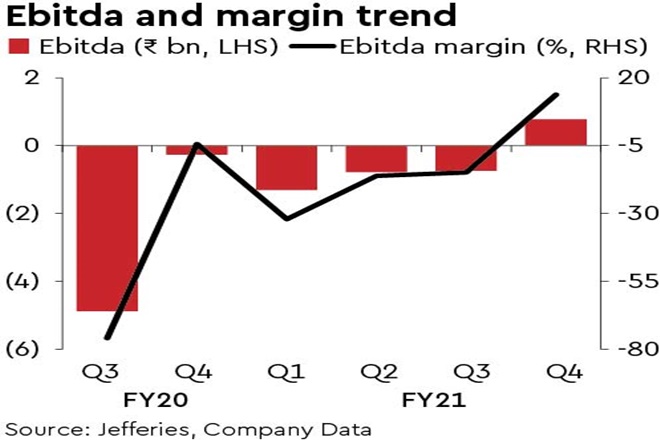

GRIL’s Q4FY21 beat JEFe and marked an Ebitda turnaround, posting an op margin of 13.8%, after 5 quarters of op losses. Capacity utilisation rose from 36% in Q1 to 75% in Q4 (41% y-o-y), suggesting better demand. Key operational metrics (sales, profitability) improved q-o-q in FY21. Electrode price recovery in Q4 led to inventory gains, aiding margins (NRV basis). Decarbonisation is a structural tailwind. We tweak FY22-24 estimates slightly, retaining EPS. Buy; PT Rs 875.

Sequential improvement: GRIL’s operational metrics improved consistently in FY21: (i) Capacity utilisation expanded from 36% in Q1 to 75% in Q4 (41% in Q4FY20); (ii) top-line growth q-o-q; (iii) Ebitda losses turned around to a healthy margin of 13.8% in Q4; (iv) traction in net profit (PAT margin at 12% in Q4); and (v) strong net cash position at Rs 27.3 bn (Rs 20.1bn as of Mar’20).

GRIL’s India business saw a good recovery in H2FY21 and delivered higher profitability. In Q4FY21, electrode prices began to recover from their lows, leading to inventory gains. In fact, GRIL posted positive Ebitda in Q4 after five quarters of operating losses. However, the company’s German operations (18,000 MT capacity) were affected by extended lockdown, lower utilisation and weaker ASPs.

Industry update: Global steel & electrode industries were affected in H1FY21 by COVID lockdowns and factory closures. However, gradual demand resumption from steel-consuming sectors supported electrode demand in H2.

Structural drivers: In April 2021 China abolished a rebate of 13% VAT on certain steel exports – thus, lower Chinese exports could be favourable for other EAF steel-producing nations. This, along with a focus on decarbonisation, could underpin Electrode demand in the longer term. Furthermore, steel industry demand is likely to be supported by structural end-user industries such as construction and automobile. Looking ahead, GRIL mgmt remains optimistic in light of the ongoing recovery in electrode demand and price stabilisation.

Key assumptions, estimates: We retain our FY22/23/24e Electrode ASPs at $6.5k/ $7.3k/ $7.5k /MT – our ASP estimates are still 40-50% below the upcycle peak of FY19. Capacity utilisation in FY22 estimated at 75% and 85%+ in FY23/24. Needle coke (key raw material) cost assumed at $2.2k-$2.3k/MT over FY22-24e. We tweak our FY22-24 estimates marginally, broadly retaining EPS.

Reiterate Buy: Commodity stocks appear to have entered an upgrade cycle after 2-3 weak years. Factoring in improving operational performance and a favourable industry outlook, we value GRIL at EV/Ebitda of 8.3x – a ~10% premium to its historical 10-year avg (vs 7.5x). GRIL’s FY23/24e P/BV stands at 1.9x / 1.5x. Reiterate Buy with revised PT of Rs 875 (vs Rs 810). Key risks: subdued EAF production, lower utilisation/ASPs, higher NC cost.