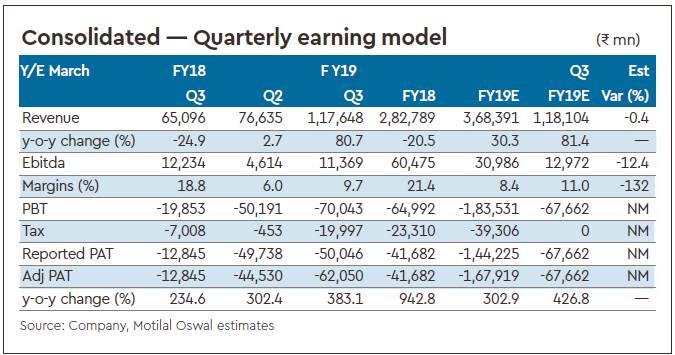

Revenue declined 2.2% q-o-q to Rs 117.6 bn (in-line). Ebitda grew 16% q-o-q to Rs 11.4 bn (12% below our est.), while Ebitda margin increased 160bp to 9.7%, due to realisation from merger synergies. Adj. net loss stood at Rs 62 bn v/s Rs 44.5 bn q-o-q. ARPU stood at Rs 89, up 1.5% v/s our estimate of Rs 92, but, this was offset by better-than-estimated subscriber base. Subscription base declined 8.3% to 387 m (2% beat), a fall of 35.1 m due to the Minimum Recharge Vouchers. Traffic declined 2.6% to 712.3 bn. However, MoUs increased 2% to 580 min/month.

Data volumes increased 11% to

2.7 bn GB. This is 65% below Bharti/RJio’s data volumes (~8-8.5 bn GB) in Q3FY19. Data/broadband subscriptions stood at 146.3 m/107 m with 6.2 m/8.2 m subscriber additions (28% broadband penetration). 4G subscriber additions were 9.5 m, taking the total to 75.3 m (19% penetration), highlighting a shift from 3G to 4G, though it was much below competition.

Capex was at Rs 11.4 bn lagging against its annual guidance of Rs 160 bn, as suppliers were finalised in Q3 and will increase in Q4. The company reduced towers by 4.5k to 198k. While broadband towers stood at 158k, it added 2k towers with 69% population coverage. 4G population coverage is at 64% v/s management target of >70%/>80 by Mar’19/20. Net debt stood at Rs 1,148 bn with Rs 89 bn in cash.