")

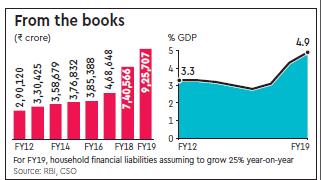

Given how borrowings by households rose a good 58% in the year to March 2018, it’s clear there’s no let-up in consumer aspirations. Financial liabilities of households stood at Rs 7.40 lakh crore in March 2018, revised data from the Reserve Bank of India (RBI) show.

That’s a modest 4.3% of GDP and assuming borrowings rose by about 25% in 2018-19, the liabilities would be less than 5% of GDP.

Data from BIS put the total credit to households at Rs 20.99 lakh crore at the end of December 2018, or approximately 11% of GDP. That is a comparatively low level of leverage and more or less at the same levels as at the end of 2017.

With more consumer credit history at their disposal, lenders today are more comfortable lending to individuals and not only those earning a salary.

In fact, the share of unsecured loans has risen sharply over the past two years as banks are now able to do better due diligence. Since these loans fetch much better yields, they prefer them to collaterallised credit where repossessing the asset in the event of a default can be costly and time-consuming.

While there has been a clear attitudinal shift towards spending, the slowdown in credit flows from NBFCs over the past year or so, would have left many borrowers without access to loans.

Ironically, this is happening at a time when interest rates are trending down. One interesting trend seen in the past few years is that the average ticket size of loans has been falling; that’s a reflection of rising inclusiveness.

However, home loans dominate the portfolios of lenders in terms of value while personal loans are the fastest-growing segment. The share of NBFCs in the total credit to consumers is expected to have fallen since August last year.