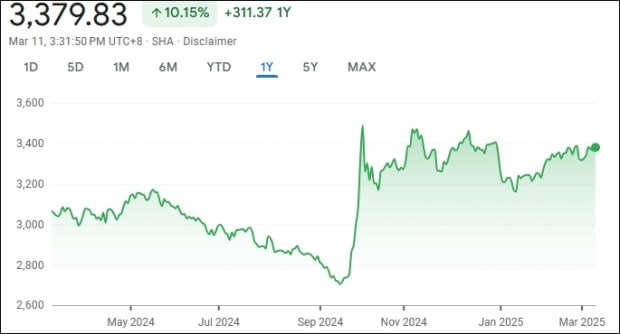

The Shanghai Composite Index (SHCOMP), a key indicator of the Chinese stock market, could be the turnaround story that global investors are waiting for. The big turn happened in September 2024 when the Chinese government unveiled key reforms in the real estate sector.

Then, China’s property market stability and economy were bolstered by coordinated efforts to address low confidence, falling prices, and liquidity issues affecting major developers. Since then SHCOMP has climbed 22% and is currently around 3,300. It had crashed to a low of 2,700 in September 2024.

Here’s a brief on the journey of the Shanghai Composite Index. Shanghai Composite Index was at an all-time high level of around 5,133 in January 2007, before the global financial crisis hit the financial markets. The next high was 4,381 which was reached in January 2015.

However, except for the bullish sentiment taking hold in September 2024, the sentiment had been tepid over a long time frame. Over the last three years, the index has been range-bound around 3,300. The index is down 4% over 3 years but is up by 10.15% over 1-year and nearly flat YTD.

Source: Google Finance

China holds big promise for investors as the stocks have remained range-bound for many years now. Recently, China also highlighted its robust policy toolkit to stimulate economic growth, emphasizing plans to advance technological innovation and boost domestic consumption, among other initiatives.

But the big question is whether FIIs are excited about China? And, are FIIs actually investing in China?

Chinese stocks could be depressed for various reasons, but on valuations they are looking attractive. The China-MSCI China Index PE Ratio is at 13 while India-MSCI India Index PE Ratio is at 22.

Nomura in its latest Asia-ex Japan Equity Strategy note retained its ‘Neutral’ stance on China and ‘structural Overweight’ on India stocks. The foreign brokerage said there is a scope of near-term outperformance of China over India, but it may not be long-lasting.

For China, it continues to believe that investors should be overweight China’s technology-related sectors, citing many incremental positives including the DeepSeek/AI narrative.

Nomura also cited US-China tensions, where the White House’s ‘America First Trade Policy’ and ‘America First Investment Policy’ designates China a key foreign adversary. Trump has already imposed an additional 20 per cent tariffs on Chinese imports.

The country’s economic future remained clouded by a deepening trade war with the United States, with Beijing indicating its willingness to engage in ‘any type of war’ and dismissing the US’s fentanyl-related justification for slapping tariffs as a ‘flimsy excuse.’

Stocks to Watch

Chinese IT megacaps are challenging the US tech titans. The challengers to the ‘Magnificent Seven’ stocks, dubbed as the ‘7 titans’ by Societe Generale SA, the group include Alibaba Group, Tencent Holdings, Xiaomi, BYD, Semiconductor Manufacturing International, JD.com, and NetEase.

This year’s $439 billion gain in Chinese IT megacaps has left their once unbeatable US peers in the dust, and many investors believe the outperformance will continue.

Deflationary Pressure

While the stock market seems to have responded to the stimulus, the economy is yet not out of the woods. The fear of deflation is getting real in the Chinese economy.

Last week’s data showed that China’s deflationary pressures worsened in February 2025, with both consumer and producer prices falling more than expected on sluggish consumer spending.

The current figures may fuel discussions about using more substantial stimulus measures to combat falling inflation and boost domestic demand. Expect some sentiment boosting news from China’s National People’s Congress soon.

What is happening to Chinese trade

China is exporting more and relying less on imports. That has led China’s trade balance to expand beyond expectations in the first two months of 2025, driven further by an unexpectedly steep drop in imports amid U.S. trade tariffs and weaker domestic demand.

The trade balance increased to $172.50 billion in January-February, versus projections of $143.10 billion. Imports declined 8.4% in January-February, compared to estimates of a 1% increase. Exports increased by 2.3% year on year, falling short of estimates of 5% growth and dropping drastically from 10.7% in December.

Another big development that has started to happen in the currency market is putting Chinese markets in a sweet spot. The dollar has recently lost strength, and this is reflected in the dollar index.

The US Dollar Index (DXY), which tracks the greenback against a basket of currencies, is at its lowest level since early November 2024, hovering around 103.45. If the dollar weakens, it’s an advantage to emerging markets, including India. However, as of now reallocation away from India and towards China still seems to be happening. If the DXY continues to weaken, however, this could change.

Also Read: US stocks fall after Trump declined to rule out a recession

Latest from China

The Ongoing Chinese National People’s Congress week-long meeting is expected to reveal much of the government’s efforts to shore up the dwindling economic conditions and provide cues for the market. Policymakers are prioritizing increasing consumer stimulus and economic support as top priorities.

The NPC is anticipated to aim for 5% GDP growth despite real estate and trade issues. Foreign policy, military spending, and technological developments will all be important subjects at the sessions, which will be widely watched across the world.

Will the Shanghai Composite Index once again react bullishly to these developments? Only time will tell…

Also Read: Indian investors set to trade while US sleeps as Nasdaq explores round-the-clock trading