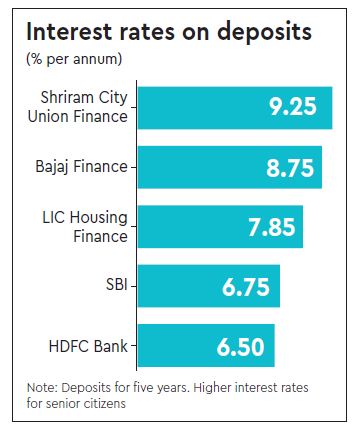

Non-banking financial companies (NBFCs) and housing finance companies (HFCs) faced with a liquidity crisis are offering higher interest rates to retail investors on fixed deposits to raise funds. They are offering interest rate of up to 9.25% on deposits for five years. In contrast, the country’s largest lender, the State Bank of India, is offering 6.85% for five-year tenor.

Leading NBFC Shriram City Union Finance is offering 9.25% interest for five-year deposits, 9% for 3-year deposits and 8.25% for one-year deposits. Similarly, Bajaj Finance is offering 8.75% for five-year deposits.

Liquidity crunch

Banks were one of the major sources of funds for NBFCs. But following a series of defaults by ILFS, banks have become cautious in lending to all NBFCs and HFCs. They fear an asset-liability mismatch in the operations of NBFCs and HFCs. As a result, the margins of NBFCs have taken a hit and sourcing of funds has become tough. Around half of funding requirement of HBFCs comes from banks followed by debt market and retail deposits.

As the cost of funds for NBFCs is lower when they borrow from banks and debt markets, the liquidity crunch has raised their cost of funds. The liquidity crunch had also prompted finance ministry to push Reserve Bank of India to ease norms for bank funding to NBFCs.

Look before you leap

Retail investors must analyse the company before investing in its deposits. They must look at credit ratings, assets and liabilities and record of servicing debts. If the rating of the company is AAA, then it means it is a safe and secure investment. If the rating is lower, there could be risks involved.

Even after investing, investors must check the ratings of the company regularly and be cautious if there is any downgrade. For NBFCs, RBI has made it mandatory to have an ‘A’ rating to be eligible to accept public deposits. If one invests in an unrated or low-rated deposit, the risks are high. It is better to ignore the unrated companies and deposit schemes of little-known companies.

Also read: How to apply for petrol pump dealership: Key things to know as oil PSUs set to open 55,000 new retail outlets

Joydeep Sen, founder, wiseinvestor.in, says while fundamentally there are issues with NBFCs like asset liability mismatch, that has always been the case. “What is happening currently is about sentiments; over the next few months, as and when there is no further default after IL&FS, sentiments will normalise. Investors can go for AAA rated NBFCs with a good track record, i.e., goodwill, and diversify the portfolio for risk management.”

Unsecured loans

As company fixed deposits are unsecured loans, repayment of principal and interest are not guaranteed, and in case of any default or delay, investors have little recourse. Corporate deposits carry default risk in case of large-scale premature withdrawal by investors or if the company is passing through a financial crisis.

However, as per the provisions of Section 58-A of the Companies Act, 1956, if the company is winding up, then it will give first preference of repayment to the equity shareholders rather than fixed deposit holders. Bank deposits provide security of up to an investment of Rs 1 lakh, which is not the case with corporate fixed deposits.

Also read: India’s GDP growth to fall from 8.2% in Q2; here’s what economists say

Tax and interest payments

Company deposits pay interest at monthly, quarterly or yearly intervals and income tax is deducted at source if the interest paid is over Rs 5,000 in a financial year. For bank deposits, TDS is deducted if the interest income is over Rs 10,000 a year. An investor will have to pay tax on the interest earned for bank and NBFC deposits at one’s marginal rate.

The tenure of company deposits ranges from one to seven years and one can earn compounding interest by reinvesting the principal amount along with the interest earned. Investors can get direct ECS credit facility for interest payments or advance interest warrants for the year. However, unless one needs income regularly, they should prefer cumulative schemes to regular income options since the interest earned gets reinvested at the same coupon rate, resulting in better yields.