Mahesh Vyas, head of CMIE, looks at Indian manufacturing data and concludes that corporate financials are in good shape. Debt-equity ratios in March 2008 were the lowest in a decade despite a sharp increase in investment. So lending institutions should find companies attractive

Perhaps the most debilitating impact of the current financial crisis is a loss of confidence. Banks do not trust each other and other businesses as there is no transparency or even understanding of the nature and extent of the toxic assets held by enterprises. Suspicion and fear breed panic. And, even in India, banks get extra-cautious in extending credit.

In the past few weeks, media has quoted several anecdotes of companies starving for funds following the meltdown in American markets. Loans were being denied and lines of credit sanctioned to businesses were being canceled. A coincidental liquidity squeeze in Indian financial markets around the same time as the global crisis added tremendous credibility to such stories. Call rates shot up to 18% because of domestic reasons such as advance tax payments and sharp increases in cash reserve ratio requirements. The RBI and SEBI reversed policies to infuse liquidity and rebuild confidence. The result was positive?the call dropped to 7%. But fear is contagious and it continues to be fed by wild rumours of financial distress in companies.

What is the impact of the global financial market crisis on Indian corporates? We seek to answer this question with the help of a little data-crunching. Would companies be starved of funds? Would banks and capital markets be unwilling to provide funds to companies?

Importance of equity marketsThe rapid fall in the equity market indices has raised anxieties about the ability of the markets to supply equity capital to companies. So, we may investigate the role of equity capital and equity markets in financing companies.

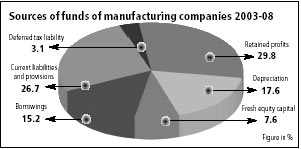

The most important source of equity capital is retained earnings. In fact, retained earnings are the single largest source of fresh funding for manufacturing companies. Retained earnings accounted for 30% of all sources of funds for the manufacturing sector in the last five years. They also accounted for 70% of the total equity capital added by companies in the last five years. Capital markets play no role in this fund source that depends entirely on the profits generated by companies and decisions by their shareholders to retain these profits or distribute them as dividends.

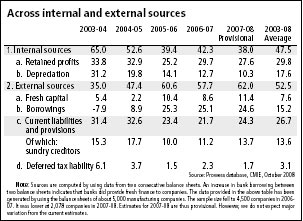

Indian companies have been making good profits in recent times, and finding internal generation of funds a fairly good source of funds. In the five years ended March 2008, internal accruals have been the source of about 30% of the total additional resources garnered by the manufacturing sector. Its contribution has varied from about a quarter to a third during this period. Infusion of fresh equity capital has played a much smaller role in the total fresh resources raised by companies. Its average share was 13.3% in the last five years with a wide variation?from 3.8% to 21.2%.

Even in the case of fresh equity capital, the capital market plays only a partial role. A significant 37.5% of the fresh equity raised by the manufacturing sector was through private placements. Another 24% was raised through rights issues, with only 38.5% raised through the public offer of shares in the past five years, when the Indian capital markets were booming and new investments plans were being rolled out aggressively. Only 13% of the total resources raised by the manufacturing sector were in the form of fresh equity capital.

The markets are unable to channelise household savings into equity capital sufficiently. Or, companies prefer not to approach households directly through the capital markets. They prefer other intermediaries to provide them with finance. This does not deny the importance of the equity capital markets but helps us place its role in perspective. And the inference we can draw from the above is that the recent fall in equity markets is unlikely to significantly impact the ability of companies to raise funds since the markets played only a marginal role in funding companies.

Debt financing and role of banks

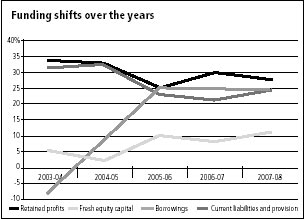

Borrowings have played a smaller role in financing the manufacturing sector than equity. While equity (retained earnings and fresh capital) accounted for 30% of the total additional resources of the manufacturing sector, borrowings provided only 15%. But this average has varied from -8% to 25%. The negative 8% implies that on a net basis, the manufacturing sector returned monies to the banks. This happened in 2003-04. Since then, the share of borrowings has increased and averaged 25%. Thus, in more recent times, the importance of borrowings in financing the sector has been only a shade smaller than retained earnings, which continue to be the single most important source of funds.

Borrowings are mostly from banks, which could starve companies of funds as they themselves could be short on funds. This is a problem being addressed by regulators by infusing more money into the system. Still, banks may not lend as they may believe that companies could default in such times. Much depends on India Inc?s financial health, where the manufacturing sector looked exceptionally healthy.

As of March 2008, the debt-equity ratio of manufacturing companies was at its lowest in a decade in spite of a sharp increase in investments. Companies were highly leveraged during the 1990s. During the boom times of the mid 1990s, the manufacturing sector had borrowed about 1.1-1.2 times shareholders? funds, at a time when corporates raised large sums from the booming equity markets and then leveraged these to raise borrowings. Today, companies are well capitalised and therefore are an attractive target for banks to lend to.

Companies are less stressed to collect receivables today than ever before. The average debtor days had declined to just 33 days as of March 2008. This is an all-time low and much lower than the over-50 days norm in the mid-1990s. This shows in the low working capital cycle of manufacturing companies that was down to just 35 days in 2007-08 compared to over 85 days in the 1990s. This situation is unlikely to have suddenly worsened substantially in the course of the last six months or weeks. So manufacturing companies have a good case to get bank funds. In fact, they are in the best financial health compared to any other time since liberalisation. Companies are also in the midst of robust expansion of capacities. This is therefore the time when they need funds and can take on additional borrowings.

It is therefore not surprising that in spite of consistent increases in the CRR, banks have continued to lend happily to industry. The year-on-year increase in bank credit to industry was a robust 31% as of 29 August 2008.

Sundry creditors and liabilities

The manufacturing sector manages a fairly substantive chunk of its resources from sundry creditors and other sources of current liabilities. These accounted for about 27% of the total resources garnered by it in the past five years.

On a net basis, manufacturing companies need resources to finance their current assets, which do exceed current liabilities. These excess assets (mostly inventories) are financed largely by bank borrowings. But India Inc enjoys higher sundry creditors than sundry debtors, giving it a small but significant surplus. In the past five years net sundry creditors were over five per cent of total resources. Most importantly, this is effectively free money for the corporates.

Conclusion

Retained earnings have been the single most important source of finance for the manufacturing sector in the past five years. Fresh equity capital has played a small role and the equity capital markets have played an even smaller role in financing the corporate sector?s growth. Thus, the current meltdown on the bourses would not impact the resources available to companies. Borrowings have played a smaller role than retained earnings but their share has been growing. Companies are in good financial health with a low gearing ratio. This merits an increase in bank lending or the raising of resources through debt instruments.

The author heads the Centre for Monitoring Indian Economy