From the next fiscal, insurance companies will have to maintain a solvency margin of 145% instead of the 150%. The Insurance Regulatory and Development Authority (Irda) has decided to move towards a risk-based solvency approach and has constituted an expert committee to suggest the road map.

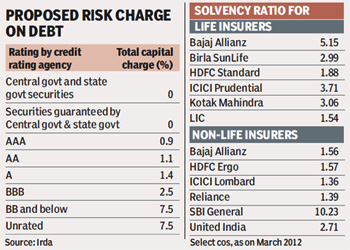

By moving towards a risk-based solvency approach, it will deter insurers from investing in risky assets. The market risks that will be covered include interest rate risk, equity risk, property risk, spread risk and concentration risk. Insurers are required to invest funds following Irda?s guidelines. Currently, though majority of funds need to be invested in government securities and approved investments, no risk charge is provided to the insurers who invest in more risky investments. The regulator, in a draft exposure, has decided to define the percentage to adopt the risk-based solvency approach in line with the Solvency-II norms on capital adequacy requirements.

By moving towards a risk-based solvency approach, it will deter insurers from investing in risky assets. The market risks that will be covered include interest rate risk, equity risk, property risk, spread risk and concentration risk. Insurers are required to invest funds following Irda?s guidelines. Currently, though majority of funds need to be invested in government securities and approved investments, no risk charge is provided to the insurers who invest in more risky investments. The regulator, in a draft exposure, has decided to define the percentage to adopt the risk-based solvency approach in line with the Solvency-II norms on capital adequacy requirements.

Solvency margin is the amount by which the assets of a life or non-life insurer exceed its liabilities and is a part of the shareholders? fund and not policyholders? fund. For a policyholder, looking at the solvency margin of insurance companies is important as it will determine whether it is in a position to pay claims. In fact, an insurer will be insolvent if its assets are not adequate or cannot be disposed of in time to pay policyholders? claims.

Analysts say it is important to look at the solvency margin of private life insurance companies as they are not backed by the government and are more susceptible to market risks. In fact, at the end of March 2012, all the 24 life insurers complied with the stipulated requirement of solvency ratio of 1.5. Life Insurance Corporation of India reported a solvency ratio of 1.54, which was the same as at the end of March 2011. Data from Irda show that as on March 2012, 22 private life insurers have maintained the solvency ratio at above 1.70 out of which 17 had the solvency ratio at above 2.50. Of course, high solvency margin could also mean that the company is simply not investing and is sitting on its cash pile.

Under Section 64VA of Insurance Act, 1938, every insurer will have to maintain an excess of the value of assets over the amount of liabilities of not less than an amount prescribed by Irda. The Irda annual report for 2011-12 underlines that one of the important factors that influences insurance penetration is the capital requirement under the solvency margin. Emphasising that since pure term products provide simple life cover, companies should design products, which could reach various segments of the population in meeting their insurance needs and enhance insurance penetration. In line with this objective, the regulator had decided to allow the life insurers to reduce the capital requirement in the case of pure-term products without changing the factors loading in the case of the remaining products.

Typically, for an insurance company assets are fixed and investment assets, whereas liability is future payouts like claims, surrender benefits and maturity benefits and based on future projections of these payouts, an insurer will arrive at its liability. The Irda has suggested that risk charge should be applied for all mandated and non-mandated assets of the insurer. For life insurers, assets pertaining to the non-linked business should only be considered as the risk pertaining to the linked business is being borne by the policyholders. For life insurance companies, the minimum solvency will be the policy reserve as disclosed by an actuarial valuation of the liabilities and for non-life insurance companies it will be based on the net premium or net claim.