By Manoj Kumar Upadhyay

Potential of Wind Energy in India

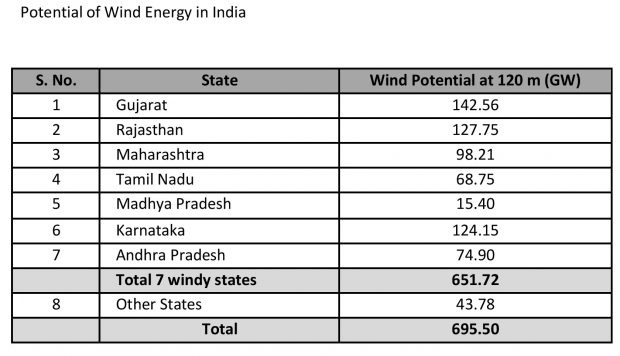

Wind is an intermittent and site-specific resource of energy and therefore an extensive Wind Resource Assessment is essential for the selection of potential sites. The Government of India (GoI), through National Institute of Wind Energy (NIWE), has installed over 800 wind-monitoring stations all over the country and issued wind potential maps at 50m, 80m, 100m and 120m above ground level. The recent assessment indicates a gross wind power potential of 695.50 GW at 120 meter above ground level.

Wind Installed Capacity

India’s wind energy sector is led by indigenous wind power industry and has shown consistent progress. The expansion of the wind industry has resulted in a strong ecosystem, project operation capabilities and manufacturing base of 10,000+ MW per annum. The country currently has the fourth highest wind installed capacity in the world with total installed capacity of 39.87 GW (as on 30 th Sept. 2021) which is about 66% of the wind capacity target of 60 GW under 175 GW RE target by 2022. The wind generated was around 24.57 Billion Units during April-July, 2021.

Government Policies to promote Wind Sector

The Government is promoting wind power projects in entire country through private sector investment by providing various fiscal and financial incentives such as Accelerated Depreciation benefit; concessional custom duty exemption on certain components of wind electric generators. Besides, Generation Based Incentive (GBI) Scheme was available for the wind projects commissioned before 31 st March 2017.

In addition to fiscal and other incentives as stated above, following steps also have been taken to promote installation of wind capacity in the country:

- Technical support including wind resource assessment and identification of potential sites through the National Institute of Wind Energy, Chennai.

- In order to facilitate inter-state sale of wind power, the inter-state transmission charges have been waived off for wind projects to be commissioned by June, 2025.

- Issued Guidelines for Tariff Based Competitive Bidding Process for Procurement of Power from Grid Connected Wind Power Projects.

Challenges

The wind power sector is an important component in India’s plans to decarbonise its power sector. Wind power target set by GoI is 60 GW out of 175 GW target of installed renewable energy (RE) capacity by 2022 and 140 GW out of 450 GW RE target by 2030.

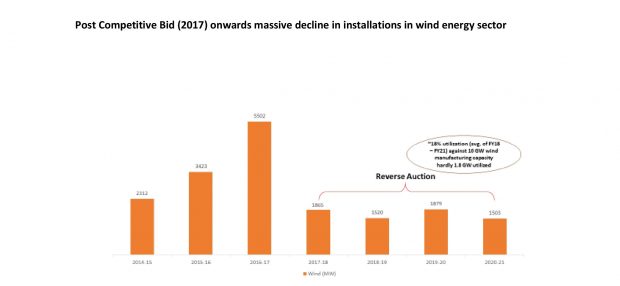

However, India’s wind power sector is struggling to match the growth of the solar sector and since 2017 and it has not been able to achieve its annual capacity installation target. The wind power industry and experts highlight that the reason for the stagnation is the shift to reverse auction route in the wind sector, lack of financial incentives and difficulties in finding land at windy sites and power evacuation infrastructure for the projects.

Reverse Bidding, Land & PLF issues

- For winning the bids under the current reverse bidding process, the investors are bidding in only the highest PLF states to win the bid as discovery of the lower tariff i.e. below Rs. 3.00 per Kwh as above this tariff Discom’s are not willing to enter into long term power purchase agreement (PPA) . This scenario is resulting in low capacity addition (approx 1.50 GW per annum) in India in the last 5 years.

- There are constraints to install beyond 1.5-2.0 GW per annum of Wind Energy projects in any State because of challenges related to land availability & RoW, power evacuation, grid capacity, logistics constraints and infrastructure capability.

- Concentration of projects create severe pressure on land and power evacuation infrastructure creation which leads to choking situation as witnessed in Gujarat.

- This is creating execution challenges at the state level and not able to generate volumes.

- In spite of land and infrastructure available in other States, investors do not prefer states like MP, Rajasthan and Maharashtra as the proposed Projects cannot compete on PLF & reverse auction economics basis in comparison to projects in Gujarat and Tamil Nadu.

- Because of reverse bidding, we are not able to utilise seven windy states, wherein each wind state has capability to deliver 2 GW per annum. So, if we can use all the seven windy states, we will be able to build 14 GW per annum. Due to the current reverse bidding process, we cannot build more than 1.5 GW to 2 GW per annum of wind power projects.

- While approx. 28.1 GW of capacity bidding has been done since Feb, 2017 (5 years since auction regime), approx.19.7 GW of wind capacity has been allotted, out of which only about ~4.5 GW of capacity has been commissioned so far.

- At present, states are trying to avoid the Captive projects to be set up, due to loss of their revenue stream by power intensive industrial customers.

- The above slow development has led to reduction in number of domestic Wind turbine manufacturers from 12 – 13 to 4 – 5 and in-turn reduction of the number of MSMEs engaged in the wind sector from 4000 to about 1000 and reduction in jobs in the wind energy sector from 2 Million to about 63,000.

It has been observed that the reverse bidding is not very successful in the projects where project components are supplied from domestic manufacturing. In India, the reverse bidding has impacted domestic manufacturing & export based wind sector and also it was not very successful in the earlier coal mines auctions.

GST rate

- The GST rate on wind turbine has been increased from 5% to 12% w.e.f. 1st Oct’21 which has become an additional 7% cost in the wind turbine as there is no pass through.

- This will result in further slowdown of the wind turbine manufacturing and capacity additions over the next 18 months besides lower participation in the upcoming bids by prospective bidders/investors due to decreased returns.

Wheeling Charges & Captive use

- Currently all states with viable wind resource have different wheeling, transmission and banking policies; in few of the states these policies changes very frequently on yearly basis, Recently APTEL vide its Judgement dated January 28, 2021 also directed CEA to come up with a uniform banking procedure which will be followed by all the States.

- MoP amended order dated 21st June, 2021 for waiver of ISTS charges further creates ambiguity w.r.t. its applicability to Captive and third party users and waiver of transmission losses to the stakeholders.

- Investors are not opting for captive option even when Third Party Consumer consumers with > 1 MW project are allowed because of high cost due to Wheeling & Transmission Charges and Losses, Banking Charges and its frequent changes by various states through SERCs and due to poor enforceability of RPO compliance.

Suggestions

To utilize current 10+ GW per annum of domestic Wind Turbine manufacturing capacity & reviving the Indian Wind industry under ‘Aatmanirbhar Bharat’, the following actions are needed from MNRE & Ministry of Power:

Change in the current Bidding Mechanism:

- Wind and solar are two different technologies and should be treated differently. Solar power generation in day time i.e. 8 am to 5 pm while the peak power demand across the country is between 5 pm to 8 am during which wind generates ~70 percent power. Therefore, unless wind power grows, the grid will starve post 5 pm and we will see power cuts as being experienced by USA and few other countries, thus pushing the grid towards instability resulting in blackouts.

- Unlike solar, wind power development cost varies from state to state. There is a need to develop the wind project site, collect data and then carry out biddings. (At present, calling for bids anywhere in India on a competitive basis with ceiling prices is resulting in lop-sided development).

- Currently, the PLF of wind power in our country is varying in the range of 35% to 43% across sites in 7 windy states. NIWE should assess base tariff in various states based on wind resources & PLF availability in those states. Further, STU & CTU needs to create power evacuation facilities as per the potential mapped by NIWE and super highway grids should be planned & developed looking to the gigapower generation requirements coming up under Green Hydrogen & Green Ammonia segment.

- Reverse bidding has adversely impacted domestic wind manufacturing sector similar to what was experienced earlier in the coal mines auction.

- Therefore, current reverse bidding mechanism to be replaced by closed transparent bidding where each bidder should submit tariff only one time and right to revision of the price option (no reverse auction) should be dropped. The tariff threshold for closed tender may be fixed in conjunction with the state wise tariff to be fixed by CERC in consultation with NIWE on the basis of wind resource assessment of each wind zone & average power procurement cost of the States DISCOMs.

- SECI to sign the PPA with interested Bidders/Investors at a tariff submitted under the closed transparent bidding for different sites & states and bundle this power and sell same to Discom(s) at an average tariff of these seven windy states.

- A single tender should cover the installation requirements of seven states and for each state, capacity should be capped at 2 GW. The bidder should also be given choice to bid for maximum up to 2 GW in not more than 2 states with a max. cap of 50% of defined individual state capacity as per tender. The penalty for non-execution of the project to be increased to 10% of the project cost. This will attract serious investors while giving flexibility to the bidders to offer sites and volume of work as per their choice. Further, every bidding state will get equitable chance for the development of its green energy portfolio unlike as per current scenario.

- Mandatory wind specific RPO & its strict enforceability with heavy penalty mechanism.

- To enable MSMEs to hedge their power cost for 25 years, uniform policy on charges / losses for wheeling, and transmission and banking is required for captive power consumers.

- Besides the above other existing cost/charges like Wheeling and Transmission losses, Electricity Duty, Cross Subsidy Charges and Additional Surcharge for respective RE project as applied by various states should be waived uniformly for MSME category.

- Captive installed capacity of Wind should not be restricted to the Contract Demand or a percentage (%) of the Contract Demand.

- 5% GST should be introduced on sale of Renewable Power. This will complete the loop as currently there is no GST cost pass through.

Way Forward

With above suggestions, the projects can also be planned in low and medium windy sites such as Rajasthan, MP and Maharashtra etc. where no major wind project development has taken place since last 3 years, which was earlier a normal development for the state. Further, already closed wind turbine & component manufacturing facilities in low windy states can be revived as per above suggestions, which will in-turn create job opportunities.

The author is Deputy Adviser, NITI Aayog. Views are personal

(Disclaimer: This article is intended to inform decision-makers in the public, private and third sectors. The views of writers are personal and it does not represent the views of either the Government of India or NITI Aayog. They are intended to stimulate healthy debate and deliberation in power sector. The data are taken from published source, MNRE/ CEA/Ministry of Power website.)