Excluding the contribution of Capco and Metro, we estimate organic revenue growth for Wipro at ~2.8% q-o-q (CC). While this is in line with average June quarter growth for the industry before Covid, it is higher than Wipro’s track record. Organic growth during the quarter was lopsided towards consumer (~14% q-o-q, CC) and ENU (~12% q-o-q, CC) verticals. Revenue run-rate in some verticals, e.g. healthcare and manufacturing, remains close to pre-Covid levels (Mar-20).

Wage hikes still due, Ebit margin contracted ~220bps q-o-q led by Capco integration and investments. As with the rest of the industry, attrition inched up sharply (340bps q-o-q to 15.5%) for Wipro too.

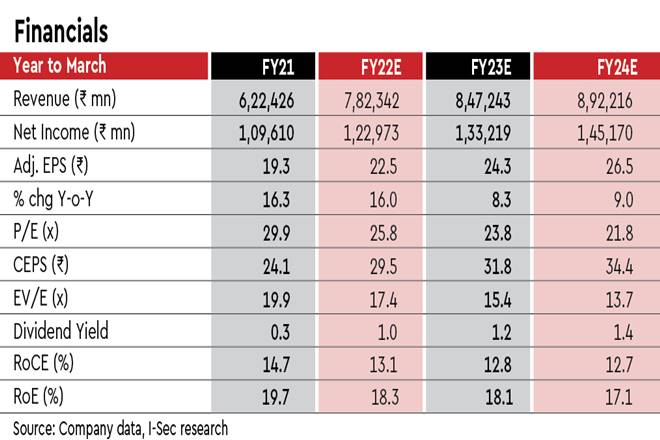

We estimate organic revenue growth guidance for Q2FY22 at 1.7%-3.7% q-o-q, largely in line with expectations. Ebit margin guidance of 17-17.5% has been retained. We see a downside risk given the impending wage hikes, supply-related cost pressures and planned investments. Even as incipient signs of a turnaround are encouraging, we await further evidence of sustainable execution on this front. Current valuations (24x FY23e EPS) more than price in a turnaround. As we see higher scope for incremental disappointments v/s surprises, we retain our Sell rating.

Revenue beat, miss on margins: IT services’ revenue grew 12% q-o-q (CC), led by Capco/Metro acquisitions. We reckon organic revenue growth for Wipro ex-Capco and ex-Metro at ~2.8% q-o-q (CC). Growth in BFSI (ex-Capco), healthcare, manufacturing and technology was weak. Capco integration (130bps impact) and investments in talent (90bps impact) were the key margin headwinds. Sequentially, there was a marginal increase in utilisation. Gain on sale of asset led to higher than normal other income. In addition, lower ETR led to beat on EPS despite Ebit missing our estimates.

Organic growth outlook is in line with expectations: Wipro has guided for 5-7% q-o-q (CC) growth for Q2FY22. This incorporates incremental inorganic revenue from Capco and Ampion acquisitions. Organically, we estimate the guidance to be in the range of 1.7-3.7% q-o-q (CC) – typical growth level of the industry in Sep quarter (also seasonally strong).