reported better-than-expected earnings due to lower operating expenses and credit costs.")

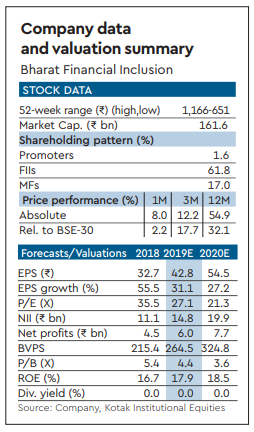

Bharat Financial Inclusion (Bhafin) reported better-than-expected earnings due to lower operating expenses and credit costs. Loan growth, though high at 38% yoy, was 7% below our estimates and 6% below guidance. Borrower acquisition continued to be healthy but growth in average ticket size was moderate at 2% q-o-q and 18% yoy. We are cutting our near-term growth and other income estimates. Our forecasts do not include any synergies of the proposed merger with IIB.

Loan growth guidance missed

Bhafin’s PAT of `2.1 bn was 8% y-o-y ahead of expectations, led by lower credit costs and operating costs. AUM of `126 bn grew 38% y-o-y compared to stated guidance of 48% y-o-y growth. Miss on AUM growth drove 3% y-o-y miss on NII growth, even as the headline growth of 88% y-o-y was high due to demonetisation-related interest reversals in the base quarter.

Key highlights of 4QFY18 performance

AUM growth of 38% y-o-y and 10% q-o-q was driven by active borrower growth of 16% y-o-y and ticket size growth of 18% yoy. Notably, Bhafin has revised its policy (in line with MFIN guidelines) to increase limit of maximum lenders to three from two and indebtedness to `80,000 from `60,000 earlier. NIM (calculated) improved 10 bps q-o-q and ~300 bps y-o-y to 10.3%. Income from investments of `140 mn was below expectation and down 53% y-o-y.

Cost-income ratio declined 500 bps q-o-q to 49% (59% in 4QFY17). Operating costs grew by 37% y-o-y, similar to overall loan growth. Active borrowers per employee improved by 7% y-o-y/q-o-q. 97% of disbursements are cashless in nature, supporting operating efficiency.

Bhafin’s cumulative collection efficiency was 99.8% for new loans disbursed from January 2017—these loans constitute 95% of gross loan portfolio as of March 2018. Gross NPL declined to 2.4% from 4.6% q-o-q due to large write-offs that were already provided for. GNPLs reduced to `4.01 bn from `4.11 bn q-o-q due to collections; the company made write-offs of `1.9 bn. Bhafin’s other income was `990 mn, up 23% y-o-y mainly due to loan processing fees and distribution fees.