offers a long-term investment opportunity notwithstanding growing investor discomfort regards falling margins and new order delays.")

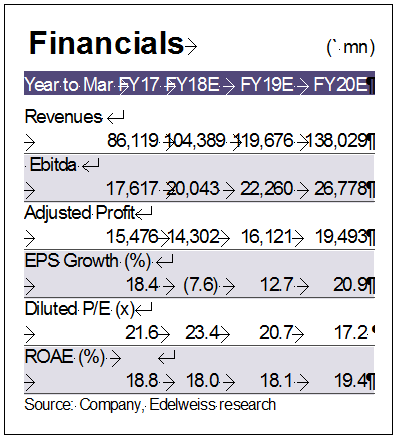

In our view, post the recent 30% plunge in stock price, Bharat Electronics (BHE) offers a long-term investment opportunity notwithstanding growing investor discomfort regards falling margins and new order delays. We are positive as a medium to long-term growth/competitive profile remains intact. Additionally, our sharp 20% cut in FY19/20e earnings factors in delays in large order intakes/inferior revenue mix. We maintain ‘BUY/SO’ with a revised target price of Rs 185 (Rs 230 earlier) given reasonable 15% Ebitda growth and strong RoE/RoCE profile (20/27%). We maintain our exit multiple of 23x as well, given BHE’s sustained competitive edge and long-term growth profile. Cochin Shipyard remains our top bet in the defence space.

Sharp 30% correction in past 4M: The stock plunged 30% in past four months. We cut our FY19/20e earnings by 20% to factor in the relatively higher impact of lower-margin civil business in FY19e along with overall delays in two large orders.

Key risk over 12-24 months: FY19e order intake, in our view, will be front-ended given upcoming elections and advanced stage of Akash/LR SAM. Potential delays could result in next round of ordering happening in FY20e, a key risk for BHE.

Outlook and valuations: Our ‘BUY/SO’ is based on BHE’s sustainable competitive profile amid rising opportunities for local players. At CMP the stock trades at 21/17x FY19/20e EPS.