bank branch in Mumbai, India, on Monday, June 3, 2019. The Reserve Bank of India rate decision is scheduled for June 6. Photographer: Dhiraj Singh/Bloomberg")

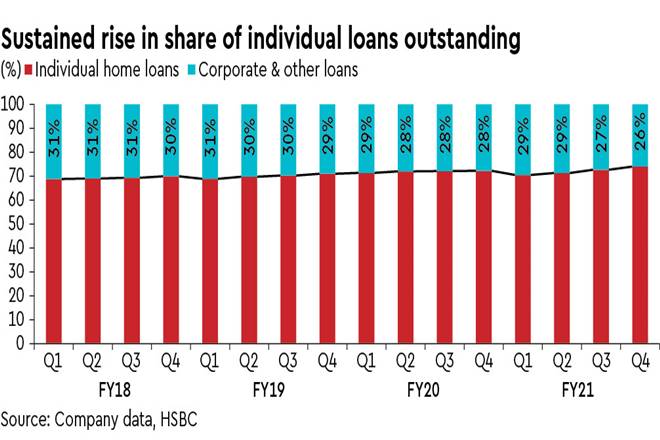

HDFC delivered a solid 60% y-o-y increase in individual home loan disbursements in Q4 (42% y-o-y growth during H2FY21), which resulted in a healthy 5% q-o-q and 13% y-o-y increase in individual loans (net of assignments). Overall loan growth (+11% y-o-y /+3% q-o-q), however, was impacted by heavy run-down in the lease rental discounting book during the quarter. Management indicated that loan disbursements in April alone are higher than that recorded during Q1FY21. However, the momentum is likely to cool off in coming months due to rising COVID-19 caseload and intermittent lockdown situation.

Asset quality remains stable: Overall asset quality remained largely stable with gross stage 3 assets at 2.3% – stable q-o-q. Segmental asset quality too remained stable. Restructured loans stood at ~Rs 45 bn or 0.8% of AUM, of which around 27% were individual loans and balance from non-individual segment. Restructured loans are classified as stage 2 assets. Disbursements under ECLGS scheme stood at ~`25 bn (~0.4% of AUM). Bad loan write-offs in FY21 stood at Rs 13.7 bn or ~0.25% of AUM.

NIMs compress q-o-q; opex remains elevated: Sequential compression in loan yields outpaced the decline in cost of funds, thereby putting pressure on net interest margins. Interest on interest reversal of Rs 1.1 bn also impacted yields. However, this was offset by healthy assignment income of Rs 4.4 bn which helped recoup some margin loss. Opex remained elevated on higher ESOP related costs.

Outlook: We reduce our FY22/23e earnings by an average 7% on lower growth assumptions and revise our SOTP-based TP to Rs 2,900 (from Rs 2,930 earlier). We retain Buy rating as we believe HDFC’s dominant position in the mortgages segment makes it well poised to benefit from strong demand in individual housing. Also, falling cost of funds allows it to compete against large banks and protect/grow its market share.

With the core mortgage business trading at c2.1x FY23e PBV, valuations are attractive, in our view. Besides, most of its subsidiaries in the financial services space continue to do well. Downside risks: (i) prolonged and deepened impact of the second wave of COVID-19; (ii) aggressive product pricing by banks; and (iii) a moderation in housing demand.