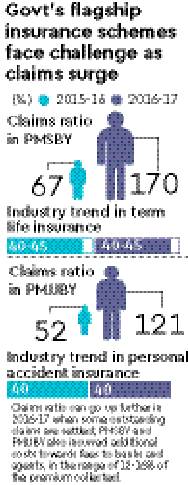

The high level of claims for the Narendra Modi government’s flagship social-security insurance schemes are threatening their viability. The claims-to-premium ratio for the Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) — a term life insurance policy — hit an unsustainable 121% in 2016-17, the second year of operations.

The ratio was an even higher 170% in 2016-17 for the Pradhan Mantri Suraksha Bima Yojana (PMSBY), under which payment of Rs 2 lakh is guaranteed in the case of accidental deaths or grievous injuries.

These schemes, launched in May 2015, were projected as path-breaking steps to provide affordable, universal access to essential social security protection. The annual premium payable under PMJJBY, which covers even suicidal deaths, is Rs 330 while the same is just Rs 12 for PMSBY. The premium amount has to be paid by May-end every year for renewal and the policies are linked to the beneficiary bank accounts.

In the first two years of the schemes, the claim-to-premium ratios were 88% for PMJJBY policies, under which the sum assured is again, `2 lakh, and 121% for PMSBY. Compare this with the claims ratio of 40-45% for usual personal-accident and term life covers.

Very high claim ratios have caused a sense discomfort among insurers over the polcies, particularly PMSBY. Mostly public-sector insurance companies like New India Assurance, National Insurance Company and United India Insurance offer the extremely low-cost policies under PMSBY.

According to sources, the insurers have made several representations to the government, asking for a major increase in premium amount so that the losses from PMSBY don’t surge. “The companies have written to the government suggesting that PMSBY be repriced from Rs 12 to Rs 75-100 while agreeing to give a higher accident cover of Rs 4 lakh,” an actuary with a state-run insurance company told FE.

The government is, however, still on a wait-and-watch mode as it is hopeful that once the pool of policy holders reach a critical mass, claims ratio could climb down. Analysts also feel that the trends in the two schemes meant for the poor need to be watched for another couple of years before repricing them.

“It (claims ratio in PMJJBY) is not very alarming as of now. But, if this trend continues year after year, then something has to be done in terms of pricing,” said S B Mathur, former chairman of LIC and Life Insurance Council. He is of the view that even claims ratio of 105-106% should not be an issue given the social-security nature of the schemes. Insurance earn at least 6-7% annually from investing premiums collected. Mathur cited claims ratio well above 100% in the third-party motor insurance policies to drive home his point.

The losses to insurers from the social-security schemes are higher than the differential between claims and premiums as they also incur additional expenditure on agent and bank fees. Such expenses stood at Rs 127 crore for PMJJBY and Rs 20 crore for PMSBY in 2016-17.

Rise in claims ratio is one reason why the two policies are not aggressively marketed by insurers; the number of policies under both schemes grew by just 5% in 2016-17 – 3.11 crore and 10.02 crore people have obtained PMJJBY and PMSBY policies till May-end, 2017. About 29 crore bank accounts have been opened under Pradhan Mantri Jan Dhan Yojana in the last three years to provide various social security benefits to the poor seamlessly.

You may also like to watch this video

“If the claims ratio continues to be at such high level for another 1-2 years for both PMSBY and PMJJY schemes, then one could see price revision or change in entitlements. One option is to reduce sum assured for the older people and retain/increase the same for younger people,” said Kapil Mehta, co-founder of SecureNow Insurance Broker.