Better toll collections across projects offset the impact of lower EPC revenues during the quarter to some extent. Increased interest expense and share of losses from SPVs impacted earnings for the quarter. Cash profit, however, remained positive. A second tranche of payment from GIC is expected shortly, with the balance expected by FY2022. We cut estimates by 9%3% for FY2022/23 to factor in higher debt and revise our fair value to Rs 145 (from Rs 150).

Retain Buy.

Results impacted by higher debt and losses from SPVs: Revenues were lower than our estimates as the impact of improvement in toll collection was offset by lower EPC revenues. Margins remained strong for both EPC and BOT segments; however, increased interest expense on higher debt and losses from SPVs resulted in lower-than-expected PAT. The company expects to complete construction on Agra-Etawah and 2 Rajasthan projects during H2FY21.

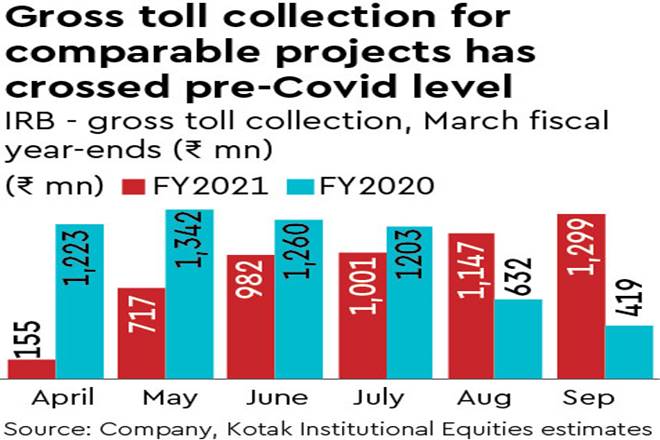

Toll collections from Mumbai-Pune and Ahmedabad-Vadodara project jumped sharply q-o-q on revival of economic activity. Net debt has moved up on consolidation of the Mumbai-Pune project and higher debt at a parent level. IRB expects gross debt to remain high during FY2021 as against earlier expectations of a decline by the year-end. Operational cash flows declined y-o-y and FCF declined on lower OCF and higher capex for the Mumbai-Pune project.

Second tranche of payment from GIC expected in Nov 2020: Of total proceeds of Rs 44 bn from GIC for a 49% stake in private InVIT, the first tranche of Rs 37.5 bn was infused during Feb, 2020 and utilised for debt reduction and construction requirement. The second tranche of Rs 2.5 bn via subscription to right issue of Rs 5.1 bn of private InVIT will come during Nov, 2020. This will be sufficient to meet the incremental equity requirements of Rs 4-4.5 bn for the portfolio. Remaining amount of Rs 4 bn will come over the next 9-12 months.

Revision in guidelines to make HAM projects attractive: IRB’s EPC order book of Rs 51 bn provides limited revenue visibility till H1FY22. Recently proposed changes in HAM project guidelines that recommend the linking of interest rates with MCLR plus 125 bps (as against bank rate plus 300 bps earlier) is expected to reduce the interest rate differential between the annuity payments and interest paid by SPVs and will make HAM projects more attractive.

Along with this, speedier release of NHAI’s proportion of payment will shore up liquidity for developers. IRB would thus be eyeing both HAM and BOT projects. We build in Rs 45 bn of order inflows for FY2021/22 for the company.

Cut estimates by 9/3% for FY22/23; retain Buy: We revise our estimates to factor in higher debt, improved toll revenues and lower EPC revenues. Net of roll forward, revised fair value stands at Rs 145 (Rs 150 earlier).