Income Tax simple definition: Wondering what is income tax and how does it work? Income tax in India is a tax paid by individuals or entities depending on the level of earnings or gains during a financial year. The earnings may be both actual and notional. The Government of India decides the rate of income tax as well as income tax slabs on which individuals are taxed. Those under higher income slabs are taxed at higher rates. The taxable income slabs are changed from time to time, keeping in mind the price levels. Sometimes, the government also provides income tax rebates, which benefit people in the lower-income group. To collect long-term funds, the government also provides income tax incentives. The amount invested in tax-saving schemes is deducted from gross income, which reduces the amount of taxable income and benefits the taxpayer.

In case the actual tax payable is less than either the amount of advance tax paid or the amount of TDS for the corresponding year, the assessee may claim the excess tax back by filing the appropriate ITR Form. Once the ITR is verified, the income tax refund is processed if the Income Tax Department finds that the claim is genuine.

What type of tax is an income tax? What type of income is taxable in India?

Income tax in India is a direct tax on the income or earnings in a financial year. Below are some types of incomes and their taxation rules in India:

- Income from salary/pension: This includes basic salary, taxable allowances, perquisites, and profit in lieu of salary, as well as pension received by the person who himself/herself has retired from the service. Incomes from salary and pension are included in the computation of taxable income.

- Income from business/profession: This includes actual and presumptive incomes from business and professions that individuals do in their personal capacity and is added to taxable income after adjustment of the deductions allowed.

- Income from house property: An income tax assessee can own one or more house properties. These house properties can be self-occupied or rented out or even vacant. This head describes the rules relating to such ownership. The rules under this head describe how rent from one or more house properties is to be treated for the purpose of calculation of taxable income. It also describes how interest on home loan is to be accounted for in the case of self-occupied, rented out and vacant properties. An income tax assessee can claim certain deductions such as municipal taxes and a standard deduction for house maintenance in certain cases. The final net income or loss under this head is then added to or deducted from the income from the other heads.

- Income from other sources: This includes incomes like interest from a savings account, fixed deposits (FDs), family pension etc, which are included in the taxable income.

- Income from Lottery, Betting, Race Horse etc: Such incomes are included in the total income, but excluded from taxable income as different tax rates are applicable on these types of income.

- Capital Gain: Capital gains arise at the time of selling capital assets like gold, house properties, stocks, securities, mutual fund units etc. Depending on the types of capital assets and the period of holding, gains on the sale of such assets are categorised as short-term and long-term capital gains. Although capital gains are part of income tax, they are not added to taxable income, because except short-term capital gains on the sale of debt funds, other gains are taxed at different rates.

Who is eligible for income tax?

As income tax is based on one’s ability to pay it, different tax rates are applied to different income slabs, which is revised by the government from time to time. Currently, there is zero per cent tax on taxable income up to Rs 2,50,000, 5 per cent tax is levied on taxable income between Rs 2.5 lakh and Rs 5 lakh, 20 per cent tax is levied on taxable income between Rs 5 lakh to Rs 10 lakh. For taxable income above Rs 10 lakh, 30 per cent is the applicable rate.

On the tax payable, 4 per cent Health and Education cess is also charged. Moreover, 10 per cent surcharge is levied on income between Rs 50 lakh and Rs 1 crore and 15 per cent surcharge is levied on income over Rs 1 crore. Tax rebate (under section 87A) up to Rs 12,500 is provided to the assessees having total income after Deductions up to Rs 5 lakh. However, usual tax computation will be applied in case the taxable income exceeds Rs 5 lakh limit.

How is income tax calculated in India?

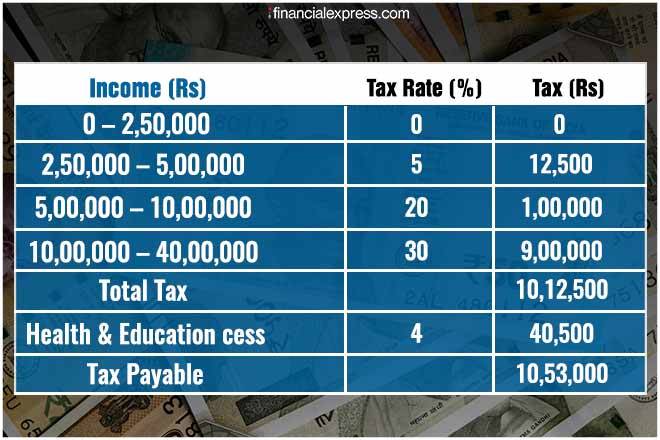

Income tax in India is calculated on the basis of tax rates determined by the government for an Assessment Year (AY). For example: For AY 2019-20 (Financial Year 2018-19), the tax payable may be calculated in the following way:

Once the gross total income is calculated by adding all the above sources, whichever applicable, deductions on account of tax-saving investments, allowed expenses, donations etc are adjusted. The main sections under which Income Tax deductions in India are allowed include up to Rs 1.5 lakh under sections 80C, 80CCD, 80CCD(1), 80CCD(2) and 80CCG combined; up to Rs 50,000 u/s 80CCD(1B); up to Rs 1 lakh u/s 80D and 80E, 80EE, 80G, 80TTA.

After the entire eligible deduction amount is reduced from the gross income, the figure of taxable income is arrived at. The income tax amount that is payable is computed on the basis of taxable income. Now, suppose, if a person’s taxable income is Rs 40 lakh, his tax payable for the AY 2019-20 (FY 2018-19) will be calculated as:

Income Tax Return forms in India:

Filing of Income Tax Return (ITR) is compulsory for earning individuals or entities, depending on their earning capacity. The Income Tax Return needs to be filed on prescribed ITR Forms. For AY 2019-20, there are six ITR Forms: ITR-1, ITR-2, ITR-3, ITR-4, ITR-5 and ITR-7.

- ITR-1: This ITR form is also called Saral and is for resident Indians having Income from Salaries, one House Property, Other Sources (interest, family pension etc.), and Agricultural Income up to Rs 5,000. This form does not apply to an individual who has invested in Unlisted Equity Shares or is a Director in a company or has a total income of over Rs 50 lakh.

- ITR-2: This ITR form is applicable to Individuals and HUFs who don’t have income from profits and gains of business or profession.

- ITR-3: Individuals and HUFs having income from profits and gains of business or profession need to use this form.

- ITR-4: This form applies to resident Indian Individuals, HUFs and Firms (other than LLP) having income from Business and Profession up to Rs 50 lakh, which is computed under sections 44AD, 44ADA or 44AE. An Individual, who is either a Director in a company or has invested in Unlisted Equity Shares, can’t use this form.

- ITR-5: This form applies to assessees other than Individual, HUF, Company, and persons filing the ITR-7 Form.

- ITR-7: This form is applicable for the persons, including companies, who required to furnish return under sections 139(4A) or 139(4B) or 139(4C) or 139(4D) of the Income Tax Act.

What is income tax used for? Why income tax is important for the Government of India?

According to estimates, about 71 per cent of the government’s total revenues are collected through taxes and duties, while nine per cent come from non-tax revenues, and the rest of about 20 per cent are covered through borrowings and other liabilities. The revenue collected by the government is used in various ways, like paying states’ share of taxes and duties, interest payments, expenditure on central sector schemes and centrally sponsored schemes, pension to retired government employees, defence expenditures, subsidies, expenses through finance commission, transfers, etc.