In the seventies and eighties, when the East Asian tigers were posting stellar growth rates led by exports, the mainstream thinking in India held that a similar model could not be adopted because of the economy’s continental size. Export pessimism pervaded economic policy opinions and the country’s planners persuaded the belief that India’s growth must originate from within, ie, the domestic market. The strategy to pursue export-led growth anchored upon an undervalued exchange rate policy, which had no takers. It mattered little that India’s share in global trade was miniscule—below 0.5%—and remained stagnant for decades. There was equanimity about pegging the exchange rate to a currency basket.

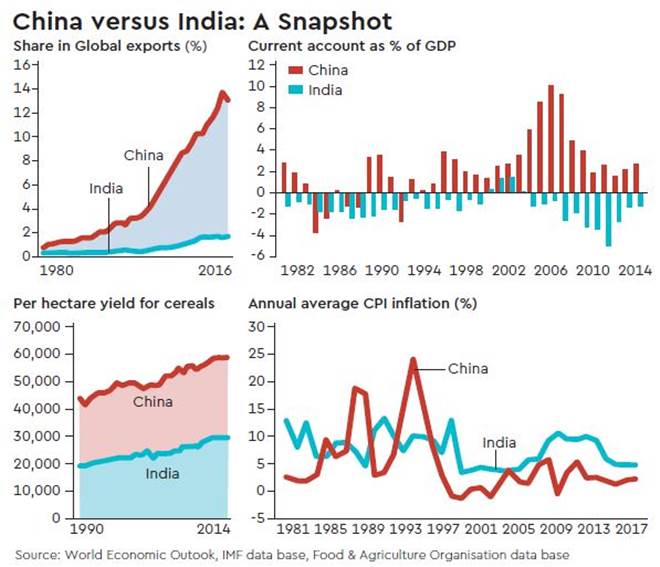

But China had picked up the cue from Asian Tigers, silently devising a new growth strategy centered upon an undervalued exchange rate to propel exports. Its success is now a folklore: it enabled China to reap huge growth dividends as its share of world exports zoomed to 13.8% by 2015, from below 1% in the 1980s. It ran current account surpluses from 1994, which peaked at 10% of GDP in 2007.

How did China manage to sustain a weak currency for so many years despite a regular current account surplus for decades? From a balance-of-payments position, China combined strict capital controls with aggressive forex intervention to absorb surplus forex earnings, manifest in the reserves’ buildup reaching $4 trillion in 2014. Any such strategy would raise two important macroeconomic questions about inflation and stability: One, how did the People’s Bank of China (PBoC) manage the liquidity impact of forex intervention on such gigantic scale? And two, how did the Chinese government handle the exchange rate pass-through to domestic inflation, for China depended heavily on oil and raw material imports for its industry?

The answer to the first question is that ample fiscal space was created to absorb the intervention costs. Taxation reforms yielded significant gains with tax revenues reaching 20% of GDP. Fiscal prudence helped keep debt-GDP ratios fairly moderate, with an eye on high credit-rating. Simultaneously, forex reserves were strategically deployed to extract maximum returns, economic and political.

The critical part, however, relates to the exchange rate pass-through impacts upon domestic inflation. China mitigated this by deep structural reforms in both agriculture and industry, maintaining productivity growth over a long period. In particular, it managed to consistently raise cereal crop yields since the 1990s, which helped contain food inflation despite the manifold jump in demand. Labour productivity in industry leaped as FDI was directed to the tradable sector. Global FDI’s rush into China was primarily to export; the lagged development of its domestic market was incidental for achieving better scale economies, or the icing on the cake.

In substance, different elements inherent in China’s undervalued currency policy-driven export strategy helped transform its economy to much higher levels of efficiency and growth, while taming inflation a lot lower to levels normally observed in the advanced countries (CPI inflation averaged 1.95% in 21 years from 1996).

The remarkable feature here is how the Chinese authorities did not allow currency appreciation throughout these years even when domestic-foreign inflation differentials were minimal, while productivity growth much higher than the trading partners. China’s policymakers were content exporting their domestic savings or current account surpluses abroad and resisted external pressures for upward adjustments to the currency’s value right until they were ready to reorient policies for rebalancing growth towards domestic consumption.

Contrast this with India’s case. Our planners opted for a gradual weakening of the currency within a narrow band until the 1991 balance-of-payments crisis, which forced a major devaluation. In 1994, the rupee became fully convertible on the current account. The post-1991 reforms and a relatively freer exchange rate regime did create an optimistic environment for exports, but gains were tepid as the Asian crisis unfolded. It is worth noting that India’s world export share increased only marginally—to 0.66% by 2000 from 0.5% in 1990—while China more than doubled its share in the same period—to 3.9% from 1.8%!

Post-Asian crisis, Indian policymakers quickly ushered in significant capital account liberalisation even before the exporting sector could secure a sound foothold. Gushes of capital inflows forced premature currency appreciation that affected competitiveness, even while the economy ran persistent current account deficits. India’s export optimism proved myopic for its world export share increased a mere 1 percentage point in the next decade and a half to 1.6% in 2015. China meanwhile, as the folklore goes, became the global leader, increasing its share of world exports to an astounding 13.8%!

The probing question then is, why did India balk at the Chinese approach of exporting its way to growth through an undervalued currency when global trade was expanding at a rapid pace? Why did we shy away from a course that China so successfully traversed, ie, building and expanding a tradable sector for rapid growth and mass creation of jobs to draw out millions engaged in low-productivity agriculture? Why the aversion to a weak rupee?

The answer, unfortunately, lies in the sphere of India’s political economy, which lacked the capacity to handle the stabilisation issues that are inherent in pursuing such a policy. The point can be elucidated by raising a few questions. Why couldn’t RBI intervene as aggressively in the currency market as the PBoC could? The obvious answer is the lack of fiscal space to bear the costs of liquidity absorption. Just a decade and a half ago, we were witness to how a reluctant government agreed to issue ‘stabilisation bonds’, with limits, when excessive capital inflow became hard to manage in the early 2000s. Competitive calls for social sector expenditure on top of high debt-GDP levels left little scope for creating fiscal space for long-term strategic intervention. This left RBI with no option except to calibrate forex intervention operations consistent with the desired growth in its balance sheet and the monetary base. Any surplus, naturally, ended in pushing up the exchange rate.

What if the government had been open to the idea of fully absorbing the costs of forex intervention? Would RBI have gone ahead and built forex reserves of a trillion dollar or so, letting the rupee persistently drift downwards as was the case with the Renminbi? If yes, how would the government have handled the inflation fallout arising from the exchange rate pass-through? An effective response to such long-term stability concerns would then have required significant productivity increases. The answers, therefore, would certainly lie in the political economy domain—the ability for deep structural reforms. Unfortunately, the reform track record on this does not inspire much confidence.

Unlike China, India could not reform agriculture to consistently raise crop yields in response to food price inflation; agriculture reforms could not extend beyond the Green Revolution.

You might also want to see this:

Even after three decades, India has been unable to meaningfully touch factor market reforms, even as those in the product markets have remained incomplete. Efforts to build world class infrastructure spluttered midway. Stuck with structural rigidities and inadequate supply responses, any strategy to anchor an undervalued currency upon export growth would be fraught with high macro-instability risks, thus remaining out of bounds for policymakers.

So perish the thought the rupee can ever be as weak as it ought to be, given India’s persistent current account deficits. To the contrary, policymakers, including the RBI, have often swung to the other end of the pendulum, ie, delving into bouts of currency appreciation by relaxing the capital account. An abiding ‘fear of inflation’ has driven the political economy of the exchange rate into a narrow lane of policy choices, squeezed between the lack of consensus on structural reforms and voters’ sensitivity to inflation. The fallout has been an over-reliance upon demand-side management that does not even shy away from exchange rate-based stabilisation. Willy-nilly, RBI too ended up using the exchange rate as an instrument to fight imported inflation.

What has India achieved with this approach to the exchange rate? From a political economy perspective, inflation concerns have always overridden those of growth, but the unfortunate part of this story is that India couldn’t tame inflation either! We have had to subject ourselves to a new flexible inflation targeting (FIT) regime that could extract a significant sacrifice in growth.

One would expect the new monetary policy regime would not deploy the exchange rate as a policy instrument. But the temptation could be there. The central bank would be fighting a battle to gain credibility for its FIT framework, lower inflation expectations. The recent episode of sharp reversals in the exchange rate did trigger worries if the RBI was deliberately letting the rupee strengthen to contain medium-term inflation within the 6% upper bound. The central bank must realize though that any overvaluation is a short term quick-fix; such actions have been more palliative, followed often by a weakening bout – the near-run on the rupee in 2013 being the latest piece of evidence. One also hopes the government is not enticed by the false sense of improvement in fundamentals or associates a stronger currency with national pride.

Let’s be warned that if the currency is allowed to drift too far at a time when the current account gap is opening up, it wouldn’t be surprising to see a yet another run on the currency in the not-too-distant future!

New-Delhi based economist. Views are personal.