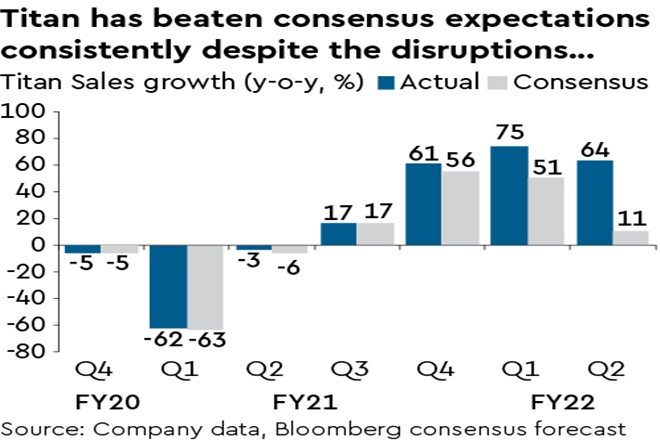

Titan delivered exceptional sales for Q2: (i) Jewellery rose by 78% y-o-y on strong pent-up demand as the network rollout picked up pace with 13 new Tanishq stores (net) added. (ii) Watches were up 73% y-o-y on recovery in walk-ins with Tier-2 cities doing better than metros. (iii) Eyewear was up 74% y-o-y with healthy growth across all segments. (iv) Taneira recorded total store operation days of 80% with all 14 stores operational. (v) CaratLane’s sales rose 95% y-o-y with two new stores. And (vi) Titan’s standalone sales were up 64% y-o-y overall, beating consensus by a wide margin.

Key concern now seems to be whether valuation is expensive: Given the stock’s run-up in the past year (up 84% vs Nifty50 gain of 55%), the biggest worry for investors now appears to be whether the valuation (FY23 PE 68x) is ahead of the fundamentals and, thus, whether there could be a risk of a derating. In our view, Titan is only midway through its evolving high growth compounding construct.

Investment case remains compelling: (i) Long-term compounding construct is well in place as Titan (6-7% market share) looks well placed to capture value from the jewellery sector’s long-term growth potential (driven by its consumer trust, brand, compelling value proposition of pricing, exchange offers, design, wedding focus) by gaining market share consistently. (ii) Unorganised to organised shift is a key tailwind as mandatory hallmarking is now another structural push for the industry to transition towards organised trade where Titan stands out. (iii) Titan is also building long-term growth options, including carefully choosing its international foray and new business such as Taneira (ethnic wear), which has begun well. (iv) We see a beginning of strong growth phase, driven by network rollout (40+ outlets per annum), strong support from wedding sales, revival in watches, eyewear, and growth accretion from Taneira. We see a decade of a potential high growth phase for Titan with a revenue CAGR of 19%. And (v) perceived expensiveness is misleading and is merely a reflection of the “long duration of growth capture” that the market is willing to assign and price to winning business models such as Titan. On our framework, the market is pricing in 15-16% long-term earnings compounding, which is well within what Titan could deliver.

Reiterate Buy and lift TP to Rs 2,650 from Rs 1,980 as we revise our estimates and, thus, long-term growth rate assumptions and roll our valuation forward.