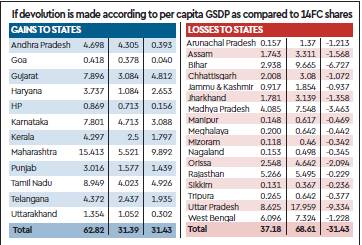

What would true devolution mean in terms of numbers? If we compare the shares of GSDP of each state with the share recommended by the 14th Finance Commission, and if ‘true devolution” is introduced, the 10 richest states would claim 62.83% and the shares of those at the bottom rung of per-capita income would be reduced to 37.18%. Even a fraction of tax devolution by way of so called “true devolution” would mean significant erosion of the principle of offsetting revenue disability.

From an operational point of view, if the principle offsetting revenue disabilities are diluted in tax devolution, the burden of offsetting the disabilities will fall on the grants. Who, then, will decide on the principles of grant distribution and its quantum? Empirical evidence shows that the grants for the Central schemes do not offset fiscal disabilities. Besides, it will relegate the states into mere agencies of the Union government.

On the issue of risk-sharing, the 13th Finance Commission had suggested the following mechanism: “macroeconomic stabilisation and counter-recessionary actions are the primary responsibility of the Central Government. It is true that the implementation of counter-recessionary measures has, to some extent, been customised, requiring measures which the State Governments are best placed to implement.

However, the associated fiscal costs should be borne nationally and hence, be financed by the Centre. This is because the desired outcomes–macroeconomic stability and maintenance of the highest possible growth rate–are targets that need to be secured nationally”. In any case, the Commissions since the 9th have been giving separate grants for disaster relief as required in their term of reference and there is no justification for a separate “pot” in the devolution.

Finally, on local government transfers and service delivery, the Finance Commission’s Constitutional role is only supplementary. Article 280 (bb and C) requires it to only make recommendations on “the measures needed to augment the Consolidated Fund of State to supplement the resources of the Panchayats and Municipalities in the State on the basis of the recommendations made by the Finance Commission of the State”. It is only about recommending measures to augment resources and not about providing resources. Of course, the Commissions have been giving grants to the local bodies, but this must be seen as supplementary, and the larger responsibility for funding them lies with the states. Besides, if the devolution has to accommodate this “pot”, are we not proposing a one size fits all decentralisation? This, in a way, is recentralisation through Finance Commission transfers.

Finally, the role of Finance Commissions, as described by Subramanian, is certainly not making awards “politically satisfying”. The founding fathers desired the Commission to be an expert body to make recommendations in a fair and equitable manner, and it is for this reason that the successive Commissions have earned respectability by performing their Constitutional role admirably and have stood the test of time.

The author is a Professor, National Institute of Public Finance and Policy; was the economic advisor to the Fourteenth Finance Commission Email: pinaki.chakraborty@nipfp.org.in