Most investors associate the electric vehicle (EV) supply chain with lithium, cobalt, and semiconductors. But one of the fastest-growing opportunities is emerging in a far less glamorous industrial material that sits inside EV tyres, lithium-ion batteries, cables, and electronic components. And, surprisingly, India already dominates the production of this key raw material.

The material is carbon black. A fine black powder made by partially burning heavy petroleum products in a controlled environment.

Carbon black is traditionally associated with tyre manufacturing. It is used to improve the durability of tyres. But the EV transition is quietly expanding its role far beyond tyres. India, already the world’s largest producer of carbon black, is increasingly finding itself at the centre of this shift.

From Tyre Chemical to EV Material

For decades, carbon black was largely viewed as a cyclical commodity chemical business tied closely to tyre demand. Manufacturers competed mainly on scale, pricing, and feedstock access. That perception is now slowly changing.

When carbon black is produced with far greater precision with tighter control over its structure and chemical properties, it becomes a fundamentally different product. It converts to specialty carbon black. A material that is used in advanced industrial applications such as lithium-ion batteries, conductive plastics, electronics manufacturing, and semiconductors.

This is where specialty carbon black manufacturers gain a strong competitive advantage.

Producing specialty carbon black is technologically complex, requiring very high consistency in quality and process. In battery and electronics applications, customers often test suppliers for several quarters before approval. Once approved, companies rarely switch suppliers because even small quality differences can affect product performance.

As a result, specialty carbon black businesses generally enjoy structurally better economics and pricing power, and demand is less dependent on market cycles.

This is transforming carbon black from a low-margin tyre chemical into a higher-value advanced materials business. For instance, Himadri Speciality, which is moving deeper into specialty materials, saw its EBITDA margin expand sharply from around 6% in FY22 to nearly 22% in FY26.

The Critical Role Inside EV Batteries

Specialty carbon black is increasingly being used as a conductive additive in lithium-ion batteries. Its job is simple but important. It improves conductivity between particles of active material, helping electricity move efficiently through the battery. Without conductive additives, battery performance weakens.

And unlike commodity-grade carbon black, these specialty products command much higher margins. This is one of the biggest reasons why investors are beginning to look at the industry differently.

EVs Need More Carbon Black In Tyres

Not just in batteries, EV tyres consume more carbon black than the tyres in internal combustion engine (ICE) vehicles. EVs are significantly heavier because of their battery packs, often by 20-30% compared to ICE vehicles. They also produce instant torque, putting significant stress on tyres during acceleration.

This combination wears down the tyres quickly. To solve the issue, tyre makers had to build stronger, longer-lasting tyres specifically for EVs. And this is where carbon black becomes critical.

But EV demand is only one part of the story. Geopolitical shifts and changing global supply chains are also helping India emerge as a major carbon black supplier.

Russia, China, and The Supply Chain Shift

The global carbon black market had undergone a hard reset even before the EV demand story fully emerged.

Until 2022, Russia was one of the largest exporters of carbon black to Europe. But the EU ban on Russian industrial exports effectively pushed Russian carbon black out of the European supply chain. Buyers who had relied on Russian exports had to find alternatives.

China was the obvious replacement. It has the world’s largest carbon black market industry by volume, with massive manufacturing capacity. But the situation is not entirely straightforward.

Tighter environmental restrictions on coal-tar and feedstock availability have slightly slowed its exponential growth. At the same time, many European manufacturers have become increasingly reluctant to rely on a single geography for critical industry materials.

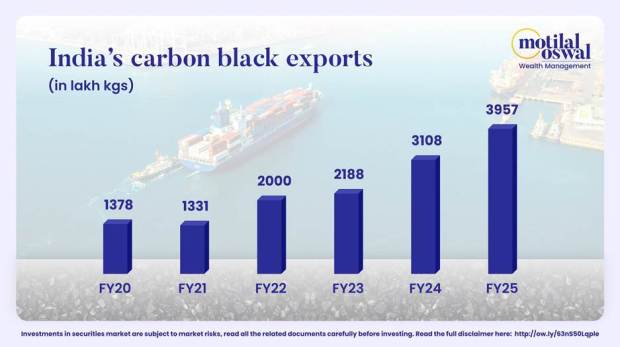

This opened the door for India. Aggressive growth in supply capacity and a feedstock advantage over China have helped India successfully transition from a net importer to a net exporter of carbon black in FY22.

According to a report from Motilal Oswal, India’s carbon black export is growing at a 20% CAGR, 5X faster than China’s 4%. And, India overtook China as the EU’s largest carbon black supplier in just 3 years.

Two Companies, One Opportunity

India has dozens of carbon black producers, but only two companies have pulled ahead in the speciality segment. These are PCBL Chemical and Himadri Speciality Chemical.

Both companies are largely invisible to mainstream investment conversations around India’s EV supply chain. Here’s a closer look at the companies.

PCBL Chemical: Riding The Global Supply Chain Shift

Previously known as Philips Carbon Black Limited, the company is a part of the RP Sanjeev Goenka Group. It is the 6th largest carbon black producer globally and the 4th largest specialty black player globally.

PCBL has also been one of the biggest beneficiaries of the global supply-chain reset. Its European market share has reportedly increased from around 4% to more than 21% over the past two years. But the company is facing short-term headwinds, even as it benefits from strong industry tailwinds.

In 2024, PCBL acquired Aquapharm Chemicals for nearly ₹3,800 crore, as part of its diversification journey into specialty chemicals. The purchase was financed through a mix of debt and internal cash flows. So far, the integration has been challenging, impacting profitability and credit outlook, turning negative.

PCBL Chemical 5-yr Financial Performance

| Metrics | FY21-FY26 |

| 5-yr Compounded Sales Growth | 25% |

| 5-yr Compounded Profit Growth | -7% |

| Operating Margin | 13% (FY26) |

| ROCE (FY26) | 8% (FY26) |

The financials show the stress in profitability, despite rising sales. Over the last five years, PCBL’s sales grew at a CAGR of 25%, but profits declined by 7% CAGR. (Note: FY21 was disrupted on account of Covid, as a result of which the base year financials are suppressed)

However, not everything is bad. PCBL’s specialty business is growing significantly faster than its legacy commodity business. In FY26, the specialty segment grew 12% year-on-year, compared to around 4% growth in the traditional carbon black business.

Himadri Speciality: The Advanced Materials Play

If PCBL represents the scale and export story in carbon black, Himadri Speciality Chemicals represents the industry’s move toward higher-value advanced materials.

The company was founded in Kolkata in 1987 as a coal tar pitch manufacturer, a viscous byproduct of coking coal. Himadri has steadily transformed itself from a traditional carbon materials company into a specialty chemicals and battery materials player.

Today, the company is increasingly focused on high-margin specialty-grade products rather than conventional commodity carbon black.

Himadri operates one of the world’s largest single-site specialty carbon black facilities at Mahistikry in West Bengal, with an annual capacity of around 130,000 tonnes.

Himadri Speciality 5-yr Financial Performance

| Metrics | FY21-FY26 |

| 5-yr Compounded Sales Growth | 23% |

| 5-yr Compounded Profit Growth | 74% |

| Operating Margin | 21% (FY26) |

| ROCE (FY26) | 22% (FY26) |

Himadri’s financial position looks much stronger compared to PCBL. The company’s free cash flow at the end of FY26 was ₹121 crores, giving it the flexibility to invest in future growth opportunities.

Its financial statement reflects the benefits of moving deeper into specialty materials. Over the last five years, sales grew at a CAGR of around 23%, while profit increased at a CAGR of 74%. (Note: FY21 was disrupted on account of COVID, as a result of which the base year financials are suppressed)

Operating margin increased from 8% in FY21 to 21% in FY26.

Himadri is now attempting to move even further up the value chain. The company is working on commissioning an LFP cathode active material plant with an annual capacity of around 40,000 tonnes starting Q3FY27, with the aim of reaching full planned capacity by FY29.

Once scaled successfully, the facility could become the world’s first commercial-scale LFP plant outside China.

LFP, or lithium iron phosphate, is currently one of the most widely used battery chemistries in electric vehicles and large-scale energy storage systems because of its lower cost, longer cycle life, and better thermal stability.

Valuation: Commodity Cycle Or Advanced Materials Premium?

The valuation gap between PCBL Chemical and Himadri Speciality Chemical shows how differently the market currently views the two businesses.

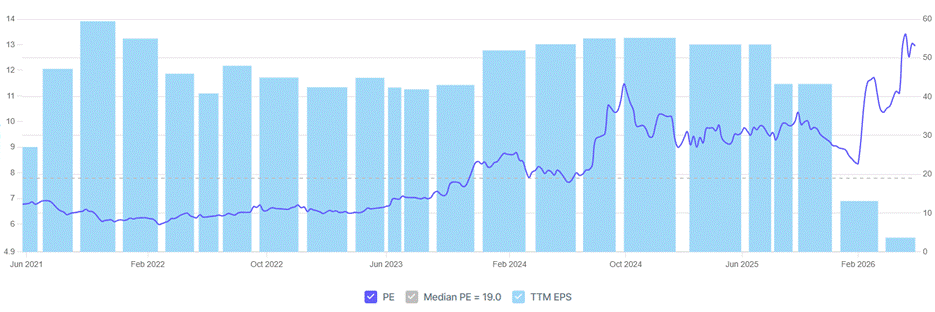

PCBL Ltd. 5-yr Price-to-earnings Chart

PCBL’s valuation multiple has remained volatile over the past few years. The stock earlier traded largely in the low- to mid-teen PE range. The 5-year median PE is 19, largely reflecting its positioning as a cyclical commodity chemical company.

Currently, the stock is trading at a PE of 53, significantly above its historical median. However, much of this sharp rise is due to the recent decline in earnings rather than a major rerating in the business itself.

Having said that, despite improving export market share and rising specialty business contribution, the stock is struggling to move higher. The reason is the financial stress due to the Aquapharm acquisition, which is weighing heavily on investor sentiment.

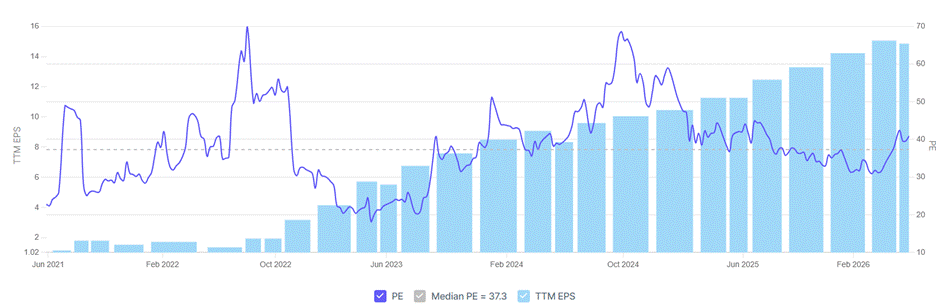

Himadri, on the other hand, is being valued very differently. Its historical PE multiple has consistently remained significantly higher than PCBL’s, reflecting the market’s confidence in its transition toward a specialty materials business. Unlike PCBL, Himadri’s earnings growth has also remained strong and relatively consistent over the last few years.

One of the most interesting aspects of the carbon black story is that the market is valuing the two companies very differently, reflecting two completely different investor expectations.

Himadri Speciality 5-yr Price-to-earnings Chart

However, the market narrative around PCBL Chemical could change if the Aquapharm acquisition stabilises and the contribution from specialty carbon black continues to rise. A recovery in margins and return ratios, particularly ROCE, would likely push investors to reassess the company beyond its current commodity-chemical positioning.

At the moment, the market is viewing PCBL more as a contra opportunity. A structurally strong business facing temporary operational and balance-sheet stress.

Himadri Speciality Chemical, on the other hand, is being treated as a growth stock, with investors willing to pay a premium for its exposure to specialty materials, battery chemicals, and the broader EV supply chain.

India’s Most Underappreciated EV Supply Chain Story

India’s opportunity in the EV supply chain may not come from lithium mining or becoming a global battery manufacturing giant overnight. Instead, it could come from supplying critical industrial materials that EV and battery makers quietly depend on.

Carbon black is increasingly becoming one of those materials. What was once seen mainly as a tyre chemical is gradually evolving into a specialty materials business linked to batteries, electronics, and energy storage.

The market is already rewarding companies moving deeper into high-value specialty materials. However, China remains a major competitive threat, with the ability to pressure global pricing through aggressive capacity expansion.

Still, whether it is PCBL Chemical’s turnaround story or Himadri Speciality’s move into battery materials, the larger industry trend is becoming difficult to ignore. You can consider adding these stocks to your watchlist.

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Deepan Datta has spent over a decade studying stocks and mutual funds. His passion is to uncover interesting stories in the financial markets and share them through his writings with investors at large. He is focused on delivering clear, easy to understand and research-backed insights. Deepan began his career as a Research Associate at S&P Global, where he developed a strong foundation in financial research and data analysis.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.