The Phoenix Mills’ (PHNX’s) FY21 and Q1FY22 operations have been impacted by mall shutdowns owing to successive Covid waves. For FY21, mall consumption of Rs 33.3 bn was at 69% of FY20 levels while rental income of Rs 5.6 bn stood at 55% of FY20 levels. To tide over the disruptions, PHNX has raised ~Rs26 bn of equity capital through QIP route and SPV level stake dilution between Aug’20 and Jun’21 and has access to an additional funding pool of Rs 10 bn. We assume a 30% LTL rental income loss for FY22e owing to expected rental waivers in H1FY22 and retain our FY23e estimates as we believe that the long-term growth story for Grade A malls in India remains intact.

We reiterate our Buy rating with an unchanged Mar-22 SoTP based TP of Rs 1,231/share which includes Phoenix Rise office and retail project of 1.3msf and retain our 10% premium to NAV considering growth opportunities from growth capital raised from GIC PE and CPPIB platform deals. Key risks are an extended second Covid wave impacting mall consumption and fall in mall occupancies and rentals.

Covid impacts FY21 consumption & rentals, recovery on cards: Firm expects retail rentals to revert to pre-Covid levels in H2FY22 assuming no third wave of Covid.

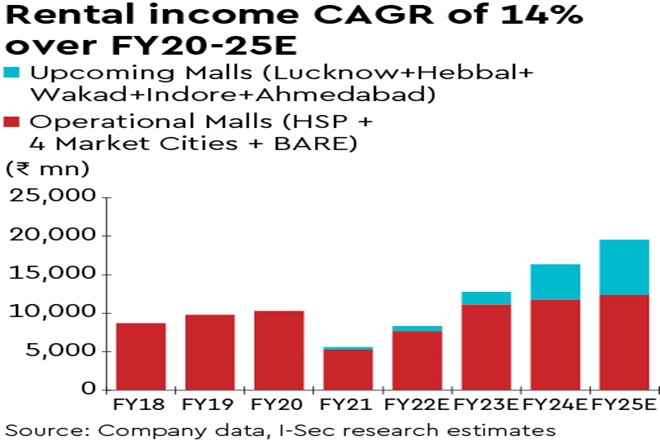

Estimated rental income CAGR of 14% over FY20-25e: PHNX will have ~13msf operational mall space by FY26e (6.9msf currently operational). We expect PHNX to achieve a 14% rental income CAGR (ex-new Kolkata asset) over FY20-25e resulting in Rs 19.5 bn of rental income in FY25e vs. ~Rs 10 bn in FY20. Of this, PHNX share is ~70% or Rs 13.8 bn.