Reserve Bank of India (RBI) governor Raghuram Rajan on Tuesday said the central bank will soon revise the marginal cost of funds-based lending rate (MCLR) mechanism. The MCLR formula had been prescribed as the benchmark for pricing loans from April 1, instead of the base rate. Disappointed that banks had not passed on the benefits of lower policy rates to borrowers despite ample liquidity, the governor said the cuts had been modest. “Earlier, some bankers said that it was the lack of liquidity that was holding rates high. Now I hear from some that it is fear of the FCNR(B) redemption that is making them reluctant to cut rates. I have a suspicion that some new concern will crop up once the FCNR(B) redemptions are behind us,” he said.

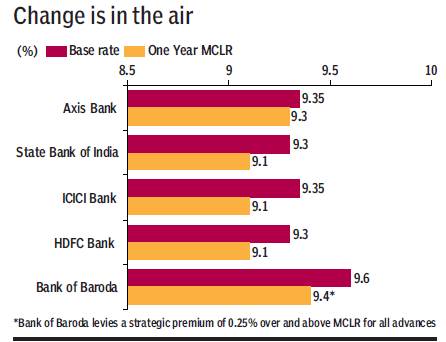

The MCLR was introduced to enable faster transmission. The base rate allowed banks to calculate the cost of funds based on the average cost or marginal cost of funds or any other methodology. This effectively meant they waited for deposits to be repriced and consequently rate cuts were delayed. While MCLR is also primarily a function of cost of resources, it is based on the marginal cost of money.

Essentially, it is the sum of the products of the rates offered for deposits/borrowings and the outstanding balance. So, for instance, if the deposit base of a bank consists more of low-cost current account and savings account (CASA) deposits, its marginal cost of funds and consequently MCLR, would be lower and vice versa.

The other differentiating feature of MCLR vis-à-vis base rate is the fact that while the latter was uniform for loans of all tenure, the RBI has mandated banks to announce MCLRs of at least five tenures – overnight, one month, three months, six months and one year. Simultaneously, it has allowed banks to add a tenure premium to each MCLR.

Market watchers believe that rather than tweaking the framework soon after its launch, the RBI should instead let the competition from the bond market force banks into lowering interest rates.

Loan growth has been subdued so far this year, whereas in the first quarter, more than Rs 1.3 lakh crore was mopped up through the corporate bond market. This follows R4.6 lakh crore raised in FY16, Securities and Exchange Board of India data reveals.

Bankers for their part point to the subdued growth in deposits – especially current and savings accounts – as a reason for loan rates not coming off. Arundhati Bhattacharya, chairman of State Bank of India, had recently told FE that it would be difficult to drop deposit rates, so it could be a while before loan rates come off.

Bankers say the MCLR is a simple calculation, which can’t be tinkered with. However, with the deposit growth being weak, it would be difficult to lower rates without endangering the franchise.