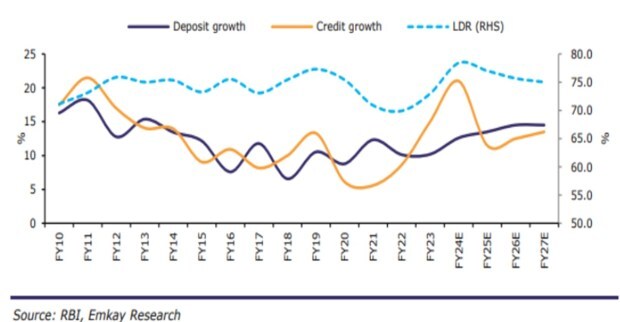

The credit growth trajectory is expected to slow down to 12-14 per cent on-year over FY25-27E from the current ~16.5 per cent YoY (21 per cent incl-HDFC), stated a report by Emkay Institutional Equities. The report also expects that the loan-to-deposit ratio (LDR) will drop to 75 per cent from a current high of 80 per cent. It further added that the overall deposit growth and more so slowing retail deposit growth (including SA) could emerge as a structural risk to India’s long term retail credit growth story, unless it is addressed.

The Emkay report stated that some of the banks have reduced the excess cash on the balance sheet to fund credit growth in the recent period, thereby delaying deposit growth and protecting margins. However, most of these levers are now largely exhausted and thus, it added, banks will have to mobilize deposits to incrementally fund credit growth. Emkay Institutional Equities cited that banks’ preference for low-cost deposits is likely to remain high and, thus, accelerating deposit growth is imperative for banks to support credit growth in the long run.

Anand Dama, Senior Analyst BFSI, Emkay Global Financial Services, said “The extended elevated rate cycle and, thus, higher funding cost coupled with rising asset-quality risk in unsecured retail loans contributing 12 per cent of YTD credit growth has raised concerns about profitable lending. The recent RBI’s actions to contain the bank’s undeterred growth in unsecured/NBFC loans has instilled fear amongst the lending institutions. Every bank will need to find its method for winning or at least surviving the retail deposit war.”

He further added, “Some of these solutions could include concentrating on the expanding branch network (metro + SURU with a focus on the Hindi Heartland, given its strong growth potential) along with a focus on corporate salary, community banking, self-funding ratio, capturing corporate/SME customer flow via transaction banking/CMS and retail customer cash flow via wealth management and so on.”

Per the Emkay Institutional Equities, private sector banks like HDFC Bank, ICICI Bank, Axis Bank, IndusInd Bank and IDFC Bank are in a branch expansion mode and have identified their niche focus areas to mobilize retail deposits, but public sector banks, except the likes of SBI and BOB, still lag and could suffer in the long run.

Seshadri Sen, Head of Research and Strategist, Emkay Global Financial Services, said “The Indian banking sector is structurally in stronger shape to ride the retail credit growth story over the next decade, amid rising consumerism. However, funding such growth via retail deposits at a reasonable cost among rising structural disruptions could emerge as the biggest challenge. PSBs may see near-term gain, but PVBs will be the winners in the long term amid the raging retail deposit war.”

Money supply has slowed down over the past decade

The report stated that the Broader Money Supply (M3) growth and deposit growth in the Indian banking system have settled at a lower level (<15 per cent) over the past decade and even slipped below 10 per cent for a few years, leading to current liquidity tightness. This, it said, is attributed to prolonged sluggish credit growth to the commercial sector (since FY14) and lower net forex asset growth for the banking sector.

However, Emkay Institutional Equities expects the lagged impact of healthy credit growth over the past two years coupled with higher interest rates offered by banks should gradually reflect via some improvement in M3 and deposit growth in the near-medium term, and long-term money supply growth will be conditioned to sustained strong credit growth and easing monetary policy by the RBI.