.")

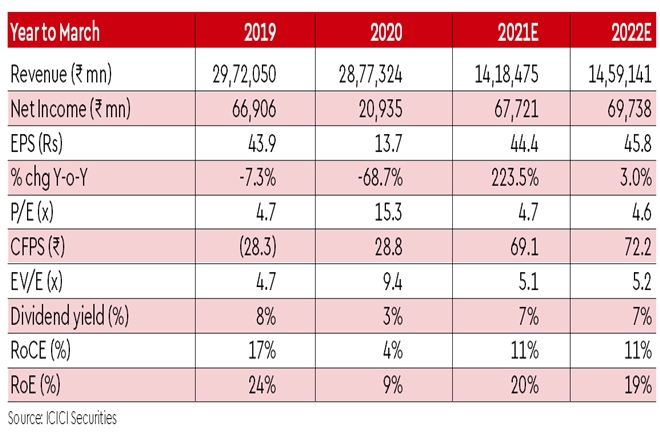

Hindustan Petroleum Corporation’s (HPCL’s) consolidated and standalone recurring EPS were in the red in Q4FY20 and down 65-69% y-o-y in FY20, both hit mainly by inventory loss vs gain in FY19. We estimate the company’s Q1FY21e EPS to be up 232% y-o-y, despite steep fall in sales volumes due to lockdown, boosted by record auto fuel marketing margins, y-o-y surge in GRM and inventory gain. Net marketing margin has recovered after being briefly in the red and the outlook for FY21 appears promising. GRM is weak, but has shown some recovery of late. HPCL has adopted the lower tax rate of 25.17%. Factoring in the lower tax rate has boosted FY21-FY22 EPS estimates by 11% and target price by 2% to Rs 278 (32% upside). Reiterate Buy.

Q4FY20 in the red due to big inventory loss: HPCL’s standalone and consolidated recurring EPS in Q4FY20 were hit by inventory loss of Rs 41.1 bn vs gain of Rs 9.2 bn in Q4FY19. Company has treated inventory loss of Rs 10 bn caused due to valuing on net realisable basis, which was lower than cost, as an exceptional item.

Reported Q4 GRM is in the red at minus $1.23/bbl, but core GRM is up 349% y-o-y at $9.5/bbl. FY20 recurring standalone EPS is down 65% y-o-y, hit mainly by inventory loss of Rs 42.5 bn vs gain of Rs 13.7 bn in FY19. FY20 consolidated recurring EPS is down 69% y-o-y and share of profit of equity accounted investee is in the red.

Q1FY21e EPS to surge 232% y-o-y: We estimate HPCL’s Q1 FY21 EPS to be up 232% y-o-y driven by: (i) record net auto fuel marketing margin of Rs 5.81/l (up 3.1x y-o-y); (ii) 7.8x y-o-y surge in GRM to $5.9/bbl (including inventory gain of $2/bbl); and (iii) product inventory gain of Rs 5.5 bn vs loss of Rs 0.2 bn in Q1FY20. This would help make up for the 36% y-o-y fall assumed in auto fuel sales volume. We are assuming the company’s crude throughput to be flat y-o-y in Q1; it was up 21% y-o-y and its utilisation rate was 101% in Apr’20.

Upside to FY21e marketing margins; downside to GRM possible, but inventory gains to boost GRM: HPCL’s FY21 net marketing margin may be higher than our estimate of Rs 2.5/l at Rs 2.75-3.0/l. Q1FY21-TD net margin is at Rs 5.81/l. We expect further retail price hikes (made since 6-Jun’20) to keep net margin at reasonable level of Rs 1.5-2.5/l in rest of Jun’20 and on 1-Jul’20. Net margin was at Rs 0.56/l on 16-Jun’20, but at current prices is likely to slip into the red on 1-Jul’20 unless further hike of Rs 3-3.6/l is made. We remain optimistic on retail price hikes as reasonable marketing margin is crucial for success of BPCL’s privatisation.

Downside to FY21e core GRM of $4.3/bbl is possible, but that including inventory gain would be in line with our estimate, or higher. HPCL is our top pick as it is best placed to gain from strength in auto fuel marketing margins and is least impacted if GRMs disappoint.