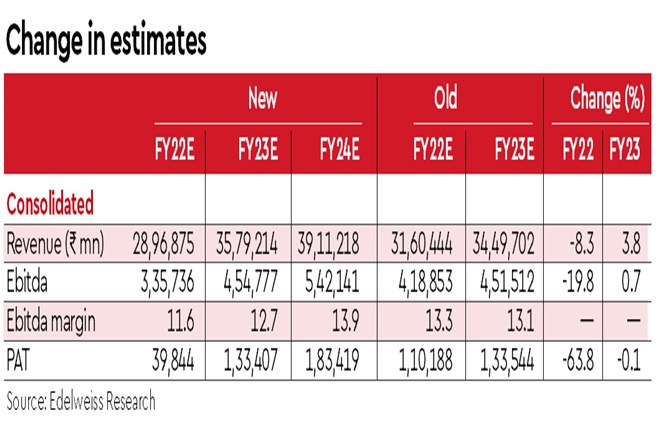

Tata Motors (JLR) has indicated that acute global semiconductor shortage is impacting its production. Taking cognisance of the same, we are revising down FY22e volumes by ~102k units assuming the challenges will persist till Q3FY21. Hence, we are revising down FY22e PAT by ~65%, but retaining FY23 estimates.

We expect global pricing power led by supply constraints and a sharp jump in used vehicle prices. We assume JLR will prioritise production of most profitable models in FY22. Maintain ‘Buy’ with a revised TP of Rs 405 (earlier Rs 436) as we roll over to Dec-22e. Sustained supply constraint is a key risk as H2 volumes are higher than H1.

Semiconductor shortage heating up

JLR press release indicates: (i) Loss of production of 30K in Q1FY22; (ii) expects production to fall by 50% versus earlier planned; (iii) expects Ebit loss and operating cash outflow of GBP2 bn; (iv) demand outlook is extremely strong with outstanding retail orders of 110K units–highest in the company’s history.

Will things normalise from Q4FY22?

As new capacities are expected to come on-stream over the next 12-18 months, we expect some shortage of semiconductors to persist till then. However, we are assuming normalisation (as it existed till Q4FY21 – JLR lost ~7K units of production). This is our base assumption and remains a key variable. It’s pertinent to note that H2 and especially Q4 are generally most important quarters for JLR.

Outlook: Short-term pressure

India and JLR are on the cusp of a strong demand and product cycle tailwind. This should facilitate balance sheet improvement. Hence, we maintain ‘BUY/SO’ with a TP of `405 (JLR at 6.5x Ebit, India at 15x Ebitda). The stock is trading at FY22/23e PER of 30.5/9.1x.

We have assumed normalisation of shortage by Q4FY22. We expect JLR to accelerate its cost efficiency programme and focus on optimising its product mix to limit the impact.